Paper Plate Market — Strategic Preview for 2026: How the Next Wave of Regulation, Cost Pressure, and Sustainability Will Redraw Competitive Advantage

PW Consulting’s latest market study on the global Paper Plate Market (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes commercial, regulatory and operational signals that will determine winners and losers across 2026 corporate cycles. The market reached approximately USD 5,676 million in 2025 and the base-case forecast shows a steady expansion at a 4.2% CAGR over the 2026–2032 horizon, underpinning a multi-year runway for investment — but one shaped by uneven regional demand, raw-material dynamics, and accelerating producer responsibility obligations.

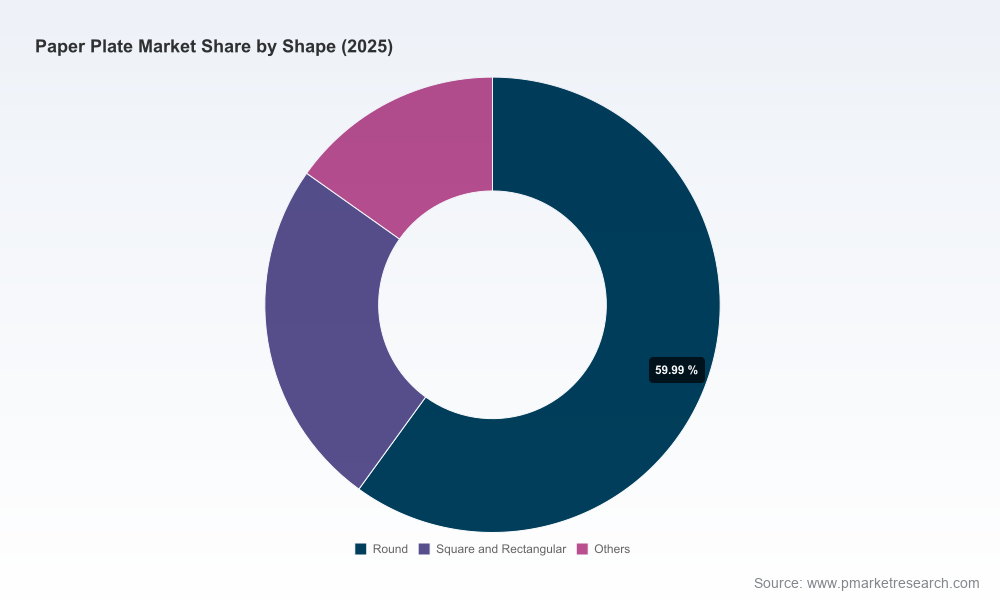

Paper Plate Market

Why this briefing matters for 2026 decision-makers

- Capital allocation: the market size and growth profile validate selective capacity investment, but not indiscriminate expansion. Our analysis highlights where marginal returns will be compressed by input-cost inflation and where premiumization (strength, compostability) can preserve margin.

- Strategic sourcing: rising pulp and paper input-price volatility means procurement strategies executed in 2026 will lock-in cost competitiveness through 2028. Our report provides stress-tested scenarios for supplier contracts and hedging.

- Regulatory risk management: new Extended Producer Responsibility (EPR) rules and trade remedies are no longer future threats — they are live variables in 2026 planning. Companies that model EPR cash flows and compliance pathways now will gain a first-mover advantage.

- M&A and portfolio moves: with market concentration remaining low (three-firm and five-firm concentration metrics indicate a fragmented landscape), consolidation and capability buys remain compelling — but the right targets are those that solve capability gaps (sustainable coatings, compostable raw materials, or localised footprint) rather than just scale.

What’s in the full PW Consulting report (practical, actionable content)

- Executive dashboards: top-line market trajectory, scenario bands for demand and cost, and an investor-ready executive summary tailored for board-level decision-making.

- Supply-chain and input-cost models: transparent, auditable models that map pulp/paperboard price movements to unit cost, with sensitivity analysis using recent Producer Price Index baselines.

- Regulatory playbooks: state-level and national EPR impact matrices, compliance cost templates, and options for producer consortia vs. solo compliance strategies.

- Commercial playbooks: product premiumization paths (strength, coatings, compostability), channel-to-product mapping, and go-to-market templates for retail, foodservice, and institutional channels.

- CapEx and ROI tools: build-versus-buy worksheets, brownfield upgrade checklists for coating and compostable lines, and a calendar of permitting and lead-times by region.

- Competitive due diligence packs: target scoring frameworks, integration risk checklists, and synergy assumptions framed for M&A diligence.

- Procurement negotiation modules: RFP templates, scorecards for fibre suppliers and coatings vendors, and contracting clauses for EPR pass-throughs.

Market dynamics: demand drivers and structural headwinds

The paper plate market shows resilience and structural growth, but beneath the headline CAGR lies a set of forces that will reshape margin pools and competitive positioning.

