Raspberry Hills || Raspberry Hills Clothing Store || 40% Off

Gardening |

2026-04-29 07:20:23

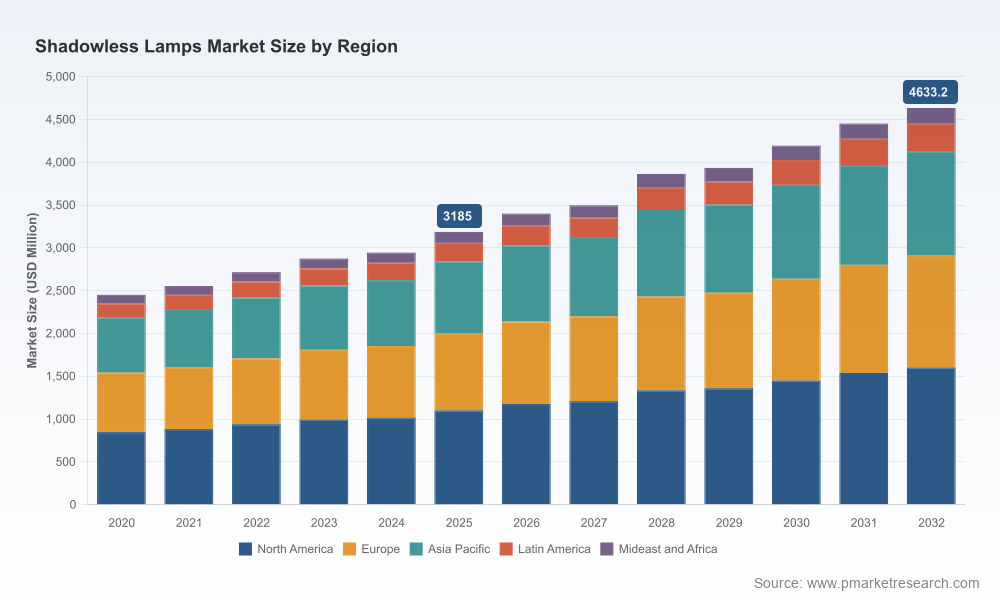

As health systems accelerate operating room (OR) modernization and surgical practice shifts toward hybrid, image‑intensive workflows, the shadowless lamps market is evolving from a product sale into a platform play. PW Consulting’s latest Shadowless Lamps Market report — grounded in historical observations (2020–2025) and a forward forecast (2026–2032) — shows the market expanding from roughly USD 2.45 billion in 2020 to USD 3.19 billion in 2025, with a projected rise toward the mid‑2030s and an expected compound annual growth rate of approximately 5.5% across the forecast window. For executives making procurement, product, and investment decisions in 2026, this report translates those macro trends into operational choices that affect total cost of ownership, OR throughput, and long‑term strategic positioning.

Shadowless Lamps Market

Timing of CapEx: With steady single‑digit growth and accelerating technology integration (in‑light cameras, wireless connectivity, software orchestration), procurement teams must balance legacy replacement cycles against modular upgrade paths to avoid stranded assets.

Shadowless Lamps Market

Platform vs. Point Solution: Leading OEMs are shifting toward modular, serviceable lighting platforms that support imaging, data capture, and interoperability. Hospitals buying in 2026 should prioritize upgradeable systems that preserve optionality for 4K/AI workflows.

Shadowless Lamps Market

Operational ROI: The value of lighting systems is increasingly argued through procedural efficiency, staff ergonomics, and documentation capability rather than lamp lumen figures alone. This reframes procurement evaluation metrics—from purchase price to operational impact over a 7–10 year life cycle.

Decision frameworks: A procurement playbook with stepwise evaluation criteria that translate clinical needs into a prioritized feature set (imaging readiness, shadow management strategy, color rendering, heat mitigation, lifecycle cost).

TCO and CapEx modeling: Interactive cost models that quantify purchase, installation, energy, maintenance, and upgrade costs across plausible 7–10 year lifecycles under different utilization scenarios.

Regulatory and compliance checklist: Practical guidance for Class II medical device pathways, including FDA 510(k) considerations and IEC 60601 electrical safety requirements, plus change‑control advice during retrofits and system integrations.

Technical adoption roadmaps: Stepwise guides for integrating 4K in‑light cameras, wireless telemetry, and OR system connectivity, including recommended API patterns and vendor negotiation points to preserve future interoperability.

Vendor scorecards and procurement RFP templates: Qualitative and quantitative evaluation matrices covering service SLA expectations, upgrade economics, spare‑parts logistics, and cybersecurity controls for connected devices.

M&A and partnership heatmaps: Investor‑grade screens that identify targets aligned to modular LED optics, imaging capability, and regional manufacturing footprints, drawing attention to consolidation levers.

Clinical impact cases: Evidence summaries linking lighting features to surgical visualization, ergonomics, and theater throughput — oriented to support value arguments in capital committees.

