Edge Data Center Market Growth, Trends, and Forecast to 2034

Other |

2026-07-01 12:17:07

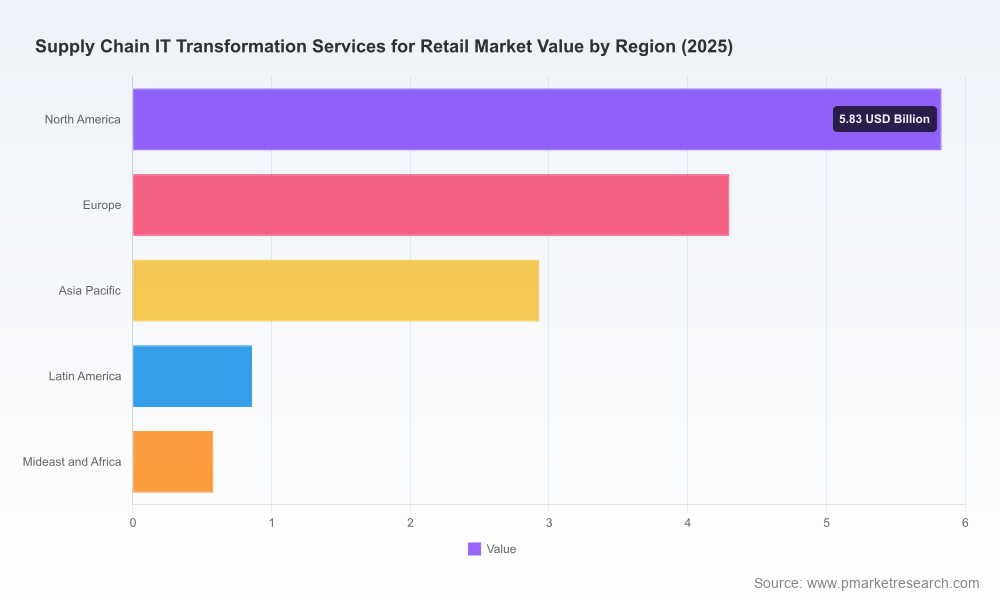

Today PW Consulting publishes a strategic preview of our forthcoming market research report, Supply Chain IT Transformation Services for Retail Market (base year 2025). As retailers confront continued pressure to reconcile cost, resilience, and customer experience, the services market that enables IT-led supply chain transformation has shown sustained expansion — growing from roughly USD 9.0 Billion in 2020 to USD 14.5 Billion in 2025, and projected to approach USD 28.0 Billion by 2032 at a compound annual growth rate (CAGR) of 9.85%. This brief synthesizes the report’s key implications for executive investment choices in 2026 while intentionally withholding granular segmentation detail to encourage decision-makers to consult the full report for tactical implementation data and provider scorecards.

Supply Chain IT Transformation Services for Retail Market

From optimization to transformation: Early projects focused on discrete optimization (warehouse or order management) are now migrating toward programmatic, platform-centric transformations that stitch planning, execution, and customer-facing operations together. The market’s near-term growth trajectory reflects this shift from siloed point solutions to integrated, services-led engagements.

Supply Chain IT Transformation Services for Retail Market

Acceleration of AI and automation: Industry data shows adoption of AI for supply chain visibility moving from roughly 30% to 41% within a one-year horizon. That acceleration translates into a strategic window in 2026 where investments in data maturity and AI ops differentiate winners.

Supply Chain IT Transformation Services for Retail Market

Regulatory and labor pressure: New and evolving regulations (e.g., packaging compliance regimes and extended producer responsibility mandates, tighter data-privacy regimes, and labor changes affecting retail work patterns) make 2026 a year for councils and CIOs to align transformation roadmaps with compliance, traceability, and workforce optimization requirements.

The full PW Consulting report is built for procurement, CIOs, supply chain heads, and program sponsors who must translate strategy into prioritized investments in 2026. Highlights include:

Investment roadmaps and timing guidance that map capabilities (e.g., visibility, demand-sensing, orchestration, workforce automation) to business outcomes and expected time-to-value.

Implementation playbooks with modular project templates, change-management checklists, and governance models tailored to retail operating models (store-centric, omnichannel, pure-play e-commerce, hybrid franchises).

Business-case frameworks and TCO calculators designed to stress-test outcomes under multiple scenarios: inflationary cost pressures, inventory stress events, and varying fulfillment mix.

Vendor-agnostic evaluation criteria and procurement templates for selecting integrators, managed services providers, and specialist consultancies — with scoring that emphasizes execution maturity, IP assets, and partnership ecosystems.

Use-case libraries and case studies that illustrate measurable KPIs, phasing of capabilities, and common pitfalls observed across historical transformations (2020–2025).

Moderate fragmentation: Market concentration remains modest; the top three vendors capture under one-third of market value while the top five capture less than two-fifths. This structure preserves avenues for specialist players and system integrators to win meaningful engagements through specialization or partnership strategies.

