Industrial Demand Driving Rugged Devices Market Expansion Through 2034

Other |

2026-05-22 12:19:18

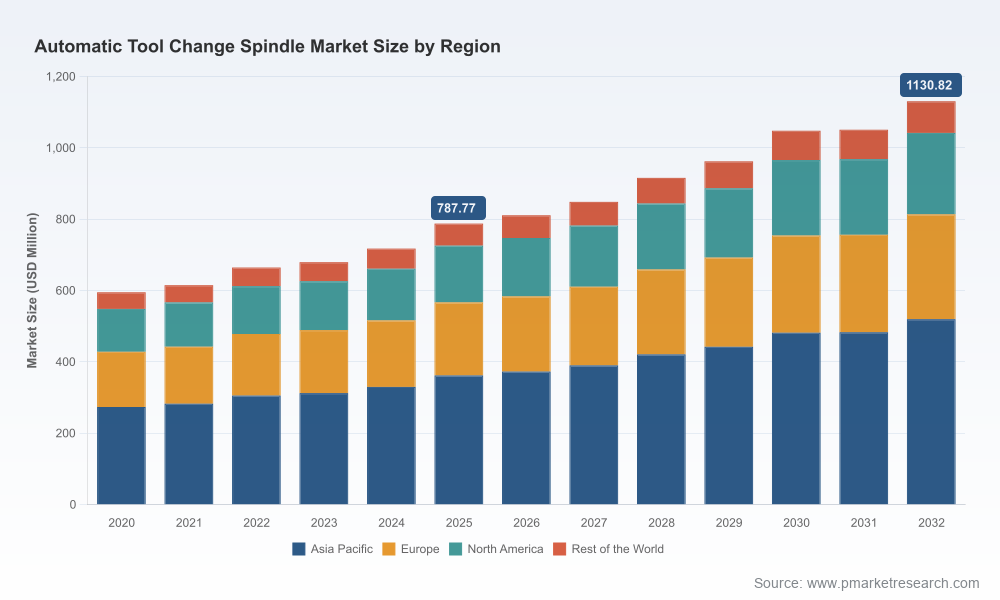

PW Consulting today publishes a forward-looking executive briefing drawn from our full market research report on the Automatic Tool Change (ATC) Spindle market. The study consolidates five years of historical insight (2020–2025) and a seven-year forecast (2026–2032), delivering the market context leaders need to make pragmatic, risk-balanced decisions in 2026 and beyond. In macro terms, the global ATC spindle market grew from USD 595.4 Million in 2020 to USD 787.77 Million in 2025 and is projected to expand at a 5.31% CAGR through 2032, reaching approximately USD 1,130.82 Million by the end of the forecast horizon. This briefing highlights the strategic value of that analysis for procurement, product, M&A and operations leaders while preserving the deeper segment-by-segment datasets in the full report.

Automatic Tool Change Spindle Market

Acceleration of automation investment: Post-pandemic capital allocation is shifting from pure volume expansion to productivity and resilience. ATC spindles—by enabling reduced tool-change downtime and supporting lights-out machining—are a focal point for CAPEX prioritization.

Automatic Tool Change Spindle Market

Technology bifurcation: High-speed air-bearing and motorized electrospindles have moved beyond niche applications, while robust, lower-cost solutions for routing and general engineering underpin wider adoption. This creates both premium and volume plays within the same category.

Automatic Tool Change Spindle Market

Supply-side shock absorption becomes strategic: Rising raw-material and component cost inflation—especially in precision bearings—has already increased manufacturing cost burdens, shifting the economics of in-house production versus outsourcing and the calculus for vertical integration.

Market sizing and trajectory: A validated top-line model with historical reconstruction (2020–2025) and scenario-based forecasts (2026–2032), available in interactive formats for sensitivity testing of price, volume, and supply constraints.

Go-to-market playbooks: Channel and OEM strategies, distributor segmentation, retrofit opportunity maps, and pricing levers for both premium and value tiers.

Technology and product roadmap analysis: Comparative assessment of air-bearing, motorized, belt-driven and gear-driven approaches, lifecycle risk matrices, and recommended R&D focus areas for speed, thermal control, and tool-change reliability.

Procurement & supplier risk toolkit: Due-diligence checklists, supplier scorecards, hedging strategies for bearing and rare component exposure, and supplier consolidation scenarios to secure continuity without eroding competitiveness.

Competitive benchmarking and vendor dossiers: Independent profiles and strategic implications for leading suppliers, with supplier strengths/weaknesses, distribution footprints and likely strategic moves.

M&A and partnership intelligence: Identification of tuck-in target archetypes, valuation comparators, and integration playbooks calibrated to manufacturing and service roadmaps.

Operational playbooks: Retrofit economics, aftermarket service monetization strategies, and labour substitution models for lights-out machining adoption.

Demand Side — productivity and specialization: Manufacturers invest in ATC spindles to compress cycle times, increase machine utilization and enable flexible production of complex, high-mix parts—particularly in sectors demanding high spindle speeds and micron-level tolerances.

Labour displacement and skills shortage: Skilled CNC labour shortages are cited industry-wide as a prime driver of automation uptake. ATC spindles are frequently a near-term, high-impact automation insert that enables reduced operator intervention.

