US Legumes Market Trends: Production Volumes, Commercial Sizing, and 2034 Projections

Food |

2026-06-08 13:15:51

PW Consulting today publishes its new market research brief, "Air Permeability Tester Market — Strategic Outlook to 2032," delivering a focused, decision-ready synthesis of market dynamics that matter for corporate strategy in 2026. Authored by the firm’s Chief Industry Analyst, the brief translates comprehensive primary research and proprietary modeling into actionable guidance for equipment manufacturers, instrument OEMs, component suppliers, laboratory networks, and corporate procurement organizations.

Air Permeability Tester Market

After a steady recovery and structural expansion across testing-intensive end markets, the global air permeability tester market reached USD 237.4 Million in our base year (2025). Our forecast shows continued growth to USD 253.9 Million in 2026 and a projected expansion to approximately USD 337.4 Million by 2032, representing a compound annual growth rate (CAGR) of 5.15% over the 2026–2032 forecast period. These macro trends underscore an inflection point for strategic resource allocation in 2026: capital investment cycles, product roadmap prioritization, channel and service strategy, and M&A timing should all be evaluated in light of predictable, mid-single-digit market growth and evolving end-market requirements.

Air Permeability Tester Market

Trajectory: The addressable market has grown consistently from its 2020 baseline, driven by expanding quality regimes in technical textiles, filtration media, battery separators, medical PPE and regulated paper/board segments. The 2026 uptick reflects both organic replacement cycles and new testing demand as manufacturers accelerate in-line and at-line inspection.

Air Permeability Tester Market

Market structure: The industry exhibits moderate concentration; the top three players account for roughly one-third of market revenues, while the top five approach just under half of the total market — a structure that concurrently enables niche differentiation and leaves room for consolidation.

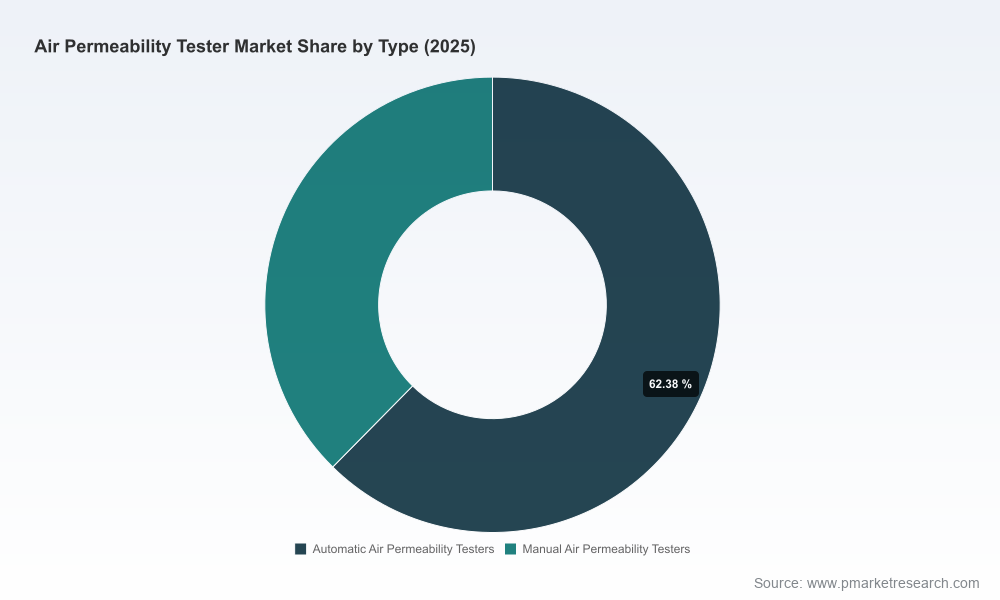

Hidden complexity: Aggregate figures mask important heterogeneity — instrument form factors (automatic vs. manual), testing methods (differential pressure, volume-based methods, spot/profile measurement), and compliance-driven demand arising from different standards regimes. Our full dataset decomposes these layers and maps them to revenue, growth rates, and technology adoption curves.

Standards and regulation: Global standards such as ISO 9237, ASTM D737 and sector-specific protocols (including paper and packaging standards) continue to set minimum functionality and reporting requirements. Compliance is a baseline gatekeeper for market access; differentiated value accrues to instruments that deliver automated compliance workflows, audit trails, and digital traceability.

Product complexity and component supply: High-precision differential pressure sensors, flow measurement modules and robust manometers are central cost and capability drivers. Firms that secure resilient sourcing, in-house calibration expertise, or preferred supplier status for critical sensors will enjoy a durable cost and quality advantage.

End-market performance demands: Textile and filtration manufacturers prioritize breathability and porosity metrics, while battery and membrane producers demand sub-micron sensitivity and specialized fixtures. Buyers increasingly prefer integrated testing solutions — combining spot, profile and online measurements — rather than standalone benches.

Service and digitalization: Predictive maintenance, remote diagnostics, and embedded analytics are becoming standard purchasing criteria for higher-value automated testers. Service revenue and recurring calibration contracts are consequential levers for margin expansion.

The competitive map is a mix of precision Swiss and North American engineering houses, established U.S. test-instrument brands, and nimble Chinese manufacturers serving mass-market and regional needs. The most consequential competitors combine rigorous standards compliance with differentiated go-to-market strategies.

