Commercial Kitchen Ventilation Systems Market — Strategic Briefing for 2026 Decision-Makers

As companies navigate the intersecting pressures of energy regulation, food-safety compliance, and tightening operational margins, commercial kitchen ventilation systems have moved from a commoditized capital purchase to a strategic lever for cost, risk, and brand outcomes. PW Consulting’s latest market study (base year 2025) synthesizes five years of historical performance and a forward-looking 2026–2032 forecast to equip executives with the insight required to prioritize investments, partnerships, and go-to-market moves in 2026.

Commercial Kitchen Ventilation Systems Market

Market snapshot: growth profile and structure

The commercial kitchen ventilation market has demonstrated steady expansion from 2020 through 2025, with the base year market size crossing the mid-single‑billion-dollar threshold in 2025 (USD, report unit). Our forecast models—anchored to a compound annual growth rate (CAGR) of 6.8% across the 2026–2032 window—project continued, durable demand driven by retrofit cycles, new-build foodservice growth in emerging urban centers, and energy-efficiency upgrades. Concentration metrics show a moderately consolidated market: the top three firms account for a material majority share, and the top five further consolidate supplier power. Those dynamics create both barriers and pockets of opportunity for innovators and scale-seeking buyers.

Commercial Kitchen Ventilation Systems Market

Why this study matters for 2026 decisions

- Regulatory acceleration is a strategic risk — Proposed energy codes and jurisdictional moves to mandate demand-control ventilation (DCKV) are becoming a leading indicator for procurement cycles. Operators who plan now for compliance-driven retrofits will avoid costly emergency capital outlays and secure first-mover energy savings.

- Energy and operating expense reduction is now measurable — Advanced controls, integrated make‑up air, and demand-driven solutions materially compress lifecycle costs when deployed at scale; our analysis quantifies typical payback ranges and scenario sensitivities for different kitchen archetypes (detailed models are included in the full report).

- Service and lifecycle revenue are a differentiator — With a meaningful concentration among market leaders, the path to margin expansion for mid-tier suppliers is service monetization (maintenance contracts, remote monitoring, performance guarantees) rather than competing on capital price alone.

- Retrofit demand outpaces greenfield in many mature markets — Aging ventilation infrastructure, combined with new safety and energy codes, means that retrofit programs will drive the bulk of addressable volume in the near term. Strategic sourcing, retrofit tooling, and installation networks will determine winners.

What PW Consulting’s report delivers — practical, decision-ready content

- Comprehensive market-sizing and a transparent forecast model calibrated to historical installation volumes, product-life cycles, and macro drivers (energy prices, construction activity, foodservice growth). The report supplies the assumptions and sensitivity levers so teams can re-scope forecasts to their own geographies and channel mixes.

- Actionable buyer personas and procurement playbooks for owners, facility managers, design‑build contractors, and institutional specifiers — including RFP templates and specification checklists that shorten procurement cycles and mitigate compliance risk.

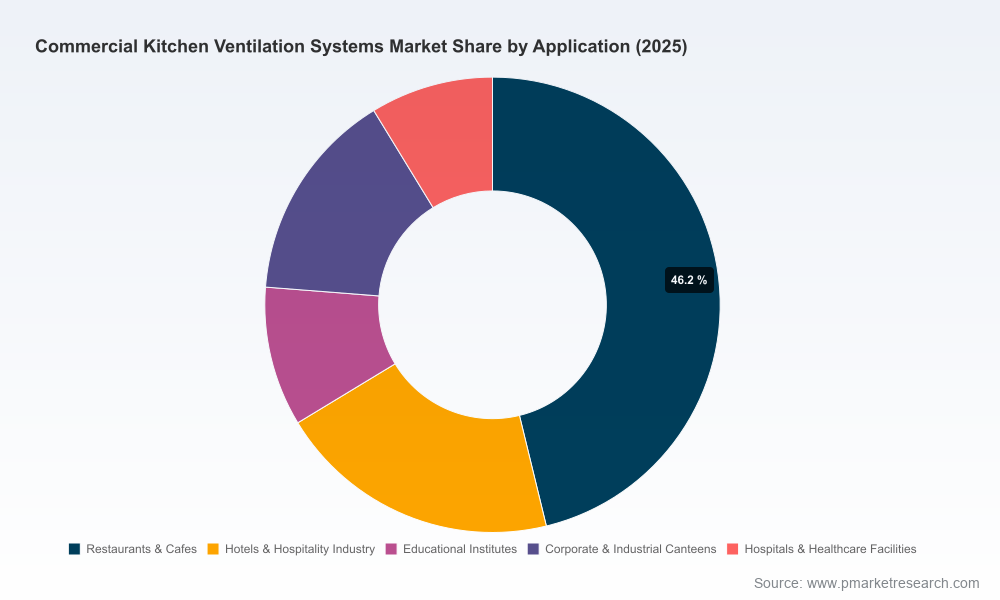

- Detailed vendor capability matrices and evidence-based scorecards that compare suppliers on product breadth, retrofit capability, DCKV expertise, service footprint, and compliance support. (Note: granular revenue splits by product, region and application are excluded from this public summary and are available in the full dataset.)

- Investment and M&A frameworks — valuation anchors using revenue, margin, and aftermarket-service multipliers; playbooks for bolt-on acquisitions to accelerate regional penetration or add controls expertise; and due-diligence checklists customized for ventilation assets and installed-base monetization.

