The Modern Gentleman’s Guide to Caribbean Leisure and Companionship

Party |

2026-06-15 16:14:53

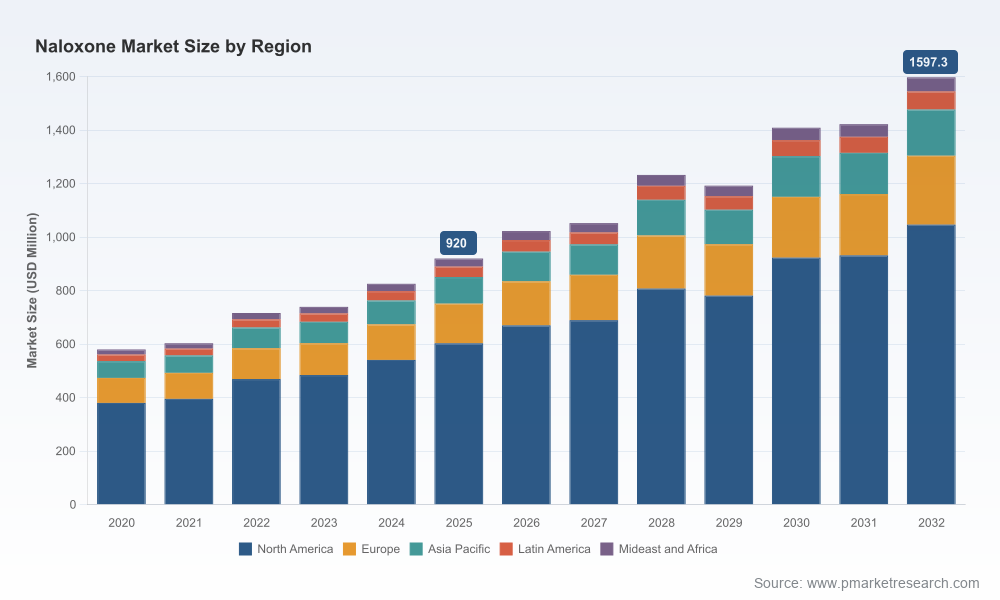

PW Consulting’s latest Naloxone Market report delivers a focused, decision-grade view of a market that has transitioned from a crisis-response commodity to a strategic healthcare asset. Valued at approximately USD 920 million in the 2025 base year, the global naloxone market is projected to grow at a compound annual growth rate (CAGR) of 8.2% through our 2026–2032 forecast horizon, reaching roughly USD 1.6 billion by 2032 under the base-case scenario. This trajectory reflects structural demand driven by regulatory liberalization, public-health procurement programs, and evolving private-sector access strategies.

Naloxone Market

This press release highlights the report’s strategic value for 2026 corporate planning while intentionally reserving granular segmentation tables and price decks for report subscribers. Consider this a concise trailer: deep enough to inform your agenda-setting conversations, but curated to prompt direct engagement with PW Consulting for transaction-level intelligence.

Naloxone Market

Regulatory normalization: The regulatory shift that enabled over‑the‑counter (OTC) naloxone access has redefined payer and retail economics. With OTC approvals and Medicare Part D reimbursement clarity already in place, 2026 will be the first full operational year in which commercial channels and public programs execute at scale under new rules.

Naloxone Market

Procurement rebalancing: Governments and health systems have moved from emergency procurement toward structured stockpiling and distribution strategies. Those shifts are creating predictable demand corridors, but also introducing new quality and supplier-diversity requirements that will affect supplier selection and contracting.

Competitive realignment: The market concentration landscape shows a mid‑to‑high level of incumbent strength, but entry and generic approvals have materially altered competitive dynamics. 2026 will reward firms that convert regulatory wins into sustainable commercial footprints.

Supply chain resilience: Intermittent shortages and episodic recalls over recent years have elevated supply-chain risk into a board-level concern. Firms that can demonstrate robust, diversified manufacturing and distribution capabilities will gain preferential access to institutional purchasers and public tenders.

Our report is designed for executives who need to translate macro trends into executable 12–24 month plans. The deliverables include:

Transparent market sizing and growth scenarios — base, upside and downside — with a clear articulation of drivers and sensitivities that matter for 2026 capital allocation.

Market-concentration and competitive positioning analysis that identifies where value accrues in the value chain and where disruptive entrants can capture share.

Commercial playbooks tailored to distinct routes-to-market (OTC retail, institutional procurement, community programs), including pricing benchmarks, payor engagement templates, and channel margin models.

