Smart Sports Clothing Market Trends Driving Connected Fitness Innovation

Other |

2026-06-14 04:20:21

As organizations prepare budgets and strategic roadmaps for 2026, denim continues to present a paradox: a mature, established category with steady consumer demand yet exposed to acute supply‑side and regulatory shocks. Our base‑year assessment places the global denim jeans market at USD 170.0 Million in 2025. Under conservative demand and cost assumptions, the market is projected to grow at a compound annual growth rate (CAGR) of 5.8% through the 2026–2032 forecast window, reaching roughly USD 252.0 Million by 2032. That trajectory creates both opportunity and complexity for brands, manufacturers, retailers and investors deciding where to allocate capital, how to hedge supply‑chain risk, and which innovation themes to prioritize.

Denim Jeans Market

This is not a slideware summary. Our full market study is built to be executed against. Highlights of the deliverables include:

Denim Jeans Market

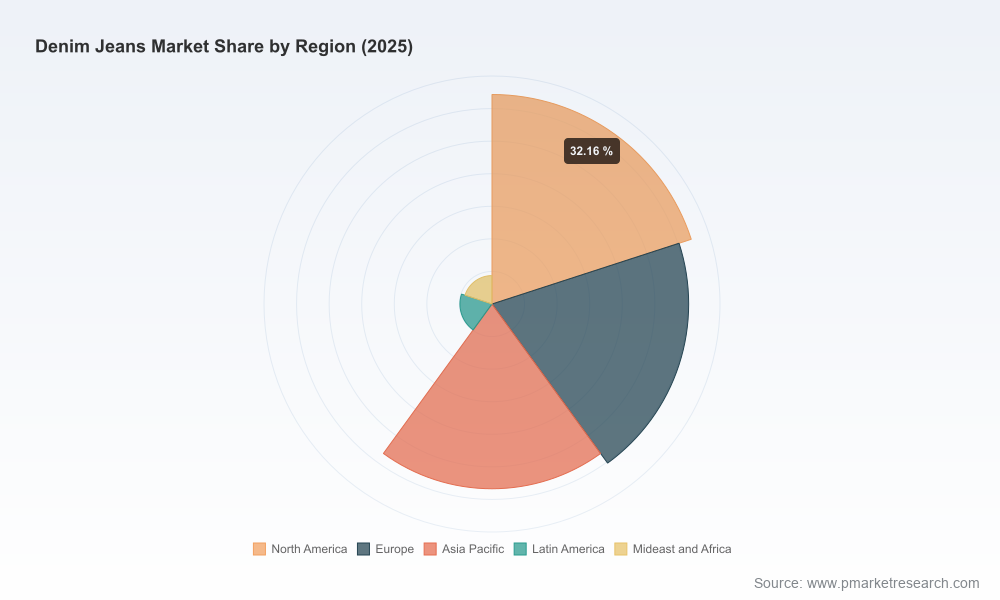

Note: the public preview deliberately omits deeply disaggregated region‑by‑region and application/split figures — these are available in the full report and accompanying data pack on our site.

Denim Jeans Market

The denim category features distinct strategic archetypes: global brand owners, fast‑fashion integrators, premium fabric innovators, circular specialists, and vertically integrated manufacturers. Understanding how each archetype deploys resources is central to strategic positioning.

Levi Strauss & Co. — A global brand owner that operates through contract manufacturing across a broad footprint. Levi’s remains focused on design, marketing and supply‑chain transparency as brand differentiators. For buyers and partners, Levi’s continued expansion of premium lines signals sustained consumer willingness to pay for heritage narratives and crafted materials.

Gap Inc. — A diversified retail owner that balances higher‑margin brand assortments and scale value channels. Its sourcing diversification, including expansion into lower‑cost manufacturing countries, illustrates the tradeoff between unit economics and supply resilience that many large retailers are negotiating in 2026.

H&M Group — An outsourcing and speed player that leverages an extensive tier‑1 supplier base, primarily in Asia. H&M’s transparent supplier reporting and fast assortment cadence are indicative of a scale‑led model that prioritizes rapid replenishment and cost control, but which increases exposure to regional production disruptions.

MUD Jeans — A circular‑first challenger producing premium recycled denim. MUD’s model demonstrates how subscription, take‑back and recycled feedstocks can attract sustainability‑minded consumers and command pricing premiums if executed at scale and with verified lifecycle benefits.

Candiani Denim — A fabric and innovation specialist whose investments in regenerative cotton, post‑consumer recycled yarns, and biodegradable stretch technologies show the pathway for premiumization through material science. Brands aiming for a sustainability premium will need to assess supplier capability, not just credentials.

Firemount Group Ltd. — A vertically integrated manufacturer with documented production in Mauritius. Recent enforcement actions (see dynamics below) underscore the reputational and operational hazards faced by manufacturers and their buyers when compliance gaps arise.

Denim and Beyond LLC — A U.S. importer and distributor managing brand imports and logistics. Companies in similar roles are central risk managers during periods of enforcement or tariff changes, balancing detention risk, bonded inventory strategies and customer communications.

Our Denim Jeans Market package combines a downloadable data pack, editable financial models, supplier risk maps and a bespoke advisory session to convert insights into an executable 12‑month plan. We pair industry‑leading benchmarking with hands‑on playbooks for procurement, sustainability adoption, and channel optimization. If your agenda for 2026 includes capacity investments, premium product launches, compliance remediation, or M&A, our team will co‑develop the operational steps and governance to deliver results.

This preview is designed to help senior leaders and investors prioritize where to probe deeper. For full access to the disaggregated forecasts, supplier lists, and the practical toolkits referenced above, please visit the PW Consulting report page to download the complete report and associated data pack. The full dataset includes the granular splits, scenario models and supplier‑level detail necessary to finalize 2026 capital and sourcing decisions.

For detailed analysis of this topic, please visit the official page:Denim Jeans Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com