Wet Granulation Equipment Market Competitive Benchmarking and Industry Outlook

Other |

2026-06-15 11:52:36

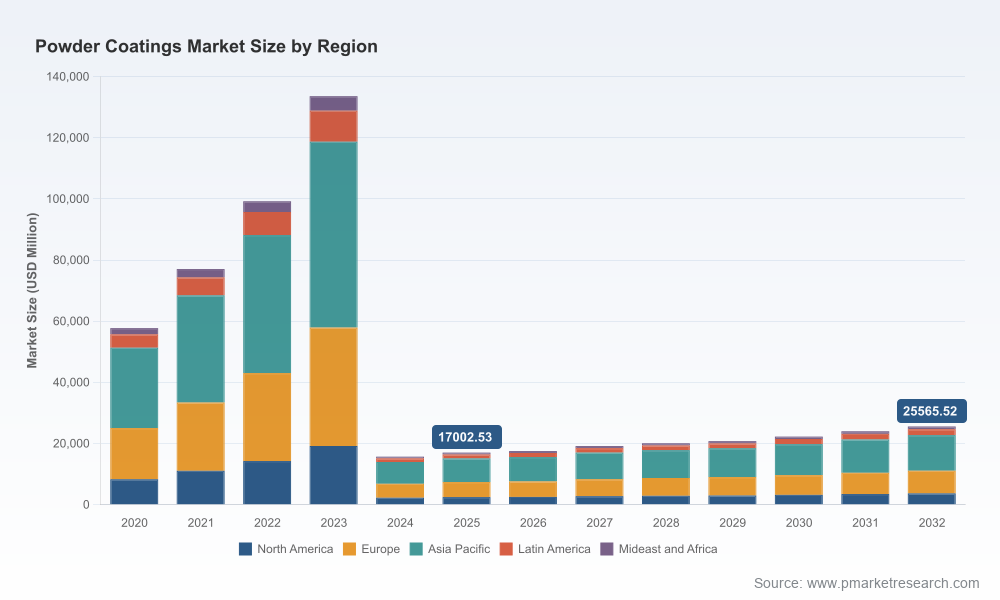

The global powder coatings market is at an inflection point. Using 2025 as our analytical base year, PW Consulting’s latest study shows that the market has been tracking a multi-year recovery and professionalization cycle and — under our central assumptions — will expand at a compound annual growth rate (CAGR) of 6.73% through the 2026–2032 forecast window. By taking a 360° view that links demand trends, raw material cost dynamics, regulatory pressure and supplier strategy, this research provides the practical, decision-ready intelligence boards and executive teams need to shape pricing, procurement, product and M&A choices in 2026.

Powder Coatings Market

Macro momentum with tactical urgency: the market’s medium‑term growth trajectory creates opportunity, but near‑term margin pressure from raw material and energy cost inflation requires calibrated responses now rather than later.

Powder Coatings Market

Regulation is a growth lever: tighter emissions and VOC rules in major markets are accelerating adoption of solvent‑free and low‑emission powder systems — a structural demand driver for technology and formulation investments.

Powder Coatings Market

Industry structure favors targeted consolidation: the market shows measurable concentration among leading suppliers, creating both opportunity for bolt‑on M&A and risks for smaller players unless they define defensible niches.

Procurement complexity is rising: resin and specialty additive volatility means raw material exposure must be actively modeled and hedged as part of commercial plans.

Base year: 2025 (our detailed models are normalized to this point).

Projected 2026–2032 CAGR: 6.73%.

Long‑run endpoint under the central case: the market expands materially by the end of the forecast horizon, reflecting both volume recovery and premiumization as end‑users demand higher performance and sustainability attributes.

Demand models and scenario trees calibrated to 2020–2025 historicals and three forward scenarios (base, upside, downside) that drive revenue, margin and working capital implications for producers, formulators and downstream manufacturers.

Raw material cost-mapping and sensitivity matrices linking key feedstocks (resins, additives, pigments, NEOL and others) to product margins at multiple price points.

Regulatory heatmaps identifying jurisdictions where powder formulations become the “best available technique” and the timing for compliance and product relabeling.

Supplier benchmarking and balanced scorecards that combine technical capability, geographic reach, ESG credentials and price elasticity to guide sourcing and partnership decisions.

A strategic playbook for product portfolio choices (thermoset vs thermoplastic trade-offs), go‑to‑market tactics, pricing architecture, and an M&A shortlist framework designed to accelerate capability acquisition.

Raw material inflation: resin and specialty chemical costs have increased with disruptive episodes in 2025–2026. Epoxy resin prices have trended upward and specific inputs like neopentylglycol (NEOL) have seen supplier price adjustments. Real‑time cost pass‑through and contract management are therefore now first‑order strategic tasks.