Supply-chain risk matrices: source-of-supply mapping, single-point-of-failure identification, inventory hedging tactics, and contingency supplier short-listing.

Regulatory and reimbursement trackers that translate recent policy changes into actionable compliance and access strategies.

M&A and partnership screening: target profiles, valuation ranges, and integration checklists for inorganic growth or capacity expansion plays.

Practical implementation roadmaps and KPI dashboards for product launches, label changes, or government contracting campaigns.

The naloxone market is anchored by established pharmaceutical manufacturers and generics specialists. Key players analyzed in the report include those with OTC offerings, institutional supply capabilities, or scale in injectable and device technologies. Notable dynamics evaluated:

Market leaders that secured early OTC positioning have converted regulatory advantage into retail visibility; however, their margins are being compressed by generics and multipack pricing contests.

Generic manufacturers and legacy injectables suppliers continue to play a critical role in hospital and EMS channels, where institutional contracts and supply continuity are decisive procurement criteria.

Niche device innovators and auto‑injector suppliers present strategic partnership opportunities for incumbents seeking to diversify product portfolios and capture first-responder and consumer adoption trends.

Public-sector purchasing agencies and emergency stockpile programs remain influential buyers. Their procurement specifications increasingly include supplier performance clauses tied to manufacturing redundancy and delivery SLAs.

For decision-makers evaluating specific vendor engagement or M&A, the report includes scored vendor dossiers, a regulatory compliance map, and a shortlist of rapid-integration acquisition targets — all calibrated for 2026 execution timelines.

Product launches and regulatory approvals have accelerated market access: high‑visibility OTC twin-pack launches and FDA approvals of generics are shifting retail assortment and payer formulary design.

Large-scale public procurements continue to underpin baseline demand. National stockpile purchases and multi-year government contracts are smoothing seasonality and creating durable volumes for qualifying suppliers.

Macro-health indicators — including a persistently high number of opioid-related overdose fatalities — sustain political will for broad access, which in turn stabilizes public funding streams for distribution programs.

Operational disruptions — episodic drug shortages and isolated product recalls — have elevated quality and traceability as decisive procurement filters in institutional tenders.

For each corporate profile we outline priority moves grounded in market realities and executable within a 12‑month horizon:

Manufacturers with OTC capability: convert regulatory wins into shelf‑share by investing in point‑of‑sale visibility, co‑payments or coupon structures, and retail execution teams to accelerate consumer adoption.

Generic and injectable suppliers: secure multi‑year institutional supply contracts by demonstrating redundant production capacity, rapid fulfillment capabilities, and robust quality governance.

Payers and pharmacy chains: deploy formulary strategies that reconcile cost containment with community access; consider tiered reimbursement and clinician educational programs to optimize uptake without disrupting budgets.

Private equity and strategic acquirers: prioritize bolt-on targets that add manufacturing scale or device differentiation; insist on validated demand forecasts and operational readiness metrics as part of diligence.

Governments and NGOs: structure procurements to incentivize supplier diversification, local manufacturing partnerships, and data-sharing arrangements that improve distribution targeting and accountability.

Clients engage PW Consulting for a combination of market intelligence and implementation support. For organizations preparing 2026 plans we offer:

Rapid commercial due diligence and integration playbooks that reduce time-to-contract from months to weeks.

Procurement strategy workshops and tender templates aligned to contemporary buyer requirements and supplier scoring frameworks.

Supply-chain resilience diagnostics and supplier qualification programs to mitigate shortage risk and support regulatory compliance.

Custom forecasting and pricing models that stress-test assumptions across policy, demand, and unit-cost scenarios for board-level presentations.

Consistent with our “trailer” approach, this release intentionally omits the granular segmentation tables, regional and channel-level revenue breakdowns, and the detailed price decks that underpin our valuation and scenario outputs. These elements are core to near-term transaction decisions and are available exclusively to report subscribers and retained clients. The high‑level market size, CAGR and the strategic implications referenced above are sufficient to choreograph 2026 strategic planning conversations — but not to replace the proprietary tables and vendor scorecards required for contracting, bidding, or M&A execution.

For executive briefings, bespoke modeling, or access to the full Naloxone Market report and supporting annexes, contact PW Consulting’s life sciences practice. Our 2026-focused packages pair the report’s quantitative backbone with hands‑on implementation support — from procurement strategy to M&A diligence — so clients can convert market momentum into defensible, near-term results.

For detailed analysis of this topic, please visit the official page:Naloxone Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com