Creatinine Measurement Market Overview: Future Growth Potential and Key Industry Highlights

Health |

2026-06-22 13:44:50

PW Consulting’s latest market study on Norbornane Diisocyanate (NBDI) is released with a clear mission: to equip boardrooms, corporate strategy teams, procurement leaders, and R&D heads with the forward-looking evidence they need to make high‑stakes decisions in 2026. Built on a 2025 base year and a 2026–2032 forecasting horizon, the study synthesizes historical performance (2020–2025) and projects the market forward at a compound annual growth rate of 5.24%. In dollar terms (USD Million), the market is modelled to expand from USD 248.66 million in 2025 to roughly USD 355.52 million by 2032, reflecting steady, structurally supported growth rather than a speculative boom.

Norbornane Diisocyanate (NBDI) Market

Timing matters. The 2026 planning cycle is the pivot point between near-term supply commitments and multi-year capital allocations. With a predictable mid-single-digit CAGR and discernible application-driven demand, companies that crystallize their strategy in 2026 can lock in advantaged cost positions, secure feedstock access, and shape product roadmaps that capture the most valuable pockets of growth.

Norbornane Diisocyanate (NBDI) Market

Market structure amplifies impact. NBDI is a specialty aliphatic diisocyanate with a compact, rigid bicyclic backbone that gives it distinct performance advantages in optical, coating and elastomer applications. The commercial market is highly concentrated among a very small number of suppliers, creating both pricing discipline and supply fragility—a combination that rewards proactive commercial and supply‑chain strategies.

Norbornane Diisocyanate (NBDI) Market

Regulation and legitimacy. NBDI is registered in major inventories (e.g., TSCA, DSL, ECL), and has an established toxicological profile documented in public chemical reference sources. That regulatory visibility reduces time-to-market friction for established suppliers but raises the bar for newcomers on compliance, testing, and handling requirements.

Market sizing and high‑granularity forecasting (2023–2032): trend decomposition by demand drivers and pricing dynamics, with scenario modelling that quantifies downside and upside pathways for 2026 strategic options.

Commercial and technical deep dives: property-by-property comparisons that explain why NBDI’s rigid bicyclic structure is particularly attractive for optical lenses, specialty coatings and high‑performance elastomers; technology readiness assessments for formulation adoption.

Supply‑chain heatmaps and feedstock risk analysis: end‑to‑end mapping from norbornene feedstocks (synthesized via classic Diels–Alder routes from cyclopentadiene precursors) through isocyanation and commercial distribution nodes, with choke‑point identification and mitigation playbooks.

Regulatory & EHS matrix: inventory listings, documented toxicity endpoints, and practical recommendations for handling, worker protection and local registration timelines—critical for firms planning plant expansions or new market entries.

Competitive landscape and commercial diligence templates: capability matrices, go‑to‑market vectors, and M&A screening criteria calibrated to a market where a handful of players dominate supply.

Actionable annexes: sample long‑term offtake agreements, tolling contract templates for captive or outsourced production, and costing models you can adapt for internal investment decisions.

Market concentration creates leverage and vulnerability. The NBDI market is controlled by a very small number of commercial producers, resulting in concentrated supply. For buyers, this concentration means that a single supplier disruption or pricing reset can materially change margin dynamics across downstream value chains.

Profile — Mitsui Chemicals, Inc. As the primary commercial producer and a de‑facto benchmark supplier, Mitsui Chemicals (HQ: Tokyo) commands both technical know‑how and established customer relationships. Their positioning—focused on high‑performance specialty aliphatic diisocyanates for polyurethane elastomers, optical applications and advanced coatings—sets the commercial reference for quality, purity and technical support.

Implication for rivals and newcomers. New entrants face a double hurdle: securing precursor feedstock and demonstrating strict quality and regulatory compliance. Successful challengers will need to combine a differentiated technical proposition (e.g., unique formulation support for optical systems), vertical integration into precursors, or creative commercial models such as toll manufacturing or exclusive regional partnerships.

Feedstock chains matter. NBDI’s bicyclic backbone is typically derived from norbornene-related precursors synthesized through Diels–Alder chemistry involving cyclopentadiene. That chemistry is well‑understood but concentrated in regional production hubs for certain intermediates; a price spike or capacity constraint at the precursor level can cascade rapidly through the NBDI supply chain.

