Refractory Bricks Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

PW Consulting today publishes a forward-looking intelligence brief on the refractory bricks market designed for corporate strategy teams, procurement leaders, investors, and policy makers preparing decisions in 2026. Built on a proprietary market model and validated through primary interviews with producers, end-users and raw-material suppliers, the report translates complex dynamics into executable options for action — while preserving the full datasets and segment tables for subscribers.

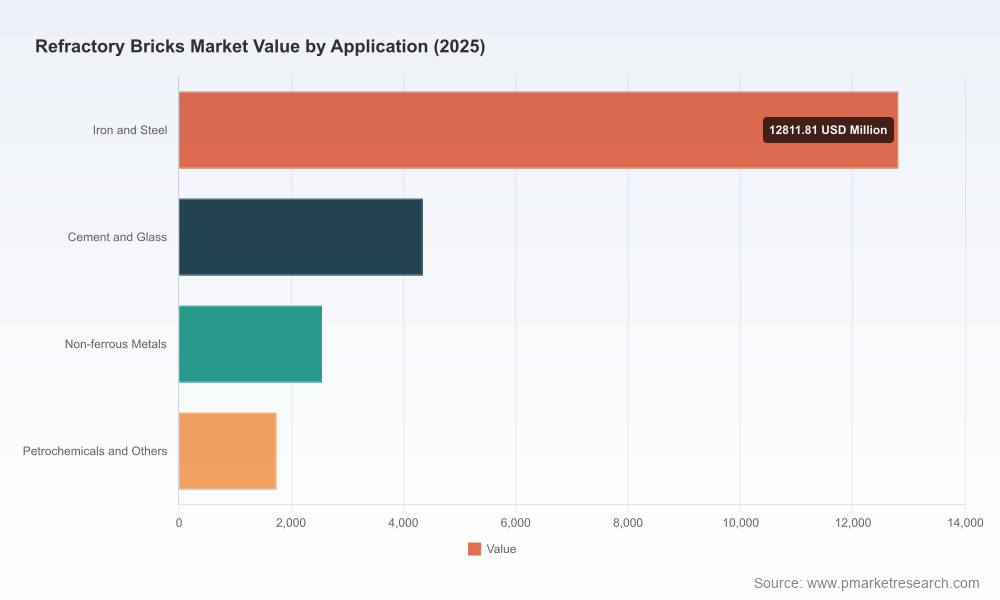

Refractory Bricks Market

Market at a glance — what the numbers imply for strategy

The refractory bricks market is established and growing. Our base-year analysis positions the global market at roughly USD 21.45 billion in 2025, with a forecast compound annual growth rate (CAGR) of approximately 4.62% across the 2026–2032 horizon. At that pace the market approaches the upper end of its historical elasticity range by the end of the forecast window, reflecting steady demand from high-temperature industries and incremental product premiumization.

Refractory Bricks Market

Those headline figures mask a set of asymmetric forces that will determine winners and losers in 2026: raw-material price volatility and concentrated exposure to key feedstocks; an evolving regulatory overlay in major manufacturing geographies; and selective capacity moves and M&A that are reshaping supplier bargaining power. Our brief maps these vectors into decision-ready scenarios, showing how a relatively modest annual growth rate translates into meaningful value shifts along the value chain.

Refractory Bricks Market

Why this brief matters for 2026 decisions

- Actionable timing: 2026 is the year many procurement contracts, retrofit programs and capacity investments will be re-priced. The brief identifies where to accelerate commitments and where to wait for price clarity.

- Cost-to-serve reappraisal: Refractory producers face cost structures dominated by a small set of raw materials; our cost curve and sensitivity analysis show how +/- volatility in alumina, magnesia and silica cascades into margins and maintenance cycles for customers.

- Regulatory risk and opportunity: New emissions and trade measures — notably recent EU guidance on ceramic manufacturing and changes to import duties in major mineral-exporting countries — make local production economics and compliance investments central to site selection and supplier selection decisions.

- Concentration and consolidation pathways: Market concentration metrics in the brief show a mid-level headline consolidation; we translate that into concrete M&A and partnership playbooks for both strategic and private equity investors.

What’s in the report — practical contents for immediate use

- Forward-looking market model (2020–2032) with scenario toggles for demand shocks, raw-material price trajectories, and emissions-policy shifts.

- Risk heatmap and mitigation playbook that quantifies supplier and plant-level exposure to feedstock volatility, trade disruption and regulatory cost passthrough.

- Supplier intelligence matrix: comparative profiles, capability assessments, and operational risk indices for the global top-tier producers and selected regional champions.

- Commercial negotiations toolkit: benchmark terms, contractual language for feedstock pass-through and volume-flex clauses, and model RFPs to accelerate sourcing cycles in 2026.

- Technology and product roadmap: which refractory chemistries and shapes are moving from lab to scale, with cost/benefit guidance for adoption versus retrofit.

- M&A and capex decision framework: returns-on-capacity and integration checklists tailored to consolidation, greenfield and brownfield options under current policy scenarios.