Paper Plate Market

- Input-cost trajectory. Paper plates are predominantly manufactured from paperboard or paper pulp with functional barrier coatings for grease and liquid resistance. Recent PPI baselines for pulp/paper categories indicate indices in the roughly 250–354 range, signaling ongoing input cost dynamics that will drive price and margin volatility in 2026.

- Regulatory acceleration. Multiple U.S. states have enacted EPR laws for packaging and paper products, requiring producers to fund collection and recycling/processing. India’s amendments to Plastic Waste Management Rules extend stricter EPR obligations to paper-based items effective April 1, 2026. Separately, trade remedy decisions have introduced duties on certain imported plates — an immediate supply-chain and sourcing consideration.

- Channel and consumer shifts. Foodservice demand is reconfiguring toward away-from-home convenience and premium single-use formats that balance convenience with sustainability claims. Residential consumption remains sizeable but is sensitive to disposable income and retail promotional cycles.

- Coatings and circularity. Advances in fiber technology and compostable barrier chemistries create premium product tiers, but verification, end-of-life logistics, and claims substantiation are increasingly decisive. Investment in certified compostability or recyclable coated paper can be a differentiator — if accompanied by credible collection and processing partnerships.

Competitive landscape: who matters and why

The market remains fragmented, with the top few firms holding a relatively small share of global value — an environment that favors both specialist innovators and regional champions. Key companies shaping the competitive frontier include:

Paper Plate Market

- Huhtamaki Oyj (Espoo, Finland) — a global leader in fiber-based disposables with deep expertise in recyclable and compostable coatings. Their R&D focus on fiber technology and scalable compostable options positions them at the intersection of sustainability innovation and broad-scale foodservice supply.

- Dart Container Corporation (Mason, Michigan, USA) — a major North American supplier with strong brand recognition in durable, heavyweight paper plates. Product innovations targeting strength and usability in commercial foodservice are core to their value proposition.

- Georgia-Pacific LLC (Dixie) — a significant player in both retail and away-from-home channels; recent investments in dedicated manufacturing capacity underscore a capacity-centric strategy to protect supply continuity for branded tableware.

- Pactiv Evergreen Inc. — supplies a diversified portfolio of paper and plastic disposables with deep penetration in institutional and commercial channels. Their integrated packaging offerings and customer relationships make them a key competitor on multi-product procurements.

- Specialists and regional champions — companies such as Genpak, International Paper, Duni AB, and several U.S. domestic producers provide localized production capability, flexible SKUs, and cost advantages in their home markets.

- Eco-focused entrants — Eco-Products, Vegware and similar plant-based specialists drive innovation in compostable claims and premium positioning, often serving foodservice customers with aggressive circularity targets.

Recent corporate moves crystallize strategic intent: Georgia-Pacific opened a new tableware-dedicated facility in late 2024; Dart launched a heavyweight “Bold Hold” paper plate line in mid-2025; and Duni Group’s acquisition activity in 2024 highlights consolidation strategies to expand product breadth in Europe. These developments demonstrate three concurrent strategic responses: capacity reinforcement, product premiumization, and targeted M&A.

Actionable strategic implications for 2026

For boards, corporate strategy teams, and procurement and operations leaders, the following imperatives should shape 2026 planning cycles.

- Model EPR now. Treat producer responsibility costs as a quasi-fixed structural expense and run at least three compliance scenarios (low, medium, high) into pricing and margin models. Consider collective compliance consortia where practical to limit administrative burden.

- Prioritise near-shore and flexible capacity. Recent trade remedies and port volatility make geographic diversification and localised manufacturing valuable. Where capex is constrained, contracting flexible toll-manufacturing or strategic tolling agreements can preserve agility.

- Differentiate on verified sustainability — not just claims. Invest in third-party certifications, end-to-end compostability pilots with waste processors, and transparent lifecycle communication. Premiumization will command higher price points only if downstream infrastructure supports end-of-life claims.

- Lock procurement levers in 2026 to secure 2027–2028 cost competitiveness. That includes multi-year fibre agreements with indexation, vertical integration options for critical pulp inputs, and supplier scorecards that embed EPR and ESG performance.

- Be selective on M&A. Targets that close capability gaps (barrier technology, regional production, verified compostable portfolios) deliver higher strategic ROI than those offering incremental scale alone in a fragmented market.

Next steps: how to use this preview

This article highlights the strategic contours that will determine performance in 2026 and beyond. For teams preparing budgets, procurement calendars, M&A pipelines, or sustainability roadmaps, PW Consulting’s full Paper Plate Market report contains the operational tools, models, and regulatory matrices that turn insight into executable decisions.

To access the complete set of models, scenario decks, supplier scorecards, and regulatory playbooks that accompany this briefing, visit the PW Consulting report page or contact your PW Consulting analyst. The full report is deliberately gated to preserve competitive integrity — consider this piece the trailer that confirms the forecast runway and exposes the decision levers you must act upon in 2026.

PW Consulting — enabling pragmatic strategy where market structure, regulation, and operational execution intersect.

For detailed analysis of this topic, please visit the official page:Paper Plate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com