Rhinoplasty Surgery in Dubai for Long-Term Results

Health |

2026-07-07 11:17:19

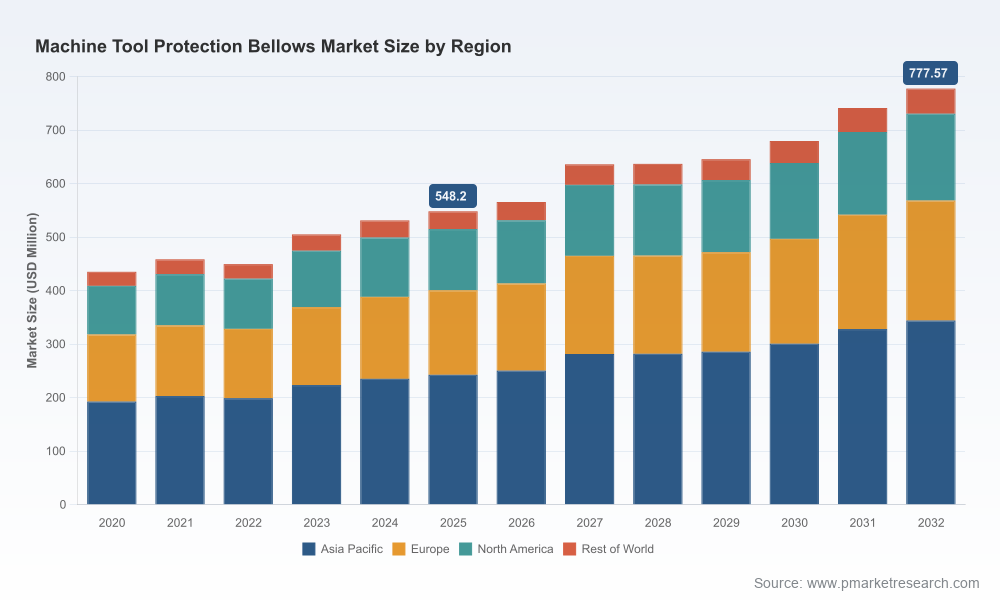

PW Consulting today publishes a focused industry briefing accompanying our full Machine Tool Protection Bellows Market report—designed to inform executive decisions in 2026. The global market for protection bellows, measured at a mid‑year base in 2025, has demonstrated steady recovery and expansion since 2020 and is projected to grow at a compound annual growth rate (CAGR) of approximately 5.12% through our 2026–2032 forecast horizon. By revealing the macro trajectory, regulatory headwinds, raw‑material sensitivities, and supplier dynamics, this briefing highlights the levers that matter for procurement, product strategy, and corporate development—while reserving the granular segment tables and regional/application splits for readers of the full report.

Machine Tool Protection Bellows Market

Procurement resilience: Rising input costs and trade measures are already compressing supplier margins. The report equips sourcing teams with a prioritized set of hedging and qualification actions that minimize disruption and protect gross margins.

Machine Tool Protection Bellows Market

Product and technology roadmaps: As machine builders accelerate automation and high‑speed machining, component requirements are shifting rapidly. The analysis identifies the technical attributes—materials, form factors, cleanroom compatibility—that will command premium positioning.

Machine Tool Protection Bellows Market

M&A and partnerships: Consolidation potential exists but is selective. The briefing highlights the commercial and technology traits that make targets attractive, along with a practical valuation framework consistent with industry growth expectations.

Regulatory compliance and market access: Updated regulatory and tariff developments are changing supply‑chain economics. The report translates those changes into actionable decisions for market entry and cost pass‑through strategies.

The machine tool protection bellows market has moved from cyclical contraction in the early 2020s into a more durable expansion phase by 2023–2025, driven primarily by increased investments in factory automation. Industry sources indicate global machine‑tool investment growth accelerated in 2025, supporting higher replacement and retrofit activity for protective components. PW Consulting’s consolidated model shows steady growth from the 2025 base through 2032 under the central scenario (CAGR ≈ 5.12%).

Two structural trends are most consequential for 2026 planning. First, raw‑material cost volatility is elevating input risk: steel plate prices and specialty resin costs increased materially through 2024–2025, creating immediate margin pressure for heavy‑duty and coated fabric bellows. Second, regulation and trade policy are reconfiguring cost baselines—European measures on steel and carbon embedded in imports come into effect in 2026, changing the landed cost calculus for manufacturers and importers. Combined with ongoing automation-led demand, these dynamics make near‑term supplier selection and price‑risk mitigation critical.

The market breaks down along three practical axes—geography, product type, and application—and each axis matters for a different type of decision. Rather than reproducing the proprietary split tables here, we summarize directional insights that buyers and strategists can act on:

Product types: Traditional folded and circular bellows remain core to most replacement cycles, while stitched and composite constructions are gaining traction where durability, chemical resistance, or thermal performance are prioritized.

Applications: CNC machining and high‑precision centers drive steady base demand; grinding and specialty cutting applications spur demand for heavy‑duty or coated solutions. Cleanroom and high‑speed machining niches are the fastest evolving pockets, commanding differentiated design criteria.

