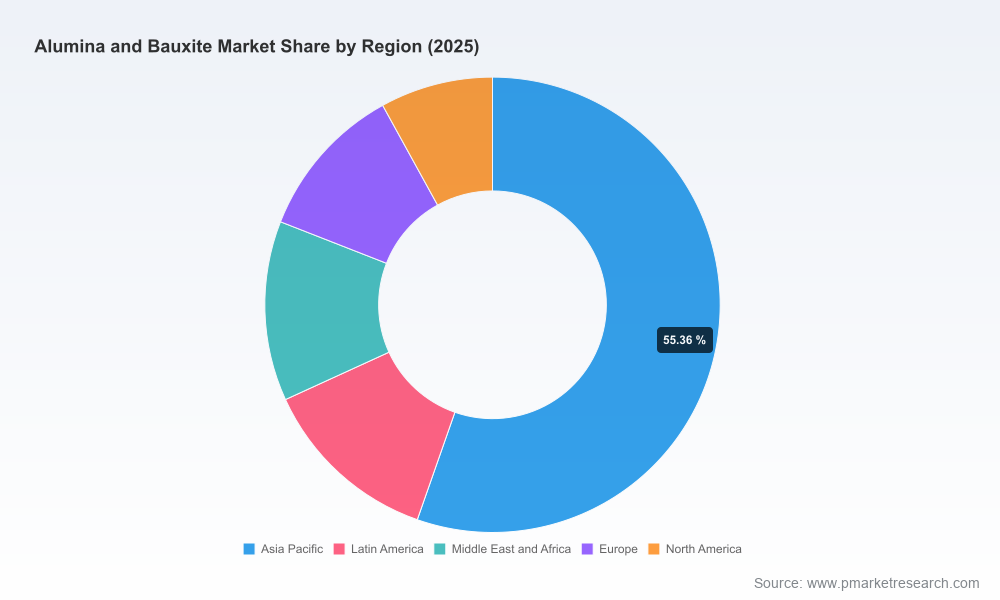

Alumina And Bauxite Market 2026 Strategic Brief: Actionable Intelligence for Boardroom Decisions

PW Consulting’s new Alumina And Bauxite Market report (base year 2025; historical 2020–2025; forecast 2026–2032) delivers a compact, decision-focused intelligence package designed to support CEO, CPO and Strategy teams as they set direction for 2026. The global market reached approximately USD 92.5 Billion in 2025 and, under our central case, is projected to expand at a 4.5% CAGR to roughly USD 126 Billion by 2032. This brief highlights the report’s strategic value, key directional signals shaping near-term choices, and the practical levers executives should prioritize. Detailed segment-level datasets and plant‑level schedules are intentionally reserved for the full report to drive direct engagement and protect competitive insight.

Alumina And Bauxite Market

Why this report matters for 2026 decision cycles

- Board- and C-suite-ready synthesis of supply, demand and price dynamics that matter for FY26 budgeting, capex gating and procurement strategy.

- Scenario-ready forecast logic that connects macro demand drivers to refinery throughput, bauxite mine ramp timelines and commercial outcomes under alternative policy and price shocks.

- Practical commercial playbooks (negotiation levers, offtake clauses, inventory sizing rules) that translate market intelligence into immediate procurement and sales actions.

- Integrated ESG and compliance pathways—covering chain-of-custody certifications and regulatory risk—that align decarbonization investments with market access and contract terms.

Data-driven signals and near-term drivers (what executives need to watch)

- Capacity additions and operational restarts: New refinery tonnage that came online in 2025 has already altered regional availability patterns. These discrete capacity moves create windows of supply arbitrage and re-pricing risk for spot and contract markets.

- Price momentum and margin pressure: Prices firmed through 2025 relative to 2024, tightening margins for downstream smelters where pass-through mechanisms are weak. This dynamic amplifies the need for flexible sourcing and indexed contract clauses.

- Policy and trade shocks: Trade measures and rising protectionist pressure have introduced additional complexity into supplier selection and landed-cost forecasting. Procurement teams must embed policy scenarios into near‑term sourcing decisions.

- Geopolitical and operational disruptions: Conflict-driven operational constraints in the Gulf region led to contract force majeure notices in early 2026, underscoring the value of diversified logistics corridors and contingency stock strategies.

- Certification and sustainable sourcing: Growing buyer preference for certified chain-of-custody and low-carbon alumina is reshaping commercial terms. Early movers with certified supply chains are gaining access to premium contracts.

- Corporate results as a real-time barometer: Public company reporting in Q1 2026 already shows the alumina segment reacting to shipment variability and realized price swings—an early indicator for downstream contract negotiations and inventory posture.

What the PW Consulting report delivers (practical modules)

- Executive snapshot: Single-page decision memo linking market outlook to strategic actions for 12, 24 and 36-month horizons.

- Demand-supply model: Transparent build-up of global demand drivers, refinery and mine throughput, and an adjustable forecast engine for in-house scenario testing.