Compliance as a functional requirement: Packaging and extended producer responsibility rules, along with data privacy regimes, are elevating traceability and provenance into mandatory design constraints for supply chain IT programs. Retailers should budget for compliance gating and digital passport capabilities early in transformation roadmaps.

Labor economics and workforce automation: Rising labor costs and new labor regulations in several jurisdictions make investments in workforce orchestration, scheduling, and automation not merely efficiency projects but risk mitigation initiatives that protect margins and service levels.

AI adoption curve: With AI adoption for visibility poised for rapid uptake, the 2026 decision window is about building robust data foundations, governance, and incremental pilots that can scale without accruing unmanageable technical debt.

The market is shaped by a mix of global integrators, Big Four advisory practices, legacy technology firms, and specialist boutiques. Our evaluation in the report focuses on execution credibility for retail-specific challenges, IP and productized offers, partnerships with core ERP/SCM vendors, and demonstrated outcomes in omnichannel fulfillment. A high-level positioning of notable providers:

Tata Consultancy Services (TCS) — recognized for end-to-end supply chain transformation capabilities, strong advisory-led approaches, and partnerships that support large-scale retail and CPG programs. Recent analyst recognition underscores maturity in execution for complex global transformations.

Cognizant — emphasizes digital supply chain modernization, planning, and resilience; a choice for retailers seeking blended delivery models combining domain consulting and technology modernization.

Accenture — positions around network orchestration and AI-infused transformation, with deep capabilities in integrating data, automation, and cloud-native services to raise agility at scale.

Deloitte — leverages broad industry advisory and systems-integration strengths with productized solutions for visibility and AI-driven resiliency, frequently chosen where strategy-to-execution continuity is paramount.

PwC — guides clients toward “supply chain of 2030” architectures focusing on flexible networks, automation, and AI, often aligning transformation roadmaps with C-suite strategic objectives.

IBM — brings analytics and predictive tooling married to consulting practices, attractive to retailers prioritizing data science and hybrid cloud foundations.

Specialist consultancies (e.g., Parker Avery) and digital natives (e.g., Brillio) — provide niche excellence in forecasting, inventory optimization, and rapid modernizations; often serve as accelerators or co-delivery partners to larger integrators.

Readers should use the detailed vendor profiles and scoring in the full report to match provider capabilities to their specific scope and risk appetite. Shortlisted providers should be validated against proof points, reference outcomes, and time-to-value metrics rather than purely brand presence.

Prioritize data foundations before broad AI bets. Organizations that balance data governance, master data, and real-time eventing with phased AI pilots will unlock predictable ROI and avoid costly rework.

Design for regulatory flexibility. Build modular compliance layers (traceability, digital passports, data residency) so that packaging, producer-responsibility, and privacy mandates can be toggled without multiplying technical debt.

Adopt a bimodal delivery approach: Combine quick-win managed services and proof-of-value pilots with a parallel strategic program that establishes a long-term platform and integration architecture.

Re-evaluate outsourcing scope. With market concentration moderate, today’s valid strategy is to assemble ecosystem stacks — pairing global integrators for scale with specialists for domain excellence — rather than defaulting to single-vendor models.

Lock governance and procurement to outcomes. Contracts should emphasize measurable KPIs tied to availability, uplift in forecast accuracy, inventory turns, and fulfillment SLA adherence, with incentives for continuous improvement.

CIOs and supply chain leaders will find the report especially valuable when preparing 2026 budgets, vendor selection shortlists, and multi-year transformation roadmaps. Tactical applications include preparing RFPs that reflect compliance needs, building business-case artifacts that reflect the current market growth and cost inflation dynamics, and structuring multi-vendor delivery models that mitigate concentration risk while accelerating capability adoption.

In keeping with the report’s role as a decision-enabling asset, this preview presents high-confidence macro trends, market trajectory (historical and forecast), and strategic implications without publishing detailed regional and application-level splits, supplier scorecards, or proprietary pricing bands. Those granular analytics, including segment-by-segment growth drivers and provider-level benchmarking, are reserved for full-report subscribers and advisory clients who require executable procurement and implementation plans.

PW Consulting’s full Supply Chain IT Transformation Services for Retail Market report (base year 2025) contains the actionable models, vendor evaluations, and playbooks necessary to convert strategic intent into deployable programs in 2026. For executives preparing budgets, RFPs, or governance structures this year, the report provides the empirical foundation and practical templates to accelerate decision cycles and reduce execution risk.

To obtain the full report, vendor benchmarking tables, and customized advisory sessions, please visit our research portal. PW Consulting’s analysts are available to brief boards, steering committees, and procurement teams on how the market’s growth dynamics and competitive landscape translate into near-term choices and long-term value creation.

For detailed analysis of this topic, please visit the official page:Supply Chain IT Transformation Services for Retail Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com