Regulatory environment: Surgical lights are regulated as active medical devices that must meet FDA 510(k) pathways in the U.S. and comply with IEC standards globally. These frameworks emphasize electrical safety, electromagnetic compatibility, and software lifecycle controls — all of which affect time‑to‑market for enhanced features such as in‑light imaging.

Technology integration: The rapid integration of 4K cameras, wireless connectivity, and intelligent lighting control is converting lighting fixtures into data capture and imaging nodes in the OR. This creates new revenue streams (service, software) but also raises requirements for cybersecurity, data governance, and standards‑based interoperability.

CapEx and hospital behavior: Capital expenditure allocations are shifting toward systems that can demonstrably improve OR utilization. LED systems continue to be favored for energy efficiency, reduced thermal footprint, and lower lifecycle maintenance — attributes that accelerate replacement cycles in modernizing facilities.

Reimbursement and procurement context: Lighting systems are typically capitalized at the facility level rather than reimbursed at a per‑procedure rate. Procurement decisions therefore pivot on operational efficiency gains and risk mitigation rather than procedure‑specific reimbursement incentives.

The market remains anchored by an established set of global OEMs increasingly complemented by cost‑competitive regional manufacturers. Market value is concentrated among a handful of global players that combine product breadth with service networks, while agile entrants specialize in modular technologies and regional manufacturing efficiency. In practical terms, top global suppliers capture a material share of the market, but the landscape also leaves room for niche innovation and regional consolidation — a dynamic that creates both defensive and acquisitive strategies for incumbents and newcomers.

Stryker Corporation — Known for high‑performance platforms, Stryker’s recent Oculan Lighting Platform and SHD Mode underscore a strategy focused on surgical visualization consistency and modular feature sets suitable for integrated ORs.

TRUMPF Medical (Hillrom/Baxter) — TRUMPF’s iLED and TruLight series emphasize multi‑lens matrices and adaptive light management, targeting procedures where consistent, shadow‑free fields matter across surgical types.

STERIS plc — STERIS combines LED systems with media and camera integration, appealing to health systems seeking unified OR vendor relationships that bundle lighting with broader operative infrastructure.

Getinge (Maquet), KLS Martin, Dräger — These European manufacturers emphasize optical quality, color fidelity, and ergonomics. Dräger’s Polaris series, awarded for design and performance, signals the growing importance of design‑led differentiation.

Mindray, Heal Force, Shanghai Huifeng, Jiangsu Yigao — Manufacturers based in China are increasing competitive pressure with cost‑efficient LED platforms and rapid product cycles, while extending export footprints into emerging markets and price‑sensitive segments.

Skytron — Focused on hospital OR ergonomics and visualization, positioning toward integrated room solutions that improve adoption frictions for busy procurement teams.

Recent product launches and recognitions — for example, Stryker’s 2024 Oculan launch and Dräger’s Polaris rollout and subsequent design award — highlight that differentiation is moving beyond raw lumen output toward integrated imaging, ergonomics, and serviceability.

Hospital executive teams: Prioritize upgradeable architectures and demand clear upgrade pathways in procurement contracts. Insist on interoperability, documented data flows for captured imagery, and lifecycle cost guarantees that include camera upgrades.

Procurement and clinical engineering: Use TCO modeling to compare legacy replacement vs. phased modernization; require OEMs to provide validated integration playbooks with PACS/AV vendors and OR management systems.

OEMs and suppliers: Invest in modular optics, embedded imaging capabilities, and remote service tooling. Monetize platforms through software subscriptions and service tiers while keeping hardware margins sustainable.

Private equity and strategic investors: Target consolidation candidates that offer complementary service networks, regional production scale, or promising imaging/software capabilities where integration barriers remain high.

Regulatory and compliance officers: Build device cybersecurity and software lifecycle management into procurement checklists today to avoid costly retrofit programs after deployment.

This briefing is a curated preview: it demonstrates the analytical depth and practical tools contained in the full Shadowless Lamps Market report while intentionally withholding detailed regional and application splits to preserve the value of the proprietary dataset. The full report includes granular segmentation, vendor scorecards, pricing benchmarks, region and application breakdowns, and downloadable financial models that allow scenario testing against local procurement constraints and clinical utilization profiles.

If your 2026 capital plans, product roadmaps, or investment theses depend on precise segmentation, vendor economics, or scenario‑level sensitivity testing, PW Consulting’s comprehensive dataset and advisory service translate market momentum into executable choices. Access to the full dataset and bespoke advisory engagements will fast‑track procurement approvals, inform M&A diligence, and sharpen product strategies for the fast‑moving OR ecosystem.

For a walkthrough of the model, a vendor benchmarking session, or to obtain the full report, please contact PW Consulting’s life sciences practice. Our granular financial models and implementation playbooks are designed to convert the market’s projected steady growth and technology inflection into measurable operational and strategic outcomes in 2026.

For detailed analysis of this topic, please visit the official page:Shadowless Lamps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com