- Implementation guides for energy retrofit pilots — including sample measurement & verification (M&V) protocols, expected energy savings ranges, and suggested procurement timelines to align with upcoming code changes.

Competitive landscape — who matters and why

Our qualitative and quantitative competitive analysis highlights a mix of global manufacturers, regional specialists, and system integrators. Key players profiled in the study include organizations with entrenched catalogues of hoods and fans, firms specializing in demand-control ventilation and air-quality controls, and service-led businesses that convert installed equipment into recurring revenue streams.

Commercial Kitchen Ventilation Systems Market

- CaptiveAire Systems, Inc. (Raleigh, NC) — Market leader with end‑to‑end offerings across hoods, fans, and grease management. Their breadth across product and service helps capture specification-led projects and large chain rollouts.

- Greenheck Fan Corporation (Schofield, WI) — Strong in fan and make-up air technologies with incremental capability in energy-recovery ventilation; well-positioned for projects where energy codes are tightening.

- Systemair AB (Skinnskatteberg, Sweden) — European engineering approach emphasizing high-efficiency airflows, smart purifiers, and demand-controlled systems suited to premium and regulation-heavy markets.

- Gaylord Industries (Tualatin, OR) — DCKV specialist with custom hood engineering and pollution control expertise—an attractive partner for chains seeking energy and emissions guarantees.

- FAST Kitchen Hoods (Mississauga, ON) and regional manufacturers — Provide compliance‑rated cULus and local code solutions that shorten lead times and appeal to independent restaurateurs.

- Chef’s Deal Restaurant Equipment (Nashville, TN) — Recently expanded service portfolio to include end-to-end engineered ventilation solutions; illustrates a broader industry trend where installers move upstream into design and consulting.

- Melink Corporation — Controls and Intelli‑Hood leader providing DCKV systems and monitoring services, a critical capability as energy codes nudge towards mandatory demand control in some jurisdictions.

- North American Kitchen Solutions (NAKS) — Flexible manufacturer with a strong presence in modular and portable ventilation systems for specialty applications.

Market concentration metrics in the study (top-3 and top-5 shares) indicate a market that rewards scale and channel reach, but still offers attractive niches for specialized controls, service models, and regional manufacturers. The competitive analysis pairs qualitative positioning with operational KPIs—lead times, retrofit capacity, aftermarket attachment rates—so buyers and investors can prioritize targets and procurement partners with precision.

Regulation, standards, and tech adoption — drivers of near-term demand

- Regulatory momentum: Emerging proposals from energy authorities (notably at state and provincial levels) aim to lift minimum efficiency requirements and in certain instances to mandate demand-control ventilation. These regulatory shifts compress decision timelines for owners and create a clear retrofit pipeline.

- Safety and compliance frameworks: Longstanding standards such as the NFPA 96 and the FDA Food Code continue to determine equipment specification, while installation codes (e.g., Uniform Mechanical Code) shape safe implementation and inspection regimes.

- Technology maturation: Remote monitoring, IoT-enabled controls, and closed-loop DCKV platforms now deliver verifiable energy outcomes; these capabilities are the primary enablers of service contracts and performance guarantees.

- Supply and installation: Lead times for fabricated hoods and specialized controls vary materially by region. Our implementation-playbook quantifies realistic procurement-to-commissioning timelines for common project archetypes.

Strategic recommendations for 2026

- Prioritize compliance-driven retrofit pipelines. Map upcoming code changes against your installed base and prioritize kitchens with the shortest payback and highest energy-intensity signature.

- Shift to outcomes-based commercial models. For manufacturers and integrators, pilot performance contracts (energy savings guarantees, uptime SLAs) to convert one-off installations into recurring revenue.

- Invest in controls and integration capabilities. DCKV and remote-monitoring competencies will be table stakes for competitive differentiation and for meeting emerging mandatory requirements.

- Design M&A to buy capability, not just capacity. Targets that add DCKV expertise, service networks, or regional code knowledge present better value than pure volume lifts.

- Operationalize retrofit execution. Build or partner for fast-install teams and standardized retrofit kits to shorten downtime for restaurant clients and reduce project management complexity.

How to use this study

The report is built for three primary user groups: (1) corporate strategists and CFOs seeking capital allocation models for retrofit programs; (2) product and commercial heads at manufacturers and integrators evaluating capability gaps and M&A targets; and (3) owners/real-estate managers who need procurement playbooks and compliance risk maps. The supporting data files include scenario-ready forecast models, vendor scorecards, and implementation templates. Note: the compact summary intentionally omits granular segmentation tables and line‑item regional/application values to preserve the commercial analytics that are available in the full report.

Conclusion — takeaways for 2026

Commercial kitchen ventilation is transitioning from an under-managed facilities item into a strategic asset class where regulation, energy savings, and service monetization converge. The 2026 planning cycle is a pivotal moment: firms that act now—prioritizing DCKV, controls integration, and retrofit execution—will convert regulatory risk into competitive advantage. PW Consulting’s full study provides the calibrated numbers, vendor comparators, and executable playbooks to guide capital and commercial choices. For executives preparing budgets, shaping product roadmaps, or evaluating acquisition targets in 2026, the study is the practical intelligence layer that turns market forecasts into immediate action plans.

To access the complete dataset, segmented forecasts, and vendor scorecards that underpin these strategic recommendations, please refer to the full report on our website.

For detailed analysis of this topic, please visit the official page:Commercial Kitchen Ventilation Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com