North America Ambulatory Surgery Center Services Market Outlook

Other |

2026-07-06 12:10:18

PW Consulting today publishes an executive briefing framing the strategic implications of our in-depth market study on the global 5G radome market. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the market has more than doubled since 2020 and is projected to sustain a robust compound annual growth rate (CAGR) of 13.0% through the forecast period. Our analysis combines granular supplier intelligence, technology roadmaps, regulatory and infrastructure dynamics, and scenario-based forecasts to help C-suite executives, product leaders, network planners, and investors make high-conviction decisions in 2026.

5G Radome Market

Two converging forces make 2026 a pivotal year for radome-related decisions. First, telecom operators and neutral-host providers are moving from pilot and densification towards wide-scale deployments of mmWave and mid-band capacity — a phase where enclosure design and materials selection materially affect RF performance, operational resilience, and lifecycle costs. Second, regulatory and capital dynamics (including expedited permitting proposals and looming spectrum auctions) are compressing deployment timetables, forcing procurement and supply-chain choices earlier in the planning cycle.

5G Radome Market

Market momentum: After a steady rise over 2020–2025, the total market is expected to continue accelerating — presenting both growth opportunities and new execution risks related to manufacturing scale-up and material sourcing.

5G Radome Market

Time-to-deploy sensitivity: With spectrum allocation and permitting timelines moving faster, early vendor selection and radome-qualification programs will determine who meets network launch windows in 2026–2027.

Cost leverage: Radome choices are non-trivial in capital planning; they interact with base station economics where a single macro or small-cell site can represent meaningful incremental costs within overall 5G CapEx budgets.

Our historical dataset (2020–2025) documents a compound acceleration in demand driven by both outdoor macro rollouts and densification of urban small cells. The market size midpoint in 2025 provides a baseline from which the 2026–2032 forecast is built; by 2032 the market is projected to reach a substantially higher level, reflecting continued densification, mmWave adoption, and replacement cycles for legacy enclosures. At a 13.0% CAGR over the forecast window, suppliers and buyers must plan for multi-year supply commitments and technology roadmaps that balance RF transparency, durability, manufacturability, and cost.

Concentration metrics are instructive: the top three suppliers account for roughly 42% of the market, while the top five account for about 59%, indicating a market that is neither highly fragmented nor tightly monopolized. This structure favors strategic partnerships, targeted M&A, and differentiated product strategies rather than pure cost competition.

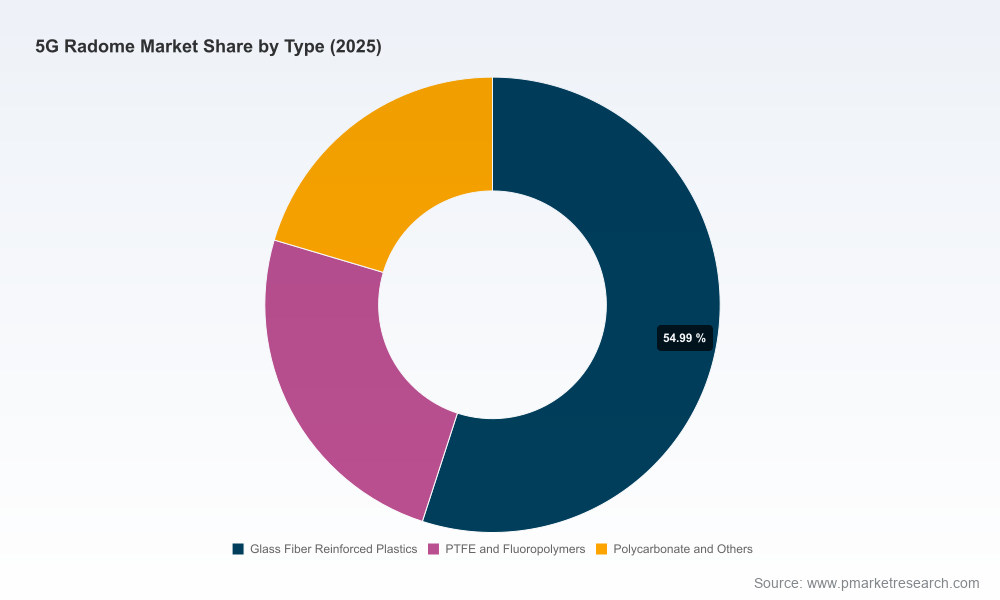

Technology-driven demand: Increasing mmWave and mid-band deployments push radome performance requirements (low-loss, wide-angle RF transparency) and favor engineered composites, advanced thermoplastics, and sandwich-core constructions.

Infrastructure capital flow: With global 5G CapEx having reached significant scale by 2025, radome demand is correlated with network spend cycles. Procurement teams should align radome sourcing with multi-year CapEx profiles to avoid supply shocks.

Permitting and spectrum catalysts: Regulatory steps to accelerate infrastructure deployment and planned mid-band auctions are accelerating rollout timelines; meeting those timelines depends on pre-qualified radome inventories and rapid certification processes.