Geography: Regional manufacturing footprints and trade measures alter sourcing logic. Firms with flexible regional manufacturing or robust distributor networks have a competitive advantage in passing through cost changes and maintaining lead times.

For teams preparing capital allocation or sourcing plans in 2026, the full report provides the precise segment-level volumes and growth rates tied to these qualitative trends—data intentionally omitted here to preserve the report’s value as the definitive source.

The supplier base is a mix of specialized fabricators, composite innovators, and precision metal shops. Market concentration is moderate: the top three and top five suppliers command meaningful but not overwhelming shares, leaving room for regional specialists and technology-focused entrants to compete. That balance shapes both pricing power and acquisition opportunity.

Dynatect Manufacturing, Inc. – Known for customizable systems and a broad portfolio that includes steel mill‑type and silicone‑coated solutions. Recent product introductions emphasize low‑profile designs aimed at high‑speed machining, reinforcing Dynatect’s strength with OEMs that prioritize compact, low‑inertia protection solutions.

A&A Manufacturing Co., Inc. – A longstanding producer of accordion‑style bellows in fabric, rubber, and plastic. Their legacy in straightforward, cost‑effective covers positions them well for distribution channels and aftermarket replacement business.

Gortec Bellows B.V. – A European specialist combining polyurethane and steel for high‑speed applications. Trade‑show activity demonstrates a deliberate move into cleanroom and precision markets—an area to watch for partnerships with machine tool builders.

Tecnovel S.r.l. – Italian engineering focus with options for cleanroom compatibility and spindle protection. Their niche positioning maps to medical and semiconductor equipment manufacturing trends.

Advanced Composites, Inc. (ACI) – Innovator in composite bellows; their materials expertise targets high‑temperature and chemical resistance applications, important where traditional fabrics and steels reach performance limits.

Hohmann Platten GmbH and Fa. Willich Präzisionswerkzeuge GmbH – European heavy‑duty and precision providers respectively, with deep experience in steel plate bellows and telescopic covers for large machine tools. These vendors are particularly relevant to firms in heavy industries and precision tooling sectors.

Recent trade‑show activity—such as Dynatect’s expanded low‑profile line at IMTS and Gortec’s polyurethane solutions at EMO—illustrates suppliers doubling down on product differentiation rather than competing purely on price. For procurement and product teams, that implies a two‑track strategy: lock in reliable supply of commodity covers while building partnerships for differentiated designs that command higher margins.

Across procurement, engineering, and commercial functions, PW Consulting recommends a compact set of measures actionable within 90–180 days:

Price and input risk: Implement raw‑material indexation clauses and multi‑sourcing for critical resins and steels; where feasible, negotiate longer forward contracts to smooth spikes tied to trade measures.

Design for standardization: Reduce SKU proliferation by identifying modular design families that meet 70–80% of customer needs—freeing R&D spend for targeted high‑value variants.

Supplier scorecards: Expand qualification criteria beyond cost—include lead time stability, compliance with ISO 14120 (machine guarding requirements), and proven cleanroom manufacturing where relevant.

Commercial tactics: For OEM channels, favor collaborative development agreements with cost‑sharing on tooling for differentiated bellows; for aftermarket, build distributor incentives and local inventory buffers to shorten replacement cycles.

Given the market’s mid‑single‑digit CAGR and rising input costs, acquisition opportunities are most attractive where buyers can immediately capture synergies or proprietary product advantages. PW Consulting’s M&A framework prioritizes targets that provide:

Access to differentiated materials or patented sealing systems;

Channel breadth in underpenetrated regional aftermarket markets;

Manufacturing scale that offsets rising raw‑material and compliance costs;

Strong engineering partnerships with OEMs in high‑growth niches, such as cleanroom and high‑speed machining.

We counsel disciplined valuation approaches that stress tested cash flow against rising steel and resin price scenarios and potential tariff exposures—details and model scenarios are included in the full report.

Proprietary market model with historical series (2020–2025) and scenario forecasts (2026–2032).

Price‑sensitivity and raw‑material stress tests that quantify margin impacts under realistic steel and resin trajectories.

Supplier benchmarking covering commercial exposure, technology strengths, and recent product activity.

Go‑to‑market playbooks for OEM, aftermarket, and distributor channels.

M&A shortlist and an interactive dashboard for slicing the market by region, type, and application (note: detailed segment tables are accessible in the report portal).

For executives allocating capital, negotiating long‑term supply agreements, or retooling product roadmaps in 2026, the key is to act on a dual agenda: secure resilient access to commodity inputs while investing selectively in differentiated technologies and partnerships that capture premium growth pockets. The market’s steady mid‑single‑digit growth provides a stable backdrop—but rising input costs, new trade measures, and faster‑evolving application requirements mean that tactical execution will determine winners over the next 18–36 months.

PW Consulting’s full Machine Tool Protection Bellows Market report delivers the detailed segment data, supplier profiles, and scenario models necessary to operationalize these recommendations. To access the complete analysis, the interactive dataset, and tailored advisory support, visit PW Consulting’s report page or contact our industrial components team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Machine Tool Protection Bellows Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com