- Executive dashboards and downloadable data packs for board-level briefings and cross-functional planning exercises.

Competition landscape — who matters and why

The competitive field balances global integrators with highly capable regional specialists. Our analysis highlights ten companies that define the market’s strategic contours — each with distinct positioning that informs partnership and procurement choices in 2026.

- RHI Magnesita (Vienna) — A vertically integrated global leader. Strengths: breadth of shaped refractories, scale in magnesia-carbon and high-alumina bricks, and investments in decarbonization initiatives. Strategic implication: preferred partner for large steelmakers seeking lifecycle cost reductions and integrated supply commitments.

- Vesuvius PLC (London) — Focused on high-performance bricks for metals and foundry sectors. Strengths: specialized engineering solutions and close metallurgical partnerships. Strategic implication: fit for customers prioritizing performance over commodity pricing.

- Shinagawa Refractories (Tokyo) — Japanese manufacturing excellence with global exports. Strengths: consistent quality and premium product lines. Strategic implication: reliable supplier for high-spec furnace linings and aftermarket support.

- Saint-Gobain Performance Ceramics & Refractories (Courbevoie) — Advanced ceramics and specialty fused products for demanding applications. Strategic implication: supplier of choice where thermal shock and corrosive environments demand higher-capability bricks.

- Krosaki Harima (Kitakyushu) — Deep Asia-Pacific footprint. Strategic implication: strong regional partner for steelmakers with local sourcing preferences.

- IFGL Refractories (Kolkata), HarbisonWalker (Moon Township), Resco Products (Pittsburgh), Puyang Refractories (China), and Chosun Refractories (South Korea) — collectively reflect a mix of regional leadership, custom manufacturing capability, and growing export orientation. Strategic implication: these players are vital for flexible supply, regional risk mitigation, and cost-competitive sourcing.

Market concentration metrics indicate a moderately fragmented market with room for further consolidation by scale players and targeted bolt-on acquisitions. In practice, the combination of feedstock exposure and differentiated product portfolios makes both horizontal and vertical deals attractive to incumbents and financial sponsors alike.

Recent developments and policy context to watch in 2026

- Selective capacity and inventory moves: recent plant expansions and targeted acquisitions by regional players underscore a deliberate shift to shorten lead times and capture aftermarket service margins.

- Climate and emissions regulation: EU directives on fired ceramic manufacturing and uneven national approaches to industrial emissions introduce compliance costs that favor suppliers with low-emissions production pathways or localized production near key markets.

- Raw-material trade dynamics: changes to import duties in major mineral-exporting countries and persistent alumina/magnesia price swings are reconfiguring cost curves and logistical preferences for both producers and buyers.

- End-market drivers: continued high global steel production maintains baseline demand for high-temperature linings, while electrification and alternative ironmaking routes create new product-service opportunities.

Strategic implications and 2026 playbook

For executives mapping 2026 plans, our brief crystallizes five immediate imperatives:

- Make feedstock strategy central. Reassess contracting models to incorporate indexed pricing, staggered volumes, and strategic stockpiles to buffer spikes that materially erode margins.

- Prioritize supplier capability over unit price. Where furnace uptime and throughput matter, total cost of ownership favors technically advanced bricks and service-oriented suppliers with rapid exchange and installation capacity.

- Accelerate decarbonization as a competitive lever. Investments that reduce process emissions or enable participation in carbon-credit programs produce both regulatory resilience and buyer differentiation.

- Design for optionality. Maintain a two-tier supplier base combining global integrators for scale and regional specialists for responsiveness — and embed contractual flex that allows rapid repricing or volume rerouting under stress scenarios.

- Targeted inorganic moves offer asymmetric returns. For corporates and PE, bolt-on acquisitions that close gaps in refractory chemistry or expand regional service networks are higher-conviction plays than broadscale greenfield builds in the current policy environment.

How PW Consulting supports execution

Our brief is intentionally crafted as a decision accelerator: it combines a transparent market model, supplier and cost diagnostics, scenario-ready playbooks, and step-by-step implementation templates for procurement, operations and corporate development. Subscribers receive an interactive data pack and can license bespoke advisory work — from rapid due diligence on M&A targets to a tailored sourcing redesign for 2026 rollouts.

We deliberately avoid publishing granular segment tables and regional splits in this release to preserve the tactical value of our modeling. The complete dataset — including segmented forecasts, supply curves by chemistry, and plant-level exposure maps — is available through the full report and consulting engagements.

Next steps

Decision-makers preparing strategic moves in 2026 should request a briefing copy of the PW Consulting refractory bricks brief and schedule a rapid-read workshop. Our team will overlay your enterprise footprint on the market model, quantify exposure, and present a prioritized list of actions calibrated to cost, schedule and regulatory risk tolerances.

Contact PW Consulting to book a briefing and access the full report, datasets and advisory options.

For detailed analysis of this topic, please visit the official page:Refractory Bricks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com