Material and logistics pressures: Rising costs for fiber backhaul and imports, along with labor inflation, have increased downstream deployment costs and put a premium on radome designs that simplify installation and reduce O&M touchpoints.

Our competitive review synthesizes company-level strengths, product trajectories, and strategic moves by incumbent and specialist suppliers. The market is populated by large infrastructure suppliers and focused composites specialists; each segment plays distinct roles in network rollouts.

CommScope (United States) — A systems-scale supplier offering antenna enclosures engineered for telecom infrastructure. CommScope’s scale and aftermarket support make it a default option for nationwide operators seeking integrated solutions.

Exel Composites (Finland) — A product engineering leader with patented composite radome designs targeted at reducing signal attenuation — a differentiator for mmWave and challenging RF environments. Exel’s IP position makes them a strategic partner for operators prioritizing performance over unit cost.

Saint‑Gobain (France) — Brings materials- and systems-level expertise (e.g., SHEERGARD solutions) across laminate, sandwich, and fabric systems. Their capability to pair hydrophobic and mechanical properties appeals to harsh-environment deployments.

General Dynamics Mission Systems (United States) — Legacy strength in protective radomes for high-frequency applications; their defense and aerospace pedigree provides rigorous qualification processes transferable to mission-critical telecom infrastructure.

Laird Connectivity (United States) — Recent product innovation (Radome5™ Poly) emphasizes injection-molded thermoplastic solutions tailored for indoor mmWave and small-cell equipment, signaling a move toward faster, lower-cost manufacturing for certain use cases.

Material and component specialists — Firms such as Diab Group and a set of regional composite manufacturers supply core materials and fabrication capability, influencing total-cost-of-ownership and production lead times.

Regional manufacturers and integrators — A broad band of specialist and regional firms address custom designs and repair services, offering agility where global suppliers may be constrained by lead times.

Recent developments underscore the pace of innovation: Laird Connectivity’s October 2025 launch of an injection-molded polyolefin solution highlights an engineering pivot to manufacturability for indoor mmWave applications, while patent activity from Exel Composites in 2025 signals ongoing performance-driven differentiation. These moves hint at bifurcation in the market: manufacturability and unit-cost optimization for high-volume small-cell deployments versus differentiated composite solutions for high-performance or harsh-environment installations.

Our full report is structured to serve procurement lead times and product strategy cycles in 2026. It combines forecasting, supplier due diligence, and playbooks that teams can apply immediately:

Market sizing and scenario models calibrated to operator CapEx cycles and regulatory timelines, with sensitivity analyses for spectrum auction outcomes and permitting acceleration.

Supplier scorecards that evaluate RF performance, manufacturing footprint, qualification timelines, IP posture, and aftermarket capability — enabling rapid shortlist creation for RFPs.

Product-matrix guidance identifying when to favor composite versus thermoplastic approaches based on deployment profile, environmental exposure, and lifecycle cost targets.

Supply-chain risk maps highlighting material bottlenecks, tariff exposure, and logistics constraints — with contingency playbooks for near-term procurement (including strategic inventory and multi-sourcing strategies).

Regulatory and spectrum impact briefs that translate FCC actions and mid-band auction timelines into procurement and deployment milestones.

Pre-qualify dual tracks: Operators should pre-qualify both performance-optimized composite vendors and high-throughput thermoplastic suppliers to match site typologies and speed-to-deploy requirements.

Lock in modular standards: Specify modular radome interfaces and common mechanical footprints to reduce SKU proliferation and accelerate field swaps during rapid rollouts.

Pursue strategic inventory for critical nodes: Given potential material or logistic disruptions, establish buffer inventories for high-impact sites where downtime is costly.

Embed test and certification early: Accelerate RF acceptance testing and environmental qualification during vendor selection to avoid downstream retrofit costs.

Monitor regulatory timelines as program gates: Treat spectrum auction and permitting milestones as hard program gates that should trigger procurement tranche releases and vendor ramp targets.

The market structure implies consolidation opportunities for buyers seeking scale in manufacturing or IP-led performance differentiation. Target profiles that create vertical leverage (materials + radome assembly) or expand geographic manufacturing footprints will be especially attractive as operators prefer single-vendor, fast-qualify solutions for mass deployments.

2026 is a planning inflection: operators will finalize budgets linked to spectrum allocation and permitting cadences, while suppliers must convert innovation into scalable manufacturing. The PW Consulting brief provides the tactical playbook — supplier shortlists, procurement timing matrices, and risk mitigations — needed to align procurement, engineering, and regulatory teams ahead of execution windows.

To preserve the strategic advantage for our clients, this public briefing deliberately highlights insights and recommendations while withholding certain segment-level breakdowns and proprietary forecasts. For full access to the detailed segmentation, vendor scorecards, and downloadable scenario models that underpin the forecast and tactical playbooks, visit our report page or contact PW Consulting’s industry desk.

For detailed analysis of this topic, please visit the official page:5G Radome Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com