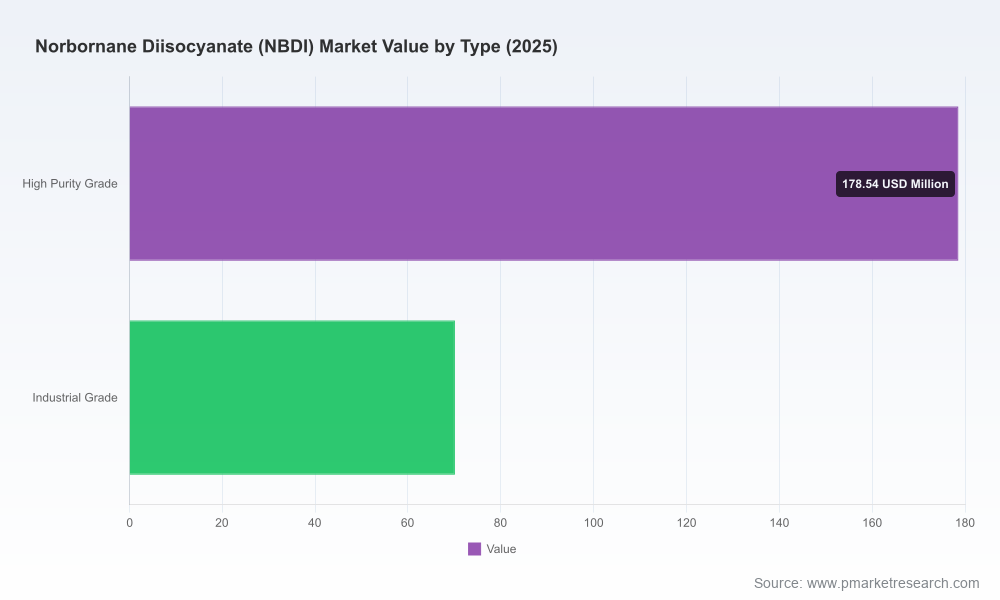

Application pull is selective and value-driven. Adoption is strongest where NBDI’s mechanical rigidity and aliphatic nature provide clear value—optical lenses, specialty coatings with UV/colour stability requirements, and high‑performance elastomers. These are not commodity use cases; they are premium niches that can sustain higher price points for high‑purity grades and technical support.

Regulatory clarity reduces market friction but raises compliance costs. The listing of NBDI on major inventories and the public availability of toxicity data streamline commercial adoption for established suppliers, while simultaneously requiring robust documentation, registration steps for new producers, and careful EHS planning for site expansions.

Procurement & supply security: move from spot reliance to a tiered sourcing strategy. Combine negotiated medium‑term contracts with strategic safety stocks and collaborative forecasting with your primary supplier(s). For critical optical and coating programs, secure contractual quality specifications (e.g., purity grades, impurity limits) and service level agreements that include ramp commitments.

Manufacturing and CAPEX: scrutinize the economics of backward integration versus tolling. Given the specialized precursor chemistry and regulatory overhead, many firms will find toll manufacturing or licensed production more capital‑efficient in the 2026 horizon—unless scale and cost of capital justify vertically integrated builds.

R&D and product strategy: prioritize formulation pilots that exploit NBDI’s rigid bicyclic structure for performance differentiation—optical clarity, coating hardness and reduced yellowing. High‑purity grades command a premium; quantify the margin uplift and route-to-market for value capture.

M&A and partnerships: screen targets that provide either feedstock security (norbornene intermediates), regional distribution reach, or specialty downstream outlets (optical manufacturing, high‑end coatings formulators). In a concentrated supplier market, M&A can be an effective way to hedge supply risk and accelerate route-to-market.

Regulatory & EHS: adopt a compliance-first posture. Ensure registration timelines are built into any market entry plan, and invest in worker safety protocols and monitoring systems that meet the highest jurisdictional standards—this limits commercial disruption and reputational risk.

Base case (PW Consulting reference): steady expansion at c.5.24% CAGR to 2032, driven by premium application growth and incremental adoption in specialty coatings and optics.

Upside triggers: accelerated adoption of NBDI in adjacent high‑value applications (e.g., next‑gen optical polymers), successful capacity additions by secondary producers, or feedstock cost declines that improve commercial economics.

Downside triggers: precursor supply shocks, abrupt regulatory tightening in large end‑use markets, or a rapid substitution by a lower‑cost aliphatic diisocyanate with acceptable performance. Our scenario models quantify these outcomes and prescribe tactical responses for each.

Leading indicators to monitor in 2026: precursor pricing trajectories, announcements of new synthetic routes or capacity, regulatory consultations affecting handling/registration, and long‑term offtake contract activity among major OEMs in optics and coatings.

Use the report as a playbook for procurement negotiations: the included pricing models and break‑even analyses allow procurement teams to test counterfactuals and structure resilient contracts for 24–36 month horizons.

Leverage the technical annexes for R&D prioritization: the formulation guidance and property benchmarking accelerate internal development timelines and improve success rates for pilot programs.

Adopt the M&A screening templates for disciplined growth: our valuation sensitivity tables and commercial due diligence checklists reduce execution risk and highlight integration milestones that matter most post‑close.

Note on disclosure and next steps: this briefing intentionally highlights strategic conclusions and the practical uses of the research while preserving the detailed segment tables, company revenue breakdowns, and Excel datasets for the full report release. Those granular data — including regional, grade and application-level splits, and company-level financial proxies — are available exclusively in the full PW Consulting Norbornane Diisocyanate (NBDI) Market Report and accompanying dataset.

For corporate strategy teams preparing 2026 budgets, R&D leaders building pilot portfolios, or investors screening specialty chemical targets, this report is designed as a compact, executable toolkit. Contact PW Consulting to access the full report and supporting datasets, and to arrange a tailored strategy workshop that maps these insights to your portfolio and operating context.

For detailed analysis of this topic, please visit the official page:Norbornane Diisocyanate (NBDI) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com