Why Is the Anti-Aging Services Market Growing with Rising Aesthetic Demand?

Networking |

2026-04-27 06:54:29

As global supply chains rebound from pandemic-era shocks and energy volatility becomes a constant, bromine has quietly reasserted itself as a strategic industrial input. Our 2026-focused market research places bromine at the intersection of commodity risk, regulatory pressure, and accelerating demand from specialty end‑markets. This preview outlines why companies active in chemicals, pharmaceuticals, oilfield services, flame retardants, and water treatment should treat bromine strategy as a board-level priority for 2026 planning cycles.

Bromine Market

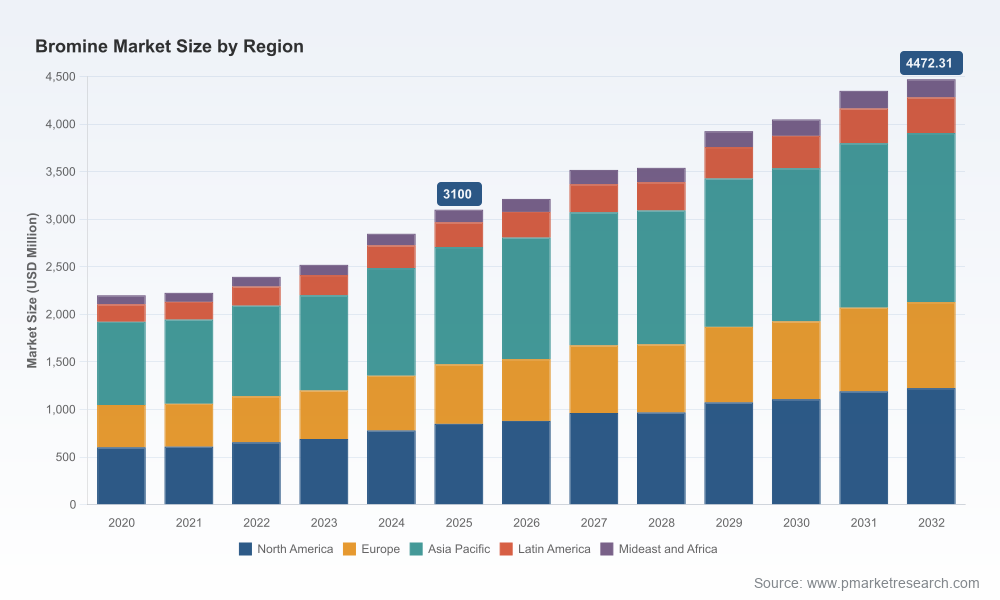

Bromine’s market footprint has expanded meaningfully in recent years. From an industry base of roughly USD 2.2 billion in 2020, the market reached approximately USD 3.1 billion in our 2025 base year — a trajectory that our models carry forward into a forecast horizon out to 2032. The industry is projected to grow at a compound annual growth rate (CAGR) of about 5.5% across the 2026–2032 period, driven by a mix of pharmaceutical synthesis, specialty chemical demand, evolving flame retardant formulations, and steady oilfield-related consumption.

Bromine Market

That topline growth masks a more complex risk/reward profile. Bromine remains a specialty commodity: extraction is geographically concentrated, processing requires energy- and water-intensive brine operations, and end-use demand is tied to regulated industries where substitutions and reformulations are common. For 2026 decision-makers, the combination of robust mid-single-digit growth and concentrated supply means opportunities for margin capture — and, simultaneously, exposure to concentrated operational and geopolitical risk.

Bromine Market

PW Consulting’s full Bromine Market report is structured to support commercial and capital allocation decisions in 2026. The analysis was built from a blend of primary supplier interviews, plant- and asset-level mapping, trade-flow analytics, and scenario-driven financial models. The following are representative actionable components that executives will find immediately useful:

The bromine industry exhibits notable concentration. The top three producers control a material majority of global supply, and the top five extend that dominant position further. This concentration creates two broad strategic realities for market participants in 2026:

Key incumbents span diversified chemical majors, regional brine specialists, and niche fine‑chemical manufacturers. Large integrated producers combine upstream brine assets with downstream derivative capabilities, enabling them to capture value across multiple end markets. Regional producers and specialist fine-chem players cater to local pharma and specialty demand, providing agility and custom chemistry that large players sometimes cannot match.

Notable market developments that refine competitive dynamics include strategic capacity investments and product launches. Examples include recent joint investment agreements between major mining/chemical players to expand production capacity at existing brine operations, and new pharmaceutical formulations being introduced into regulated markets. These moves compress the window for challengers to secure long-term offtake or to gain footholds in high-margin downstream markets.

For executives preparing strategy and budgets for 2026, the market presents a finite set of high‑impact moves. Our report anchors each with quantified scenarios and tactical next steps; highlights include:

This research goes beyond headline forecasts. It delivers plant-level visibility, supplier financial health indicators, and playbooks that translate macro trends into executable commercial actions. We combine proprietary trade-flow analytics with on-the-ground interviews and regulatory tracking to produce outcome-focused recommendations for 2026. The full report quantifies exposures for different stakeholder archetypes — producers, specialty buyers, and trading houses — and offers prioritized, ROI-backed initiatives to address each profile.

Importantly, the report preserves commercially sensitive segmentation insights behind gated models and interactive dashboards. That design follows our “trailer” approach: this preview surfaces strategic insights and the types of tools included, while core split-level data and proprietary scenario outputs are available through the full report and client engagements.

As companies finalize budgets and strategic plans for 2026, bromine should be treated as more than a commodity line item. It is a strategic input with concentrated supply dynamics, regulatory exposure and targeted growth pockets that reward anticipatory action. Whether your priority is securing feedstock, capturing downstream margin, or mitigating substitution risk, the decisions you make in 2026 will materially influence competitiveness across the rest of the forecast cycle.

For procurement leads, R&D heads, and corporate strategists, PW Consulting’s Bromine Market report provides the scenario-driven tools, supplier intelligence, and practical playbooks required to convert market visibility into measurable outcomes. To access the full set of models, plant maps, and proprietary split-level forecasts, visit our report page and request the detailed dataset and advisory options tailored to your company’s position in the value chain.

For detailed analysis of this topic, please visit the official page:Bromine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com