Producer price actions: major industry players have implemented price increases in 2026 in response to logistics, energy and feedstock pressures — a development that alters commercial negotiations and short‑term margin outcomes throughout the supply chain.

End‑user price sensitivity and product mix shift: coatings buyers are balancing higher unit prices against lifecycle benefits. Where regulations and total cost of ownership favor powder systems, premium positioning is possible; where cost pressure dominates, lower‑price, high‑throughput formulations will compete fiercely.

Regulatory acceleration: in several regions solvent‑free powder systems are being recognized as preferred techniques under industrial emissions frameworks, redirecting capital expenditure in manufacturing plants and triggering reformulation roadmaps for suppliers and brand owners.

Market pricing context: industry data shows powder coating prices in 2025 broadly ranging by resin type and performance — a useful anchor for pricing models and elasticity testing when building bids or revising long‑term supply agreements.

The market displays moderate consolidation: the top three and top five firms account for meaningful but not overwhelming shares of global supply, creating space for regional champions and specialized innovators. Strategic implications for incumbents and challengers differ:

Axalta Coating Systems (Philadelphia): Known for its Alesta powder coatings and a push into bio‑based options. Axalta’s advantage is brand recognition in automotive and industrial channels; executives should evaluate premium sustainability pricing and selective geography expansion.

PPG Industries (Pittsburgh): Offers environmentally‑oriented lines with recycled content and PFAS‑free formulations. PPG’s recent global price increases reflect cost pressure and a strong channel position; rivals should model counter‑offers and prioritize value messaging tied to performance and lifecycle savings.

BASF SE (Ludwigshafen): A critical upstream player supplying resins and additives including NEOL. BASF’s raw material price moves propagate through the value chain — buyers must develop multiple supplier relationships and consider strategic procurement alliances or forward contracts.

The Sherwin‑Williams Company (Cleveland): Leverages a broad distribution network; its powder coatings business should be considered in channel optimization scenarios and localized reformulation plans to meet regional regulatory demands.

Jotun, Kansai, Nippon Paint, Teknos, Tiger Coatings, American Powder Coatings: These firms combine regional leadership, specialty systems (protective, decorative, waterborne/solvent‑free) and niche expertise. For C‑suite teams they represent both acquisition targets and potential strategic partners for co‑development.

Fix procurement and pricing mechanics in quarter one: implement dynamic pricing clauses tied to validated feedstock indices; renegotiate terms with top resin suppliers; create a rolling 12‑ to 24‑month procurement hedge program for critical inputs.

Accelerate customer value engineering: quantify lifecycle and TCO benefits of powder systems for key accounts, and build tiered commercial offers (performance tiers, service bundles, extended warranties) to defend margin.

Reprioritize R&D to regulatory and sustainability wins: redirect incremental R&D budget to PFAS‑free, recycled‑content and lower‑curing‑temperature formulations that unlock retrofit opportunities in appliance and architectural segments.

Pursue pragmatic consolidation and partnerships: use the moderate market concentration to pursue bolt‑on acquisitions that add formulation IP or regional footholds, and pursue co‑development deals with resin suppliers to stabilize supply and share cost savings.

Operationalize scenario planning and stress testing: embed three stress scenarios (raw material shock, rapid regulatory tightening, demand slowdown) into capital allocation decisions for new lines, curing ovens and capacity expansions.

The full study contains the granular inputs executives use to execute: complete segmentation by region/type/application, country‑level demand and capacity maps, price‑by‑grade curves, supplier scorecards with capability matrices, contract templates and downloadable financial models ready for board‑level deliberation. In this introduction we intentionally preview methodology, strategic implications and the operational playbook while withholding the segment‑level percentages and full company scorecards that are reserved for subscribers. That “teaser” approach is deliberate — it lets you validate our strategic framing and then operationalize it using the full dataset on our report page.

PW Consulting recommends that executive teams use this briefing as the basis for a 90‑day action plan: (1) run the procurement stress test, (2) present a prioritized R&D roadmap tied to three customer pilots, (3) launch a pricing pilot with one major account incorporating a raw‑material index clause, and (4) run a short M&A screening exercise against the capabilities list in our full report. These steps will move leadership from analysis to controlled action before market moves create cost or margin surprises.

For access to the complete data tables, segment breakouts, supplier scorecards and downloadable scenario models, please consult the PW Consulting report page for Powder Coatings Market — the detailed intelligence that operational teams need to convert insight into measurable advantage in 2026.

For detailed analysis of this topic, please visit the official page:Powder Coatings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com