Alloy Compatibilizer Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As global polymer value chains navigate a period of accelerated technical change and regulatory pressure, compatibilizers for polymer alloys have moved from niche formulary tools to strategic enablers of product differentiation and circularity. PW Consulting’s latest Alloy Compatibilizer Market study — covering historical performance through 2025 and a forward-looking forecast for 2026–2032 — synthesizes market-scale dynamics, supplier positioning, raw-material exposure, and actionable go-to-market approaches that senior executives must internalize before committing capital or capacity in 2026.

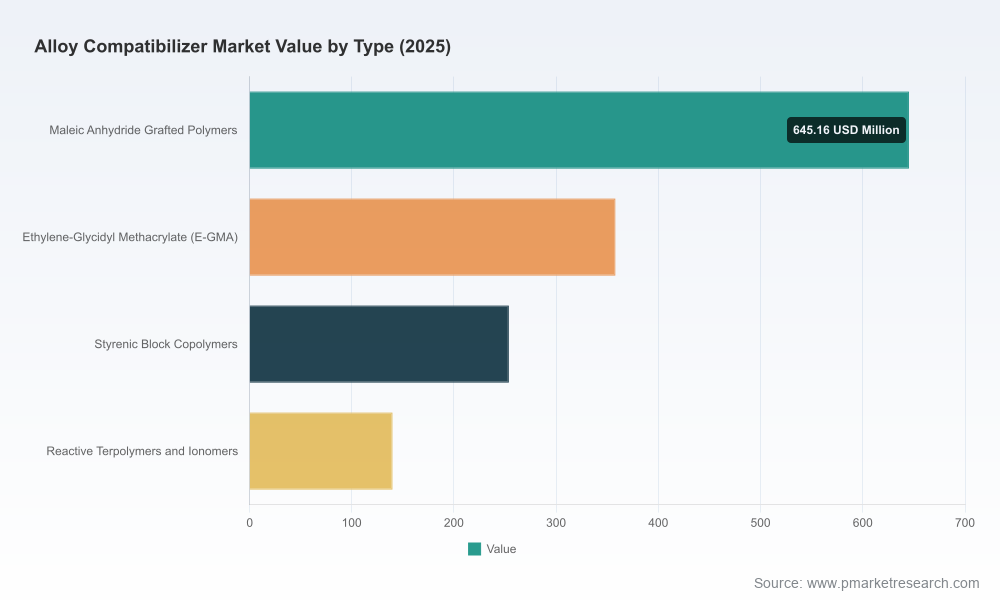

Alloy Compatibilizer Market

Headline market trajectory: clear growth, predictable variability

The compound market for alloy compatibilizers has expanded meaningfully over the past half decade. Our base-year analysis shows the market moving from just over USD 1.0 billion at the start of the decade to roughly USD 1.4 billion in 2025, with a near-term step-up projected for 2026. Over the forecast window 2026–2032 PW Consulting models a steady mid-single-digit growth path (6.5% CAGR), supporting a market worth more than USD 2.0 billion by the end of the period.

Alloy Compatibilizer Market

These macro signals are simple but powerful for boardroom decision-making: demand is real and sustained, but growth is concentrated in select value pools and application use-cases. Capital allocation therefore needs to be surgical — prioritizing technologies and routes-to-market that capture outsized share in the higher-growth pockets rather than broad-based scale bets.

Alloy Compatibilizer Market

Why 2026 is an inflection year for strategic choices

- Regulatory tightening creates product winners: New and tightening restrictions around legacy plasticizers and additives are accelerating adoption of alternative compatibilization strategies. Suppliers with validated, non-restricted chemistries can convert regulatory change into commercial advantage.

- Recycling is no longer optional: OEM and brand targets for recycled content mean compatibilizers that can stabilize heterogeneous polyolefin and engineered-plastic blends are moving from lab to production. Firms that can demonstrate performance at scale will unlock high-margin, long-term agreements.

- Raw-material price dynamics create margin opportunity and risk: Feedstock oversupply and softer contract pricing cycles in key intermediates have compressed variable costs in some regions, but volatility persists. Managing feedstock exposure (through integrated supply, long-term contracts, or flexible formulations) will determine winners.

- Geopolitical and trade headwinds: Tariff regimes and antidumping measures continue to reshape cross-border flows of additives and resins. Companies must weigh the economics of localization, tolling partnerships, and dual-sourcing to sustain customer service levels.

What the PW Consulting report contains — practical, decision-ready outputs

This study was designed for commercial and corporate strategy teams that must make 12–36 month investment decisions. Key deliverables include:

- Top-line market sizing and a dynamic demand model (2020–2032), enabling scenario analysis across material-substitution, regulatory, and circularity adoption curves.

- Technology & product roadmaps that benchmark compatibilizer chemistries by performance attributes (interfacial adhesion, thermal stability, processability) and cost-to-apply, including recommended application match-ups for automotive, electrical & electronics, packaging and construction use-cases.

- Practical supplier & customer playbooks: pricing frameworks, sample commercial terms, pilot-to-scale roll-out templates, and supplier qualification checklists tailored for compounders and OEMs.

- Supply-chain stress-testing: risk heat maps, localized vs. centralized manufacturing trade-offs, and hedging strategies for key feedstocks.