TEXTEST AG (Schwerzenbach, Switzerland) — Renowned for high-precision instruments and profile/spot measurement systems. Strengths include R&D depth for technical textiles and filter media, and strong positioning around compliance with international standards.

Frazier Precision Instrument Company, Inc. (Hagerstown, Maryland, USA) — A de facto standard for airflow resistance testing across multiple materials. Product portfolio breadth (low- and high-pressure models, compact mobile systems) and entrenched application knowledge make Frazier a default choice for many industrial buyers.

Thwing-Albert Instrument Company (West Berlin, New Jersey, USA) — Offers cross-material solutions (textiles, paper/board) and a deep legacy in standards-driven instruments. The company’s eclectic device mix supports multi-segment customers requiring portfolio rationalization.

Labthink Instruments Co., Ltd. (Jinan, Shandong, China) — Focused on packaging and material permeation testing with models supporting both differential pressure and volume methods. Competitive on price-performance for large-scale packaging labs and contract testing organizations.

Wenzhou Darong Textile Instrument Co., Ltd. (Wenzhou, Zhejiang, China) — Longstanding supplier for textile and nonwoven testing with automated solutions targeted at high-volume fabric producers and protective clothing manufacturers.

SDL Atlas (Rock Hill, South Carolina, USA) — Positioned on affordability and standards compliance; appeals to smaller labs and cost-conscious quality teams, including mask and PPE testing per EN/ASTM requirements.

GESTER Instruments Co., Ltd. (Quanzhou, China) — Offers fully automatic models for woven, knitted, nonwovens and filters; competes on customizable automation and integration capability.

Qualitest International Inc. (Quebec, Canada) — Global reach with fast, reliable testers oriented to contract labs and manufacturers seeking rapid throughput with acceptable precision.

Recent product movements (for example, TEXTEST AG’s FX 3370 SpotAir exhibited in September 2024) illustrate two tangible trends: suppliers investing in spot/profile measurement capability to address heterogeneous fabric structures, and an intensifying race to offer modular, integrated testing platforms that can be deployed hand-held, at-line, or on production lines.

The PW Consulting report is built as a playbook for 2026 decision cycles. It delivers:

Validated, year-by-year market sizing (historical 2020–2025, base year 2025) and a granular forecast for 2026–2032 (USD basis and unit/volume indicators).

Segment and regional decomposition mapped to buyer personas and procurement triggers (note: detailed numeric splits by region, type and application are available in the full dataset).

Technology and component-sourcing risk matrix, including supplier concentration, long-lead items and substitution scenarios for critical sensor stacks.

Competitive intelligence dossiers with strategic positioning, pricing posture, channel footprints and product differentiation for primary vendors.

A 12–36 month decision roadmap — prioritizing product development bets, capital expenditure windows, service model redesign, and potential targets for bolt-on M&A or distribution partnerships.

Scenario planning modules that quantify the revenue and margin impacts of accelerating automation uptake, embedding analytics, or pursuing aggressive price-led expansion into emerging markets.

Prioritize modular automation: For OEMs and service providers, invest in modular platforms that scale from bench to online testing. Buyers increasingly reward solutions that reduce operator variability and provide audit-ready outputs.

Lock down sensor supply chains: Given the centrality of precision sensors and flow measurement subsystems, secure preferred-supplier agreements or dual-source strategies to mitigate supply risk and cost volatility.

Monetize services: Convert calibration and diagnostics into subscription streams. In a market with moderate concentration, services can be a differentiator that stabilizes margins as instrument competition intensifies.

Targeted M&A: Strategic acquisitions that add complementary automation, analytics capabilities, or regional distribution networks can be value-accretive — particularly where the acquirer can cross-sell into adjacent testing categories.

Embed compliance value: Instruments that simplify compliance with ISO, ASTM and sectoral standards will command premium pricing; invest in validated, audit-ready software and reporting features.

Procurement and strategy teams should treat our market curve and scenario modules as inputs into five discrete 2026 decisions: capital budgeting (testers vs automation), product roadmap prioritization (profile/spot vs volume methods), geographic expansion (where to deploy field service), M&A target screening, and service model design (calibration/subscription). The report converts each of those choices into quantified upside and downside cases tied to market growth, payback periods and sensitivity to component-price shocks.

This release is intentionally designed as a high-value preview. To preserve the strategic exclusivity of granular regional, application and model-level forecasts (which our clients rely on when making procurement, R&D and M&A decisions), the full dataset and vendor-level revenue splits are available via PW Consulting’s full report package. For access to the complete model, interactive scenario tools, and bespoke briefings for 2026 planning cycles, visit PW Consulting’s reports page or contact our market intelligence desk to request the Air Permeability Tester Market report and supporting Excel model.

PW Consulting remains committed to delivering concise, decision-grade intelligence that equips executives with the situational awareness and quantified options required to compete in a rapidly professionalizing testing ecosystem. Our next client roundtable on implementing these recommendations for 2026 trade-offs will be scheduled in Q1 2026; interested parties are invited to request participation when ordering the full report.

For detailed analysis of this topic, please visit the official page:Air Permeability Tester Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com