Supply Side — component concentration and cost pressure: The bearings ecosystem and high-precision components are under stress from raw-material inflation and capacity tightness. These cost pressures have materially increased production costs for smaller manufacturers, forcing re-pricing, heavier reliance on outsourced subassembly, and renewed interest in long-term supplier agreements.

Regulatory and sustainability tailwinds: Energy-efficiency targets and lifecycle considerations are nudging buyers toward spindles with lower energy draw and longer service intervals—favouring designs that marry thermal stability with simplified maintenance.

The ATC spindle vendor ecosystem is a mixture of highly specialized European and US engineering houses, regional scale Chinese manufacturers, and agile US retrofit and hobbyist-oriented suppliers. The full report contains independent dossiers on each major player; below we summarize strategic positioning and near-term implications for 2026 planning.

GMN USA (subsidiary of GMN Germany) — Premium high-speed engineering: GMN’s high-speed, lubricated bearing spindles and documented guidance on selection/maintenance position it as the trusted partner for precision machining OEMs. Expect continued emphasis on application engineering services and educational content to shorten sales cycles for high-ticket systems.

Celera Motion (Novanta) — Ultra-high-speed, niche aerospace/composites play: Celera’s air-bearing offerings target thin-wall composites and non-ferrous high-speed milling. Their technology is a clear play for aerospace and specialized electronics finishing where speed-to-precision is non-negotiable.

Teknomotor — Vertical fit for woodworking and aluminum extrusion markets: Italy-based Teknomotor’s electrospindle designs and quick-change ergonomics are tailored to wood and light-alloy industries—an attractive partner for OEMs in high-throughput panel and profile machining.

Jingjiangcity Jianken — Cost-competitive scale: As a long-time supplier of pneumatic ATC spindle motors, this Chinese manufacturer represents a sourcing node for price-sensitive OEMs and retrofit houses, with strong potential to scale globally through partnerships or distribution agreements.

CNC Depot, Air Turbine Tools, PwnCNC, RapidChange ATC — Retrofit and accessibility segment: These US players are important for off-the-shelf and aftermarket adoption—lower transaction friction, reduced lead times and a focus on retrofitting ageing fleets are key strategic levers here.

SPINOGY — Modular, high power-density solutions: European modular spindles that support fully automatic tool changes and robotic cell integration are positioned to capture demand in advanced CNC milling and cobot-assisted cells.

Strategically, manufacturers and investors should treat the vendor landscape as an ecosystem with distinct roles: high-end engineering partners for precision-critical applications, regional low-cost producers for volume, and retrofit/aftermarket suppliers to capture legacy machine estates. There is room for modular partnerships and buy/build models that combine engineering IP with scale manufacturing.

Product guidance and content-led demand generation: GMN USA’s January 2026 guidance update highlights how authoritative, application-specific content reduces adoption friction for high-performance spindles.

Integration-focused releases: Information releases from ecosystem players (December 2025 onwards) demonstrate growing attention to integration—spindle + ATC + controller—rather than point-product sales.

Raw material pressure: The precision bearing market (a critical upstream input) is sizable and continues to see year-on-year price pressure and capacity dynamics that favor buyers with committed sourcing and forecasting capability.

Re-prioritize procurement for continuity: Move from transactional purchase orders to multi-year supply agreements for bearings and critical subcomponents; include indexation and service-level clauses to protect margin and uptime.

Differentiate via solution-selling: OEMs should bundle spindles with ATC systems, service contracts and predictive maintenance to capture higher lifetime revenue and lock-in customers.

Invest in retrofit channels: A near-term revenue and rapid-deployment opportunity exists in retrofit kits for ageing fleets—this is low-capex, quick-return work that also establishes installed-base relationships.

Adopt a tiered product strategy: Maintain a premium, engineering-led product line for precision segments while scaling a value platform for volume markets, with clear SKU rationalization to manage cost-to-serve.

Prepare for M&A and strategic alliances: Identify small-to-medium engineered-spindle specialists or retrofit hardware vendors as tuck-in targets to accelerate route-to-market and aftermarket service capability.

Scenario-test capital investments: Use the interactive forecast scenarios in the full report to stress-test CapEx plans against variations in component inflation, adoption curves and geographic demand shifts.

PW Consulting’s full report is structured to be immediately operational: executive dashboards that feed commercial planning, downloadable vendor scorecards for procurement, a supplier risk heat map for supply-chain meetings, and scenario models for CFO-level sensitivity analysis. We intentionally present high-level macros and strategic playbooks in this briefing to outline the decision-use cases; the complete report contains the granular segment matrices, regional breakdowns, unit economics and vendor scorecards required to execute strategy with precision.

For procurement, engineering, commercial strategy or private-equity teams evaluating entry and expansion opportunities in the ATC spindle space, this research provides the evidence base to prioritize investments in 2026 and to architect resilient, margin-accretive portfolios.

To access the comprehensive datasets, granular segment analyses and executable templates referenced above, please visit the PW Consulting report page for the Automatic Tool Change Spindle Market. The full study contains the protected segment tables, vendor scorecards and downloadable models that operational teams use to convert insight into action.

For detailed analysis of this topic, please visit the official page:Automatic Tool Change Spindle Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com