PW Consulting: Anti‑Drone Systems Market to Skyrocket from USD 2,680 Million (Base Year 2025) to USD 13,775 Million by 2032 — Forecast CAGR 26.35% (2026–2032)

Other |

2026-07-02 13:12:34

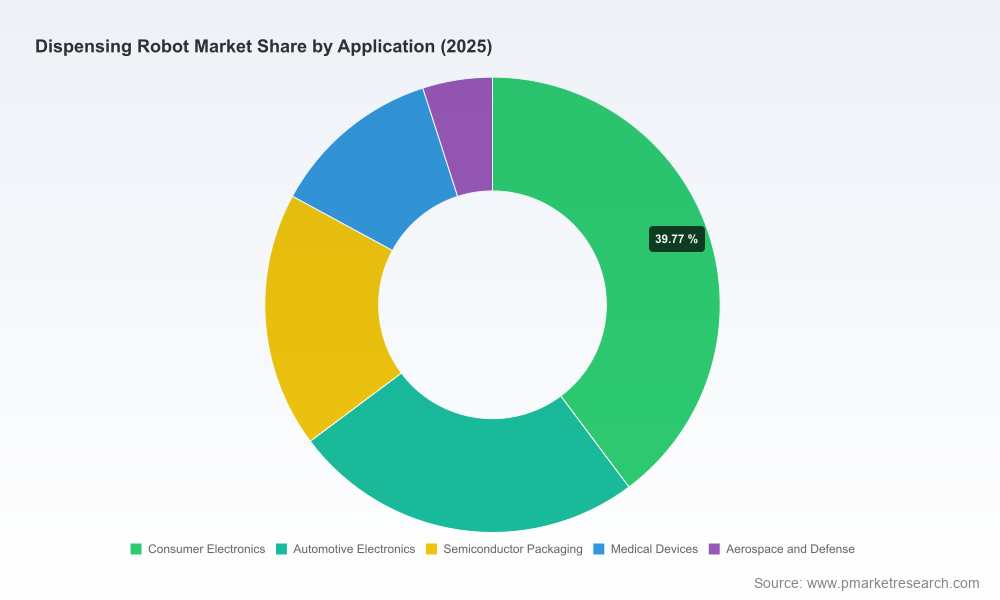

As healthcare systems and high‑precision manufacturing environments confront persistent labor shortages, margin pressure, and rising complexity in distribution workflows, dispensing robotics has moved from a niche automation play to a strategic infrastructure decision for 2026. Our new PW Consulting Dispensing Robot Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides the practical intelligence leaders need to convert market momentum into defensible advantage. The global market expanded from just over USD 1.35 billion in 2020 to roughly USD 2.07 billion in 2025 and is forecast to accelerate further — reaching approximately USD 2.34 billion in 2026 and climbing toward an estimated USD 3.85 billion by 2032, representing a compound annual growth rate of 9.24% through the forecast window.

Dispensing Robot Market

Capital discipline is reshaping project pipelines. In recent health‑system surveys, a plurality of providers signaled plans to pare capital spending in 2026 even as certain pharmacy expenditures continue to expand. The result: organizations will selectively fund automation that demonstrably reduces operating cost or unlocks new revenue‑generating services.

Dispensing Robot Market

Pharmacy and specialty medication flows are growing. Broad pharmacy spending trends point to continued expansion driven by infusion, specialty therapies, and centralized fill models — creating pockets of high demand for automated dispensing throughput and accuracy improvements.

Dispensing Robot Market

Automation is a prioritized mitigation for workforce pressure. A meaningful share of health‑system leaders now list automation investments as a core response to staffing shortages and burnout, elevating the strategic importance of dispensing robots beyond pure capital projects to mission‑critical operational tools.

Our research is designed for practitioners who must turn insight into action. The report blends market intelligence with hands‑on deliverables that operational teams, procurement leaders, and corporate strategists can use immediately:

Market sizing and consensus forecasts by year (historical 2020–2025; base 2025; forecast 2026–2032) and scenario variants that stress hospital capex contraction, accelerated pharmacy volume, and rapid central‑fill adoption.

Decisioning frameworks: vendor selection scorecards, buyer persona profiles, procurement timing playbooks, and total cost‑of‑ownership (TCO) templates calibrated to different adopter types (hospital central pharmacy, retail, long‑term care, and specialized manufacturing environments).

Deployment blueprints: phased implementation roadmaps, integration checklists for EMR/pharmacy management systems, KPI templates for throughput, accuracy, and labor displacement, and test plans for go‑live acceptance.

Commercial guidance: payback models, financing and leasing comparators, aftermarket service and spare‑parts economics, and contracting language examples to secure uptime guarantees and performance‑based pricing.

M&A and partnership playbooks: target screening criteria, valuation sensitivities for software vs hardware businesses, and integration risk matrices for prospective rollups or strategic alliances.

Vendor intelligence: structured profiles and comparative analysis of incumbent suppliers, product archetypes, technology differentiators, and go‑to‑market footprints suitable for shortlisting and competitive benchmarking.

The dispensing robot market remains commercially attractive and moderately fragmented. The top three and top five vendor groups account for modest but meaningful shares of market revenue, leaving room for specialized entrants and regional champions to scale. Below we summarize strategic positioning and implications for buyers and sellers.