- Price and margin scenarios: Three calibrated scenarios (base, upside, stress) with implied price-paths and margin impacts for buyers and sellers.

- Project and capacity tracker: Commissioning dates, phased ramp assumptions and sensitivity to delays—delivered at plant level in the full dataset.

- Commercial playbook: Recommended offtake structures, indexation and renegotiation triggers tailored to alumina and bauxite contracts.

- Risk and resilience map: Supply‑chain heatmaps and contingency playbooks for logistics, geopolitical and regulatory disruptions.

- ESG & certification pathway: Cost-benefit framework for ASI-style certifications and low‑carbon alumina sourcing aligned with market access and premium capture.

- Competitive profiles & transaction screen: Strategic positioning, capacity footprints and near-term moves for the industry’s leading producers and traders (full profiles in report).

Competitive landscape — who matters and why

The industry structure remains defined by integrated producers that own positions across bauxite mining, alumina refining and aluminum smelting, alongside regional players focused on supply security and scale. The following outlines strategic implications for 2026 decision-making.

Alumina And Bauxite Market

- Alcoa Corporation — An integrated footprint with sizable third‑party alumina sales. Recent Q1 2026 earnings revealed the alumina segment is susceptible to shipment variability and realized price pressure. For corporates, Alcoa’s public disclosures act as a near‑term barometer of refinery utilization and third‑party availability.

- Aluminum Corporation of China (CHALCO) — Large integrated refining capacity and domestic scale give CHALCO strategic pricing influence in key Asian corridors. Companies negotiating long-term supply in Asia should model CHALCO response options when constructing contract corridors.

- Rio Tinto — Broadly integrated mining-into-refining assets with global logistics reach. Rio’s asset base is a critical node for customers seeking vertically integrated security and for potential partnership or JV opportunities.

- United Company RUSAL — A major integrated supplier whose strategic moves can influence regional supply balances. Trade dynamics and policy risk should be explicitly modeled when interacting with assets exposed to shifting regulatory environments.

- Norsk Hydro (Alunorte) — Home to one of the largest single-refinery footprints. Capacity concentrated in a handful of large plants means operational events here have outsized influence on spot availability and pricing.

- Emirates Global Aluminium (EGA) — Regionally pivotal supplier; recent force majeure events during early‑2026 disruptions highlight how Gulf operations can tighten global supply chains and create short-run dislocations.

- Hindalco — A strategically integrated Indian producer; important for regional supply decisions and for companies assessing exposure to the world’s growing regional demand centers.

- South32 — Focused on sustainable mining and alumina operations, with an emphasis on environmental performance that appeals to buyers with strict supply‑chain requirements.

- China Hongqiao Group — Rapid capacity expansion, including new lines outside China, has implications for competitive pricing and regional sourcing strategies, particularly in Southeast Asia.

- Century Aluminum — Minority interests in downstream refining assets make it a relevant partner in joint-ventures and offtake negotiations rather than a pure merchant player.

Strategic imperatives for 2026 executives

- Diversify sourcing across supplier types and geographies, with explicit contingency pathways for Gulf and concentrated-refinery disruptions.

- Introduce flexible offtake structures: combine indexed contracts, volume flexes and short-term lots to balance security and price exposure.

- Prioritize certification and low-carbon alumina in customer negotiations where premium access or market entry depends on chain‑of‑custody credentials.

- Embed policy and tariff scenarios into landed-cost models and procurement KPIs to avoid stop‑start sourcing outcomes.

- Adopt staged capex and modular investments in refining and refining-adjacent processing to limit exposure to single-point failures.

- Use competitive profiles to identify JV or M&A targets that supply-secure but are under‑monetized in strategic corridors.

- Operationalize a three-tier inventory strategy: transactional, tactical (for predictable cycles), and strategic (for system shocks).

How PW Consulting supports execution

Our report is paired with a set of advisory services and deliverables designed to shorten the time from insight to action:

Alumina And Bauxite Market

- Interactive forecast model and scenario workshop for leadership teams to stress-test strategic options against alternative supply and policy paths.

- Vendor and counterparty due-diligence packages, including site-level operational risk assessments and certification roadmaps.

- Commercial negotiation templates and clause libraries tailored to alumina and bauxite offtake contracts, including escalation and force‑majeure articu-lations.

- Custom dashboards integrating client procurement systems with our price and capacity feeds for rolling 12‑month decision cycles.

PW Consulting’s Alumina And Bauxite Market report is intentionally constructed to be both a strategic compass and a practical toolkit. The core market numbers signal a healthy expansion trajectory through 2032, but the path is neither linear nor uniform: policy shifts, refinery start-ups and geopolitical events will create episodic dislocations and opportunity windows. For executives planning 2026 actions—procurement renegotiations, capex approval, partnership selection or ESG investments—this report translates market complexity into prioritized, executable steps. To access the full dataset, plant-level schedules, and the detailed segmentation tables that drive the playbooks in this brief, please consult the full PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Alumina And Bauxite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com