- M&A and partnership screening: a prioritized list of strategic targets and deal archetypes (bolt-on tech, regional footprint, recycling partnerships) supported by valuation sensitivities and integration risk factors.

- Regulatory compliance matrix and time-to-market makers — practical actions to align formulations with prevailing restrictions and certifications.

Competitive landscape — player strategies and strategic implications

The market is served by an internationally diverse set of suppliers: multinational chemical majors, regional polymer producers, specialist compatibilizer formulators, and additive masterbatch houses. While concentration is meaningful enough to influence pricing and commercialization norms, opportunities remain for differentiated players to claim premium positions.

- DuPont de Nemours, Inc. — Leverages proprietary acrylic copolymer platforms to serve thermoplastic elastomer and PVC-based alloy applications. Its strength is deep application know-how and long-standing OEM relationships in demand-critical sectors.

- Arkema S.A. — Focuses on grafted ethylene copolymer chemistries that facilitate polyolefin-to-engineering-plastic compatibilization. Arkema’s playbook emphasizes chemistry-led substitution and targeting complex alloy interfaces.

- BASF SE — Offers reactive polymeric extenders and compatibilizers and integrates them into broader polymer solution bundles. BASF’s advantage: scale R&D, global application labs, and cross-selling into existing resin customers.

- Avient Corporation — Differentiates through engineered, customer-specific compatibilizer compounds and expertise in high recycled-content blends. Avient is an attractive alliance partner for firms seeking rapid entry into circular formulations.

- SABIC; Mitsui Chemicals; SK Functional Polymer; LCY Chemical; Fine Organics; Clariant — These regional and specialty suppliers compete on a mix of local cost, tailored grades for recycling, and additive masterbatch integration. Their strategic edge lies in flexible manufacturing footprints and closer proximity to commodity customers.

Strategic implication: incumbents with proprietary chemistries and global distribution will defend premium OEM channels. However, agile regional players and compounders that can demonstrate recyclate-compatible performance and validated supply continuity will capture accelerating value pools.

Operational and commercial playbook for 2026

Based on our analysis, PW Consulting recommends a focused set of actions for corporate and commercial leaders preparing for 2026 decisions.

- Prioritize compatibility for recycled streams: Allocate R&D and pilot capacity to compatibilizers proven in mixed polyolefin and engineered-plastic blends. Secure anchor customers in high-volume verticals (automotive interiors, E&E housings) for early wins.

- De-risk feedstock exposure: Negotiate flexible supply agreements with key intermediates suppliers, explore short-cycle tolling arrangements, and maintain a portfolio of formulations that trade performance for raw-material neutrality under price stress.

- Embed regulatory-by-design: Fast-track reformulations that eliminate restricted plasticizers and align with major jurisdictional standards — this reduces conversion friction for multinational customers.

- Localize selectively: Use a hub-and-spoke manufacturing model in regions where tariff, antidumping, or logistics constraints fundamentally change landed economics.

- Pursue partnership models: Consider equity partnerships with compounders, recyclers, or regional resin producers to secure feedstock and application validation without heavy-capex commitments.

Scenario planning — what to model in 2026

Our forecast includes scenario variants that executives should model before finalizing budgets for 2026:

- Fast circularity adoption: High OEM recycled-content commitments accelerate demand for specialty compatibilizers; premium pricing and long-term supply contracts emerge.

- Commodity-price rebound: Rapid feedstock inflation compresses margins for low-differentiation grades, favoring specialty, reactive chemistries and supplier integration.

- Trade fragmentation: Escalation of trade barriers forces more regional production and local partnerships, increasing capex needs but preserving service levels.

Why PW Consulting’s full report matters for 2026

This preview surfaces strategic themes and the practical actions needed for 2026, but it intentionally omits the granular segmentation matrices, customer-level demand heat maps, and proprietary pricing models that underpin our client recommendations. The full report contains:

- Region- and application-level demand curves and elasticities calibrated to policy and substitution scenarios;

- Supplier-level commercial scorecards and comparative cost stacks;

- Investment cases with NPV sensitivities and integration checklists for M&A and JV opportunities.

For executive teams allocating R&D, manufacturing, or M&A capital next year, those granular modules are the difference between headline strategy and executable plans.

Closing — recommended next steps for 90-day execution

- Run a 90-day pilot program to validate one recycled-content compatibilizer in a target application with an OEM or tier-1 customer.

- Execute a supply audit for key intermediates and put at least one conditional long-term tie-up in place.

- Complete a regulatory-gap assessment for product portfolios against principal jurisdictional restrictions.

- Initiate partnership outreach to local compounders or recyclers in priority markets to test co-development models.

PW Consulting’s Alloy Compatibilizer Market report is built to inform exactly these decisions. If your 2026 strategic plans hinge on securing share in the next phase of polymer alloy evolution, the full study provides the actionable datasets, supplier benchmarking, and decision tools required to move from intent to execution. To access the complete intelligence, including proprietary segmentation and modeling outputs that were intentionally withheld from this preview, visit PW Consulting’s Alloy Compatibilizer Market report page or contact our industry advisory desk.

For detailed analysis of this topic, please visit the official page:Alloy Compatibilizer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com