Omnicell, Inc. — With a portfolio spanning central pharmacy dispensers, IV compounding stations, and medication‑management software, Omnicell continues to emphasize end‑to‑end workflow integration for health systems. Its strength is in platform anchoring: tying robotics hardware to medication safety and analytics suites that justify total‑system purchases.

Becton, Dickinson and Company (BD) — BD combines cabinet‑level automation (Pyxis) with high‑speed dispensing systems and recently showcased advanced boxed‑medication automation for the U.S. market. BD’s strategy amplifies central‑fill plays with an emphasis on replenishment automation and throughput for boxed inventory.

Capsa Healthcare — Capsa focuses on compact dispensing solutions optimized for retail pharmacies and outpatient environments. Their competitive angle is low‑footprint automation that accelerates adoption where floor space and incremental capex are constraints.

Swisslog Healthcare (KUKA Group) — Swisslog leverages systems integration heritage, offering storage, retrieval, and packaging automation as part of broader logistics modernization programs within hospitals and health systems. They compete on large‑scale automation and integration services.

ScriptPro LLC — ScriptPro remains a recognized name in robotic prescription dispensing for retail and government pharmacies, selling compact to mid‑scale systems and differentiated by rapid deployment models and compliance‑focused features.

Yuyama Co., Ltd. — A long‑standing supplier of automated packaging and vial filling systems, Yuyama is often chosen for compliance packaging and high‑volume outpatient pharmacy workflows.

Parata Systems (BD Parata) — Parata’s strengths are in high‑speed vial fillers and pouch packaging for central fill operations, and its recent integration with global suppliers shifts the competitive dynamic where scale and speed matter.

ARxIUM — Specializing in carousels, vial fillers, and high‑throughput fulfillment systems, ARxIUM targets hospital networks and outsource pharmacy operators seeking scale and repeatable central‑fill operations.

Baxter International — Baxter’s focus on therapy compliance and patient‑specific dispensing positions it at the intersection of clinical therapy management and automation, particularly within hospital pharmacy programs seeking clinical outcomes integration.

McKesson Corporation — As a distribution and services giant, McKesson bundles automation within broader supply chain services and can accelerate adoption through channel reach and managed service offerings.

Product launches and demonstrations continue to reshape buyer expectations. A notable example in late 2025 was the U.S. introduction of a high‑speed boxed‑medication dispensing system featuring automated replenishment features—an event that signals stronger competition around throughput, replenishment automation, and integration ease. Expect vendors to increasingly compete on software‑enabled replenishment, analytics, and outcomes guarantees rather than hardware specs alone.

Adoption levers — Workforce shortages, pharmacy spending growth in specialty care, and the push toward centralized fills and outpatient consolidation make a compelling case for automation that delivers measurable labor savings and accuracy improvements.

Commercial risks — Tight capital budgets for many health systems mean vendors must articulate near‑term ROI, offer flexible financing, and structure performance‑based contracting to move procurement committees.

Implementation risks — Integration with pharmacy information systems, change management at the point of dispensing, and service reliability are frequent sources of deployment slippage. Early wins often depend on clear KPI definitions and pilot programs that limit scope while proving unit economics.

Regulatory & security considerations — As dispensing robotics integrate with patient records and medication management systems, cybersecurity and compliance become material factors in vendor selection and contracting.

Whether you are a hospital network, pharmacy operator, vendor, or investor, the following actions are the highest‑impact moves to consider this year:

For buyers: Prioritize pilots that align with defined labor reduction targets and revenue‑adjacent services (e.g., specialty central fill). Use a phased procurement approach with clear milestones tied to payment or expansion triggers.

For vendors: Differentiate through software and services. Hardware parity is narrowing; profitable growth will come from subscription services, guaranteed uptime, replenishment automation, and data monetization.

For investors and private equity: Seek tuck‑ins that add software, field services, or regional distribution capability. Valuation premia will attach to businesses with recurring service revenue and proven integration references.

For integrators and channel partners: Build outcome‑based offerings that combine financing, implementation, and managed services to de‑risk buyer decisions and capture a larger share of lifecycle revenue.

Base case — steady growth (our midpoint forecast): adoption follows current trends in pharmacy volume and automation prioritization; TCO and outcomes data drive mainstream procurement.

Constrained capex case — slower near‑term deployments: if capital cuts intensify, adoption pivots toward leasing, managed service models, and retrofit solutions that minimize upfront spend.

Acceleration case — staffing crisis and regulatory drivers force rapid automation: widespread rollouts of central‑fill robotics and high‑speed vial systems reorder vendor rankings in favor of scale players and integrated software providers.

Executives should treat the report as both an intelligence asset and a project toolkit. Use the forecast scenarios to stress‑test capital plans, the vendor scorecards to shortlist suppliers for RFPs, and the TCO models to build CFO‑grade business cases. For commercial teams and investors, apply our M&A playbook to identify consolidation targets and model integration value.

This briefing intentionally highlights the strategic insights you need to act while withholding the granular segment breakdowns and company revenue shares that we reserve for the full PW Consulting report and interactive datasets. Those detailed tables (regional and application splits, vendor market shares, and downloadable financial models) are available through our report portal and are included in advisory engagements.

To obtain the full dataset, vendor scorecards, and executable playbooks that complement this strategic briefing, visit the PW Consulting Dispensing Robot Market report page or contact our advisory team to schedule a tailored briefing and scenario workshop.

For detailed analysis of this topic, please visit the official page:Dispensing Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com