The Rise of Electric Lawn Mower Market Demand Surges

Other |

2026-04-28 08:34:09

As PW Consulting’s lead industry analyst, I present a concise strategic preview of our full Enameled Wire Market study (base year 2025). This briefing translates robust historical performance and forward projections into the decisive strategic signals executives need when allocating capital, restructuring supply chains, and negotiating customer contracts in 2026. We deliberately show the analytical thrust and actionable frameworks in this introduction while preserving the granular segmentation and proprietary financial models for the full report—designed to drive boardroom and investment committee outcomes.

Enameled Wire Market

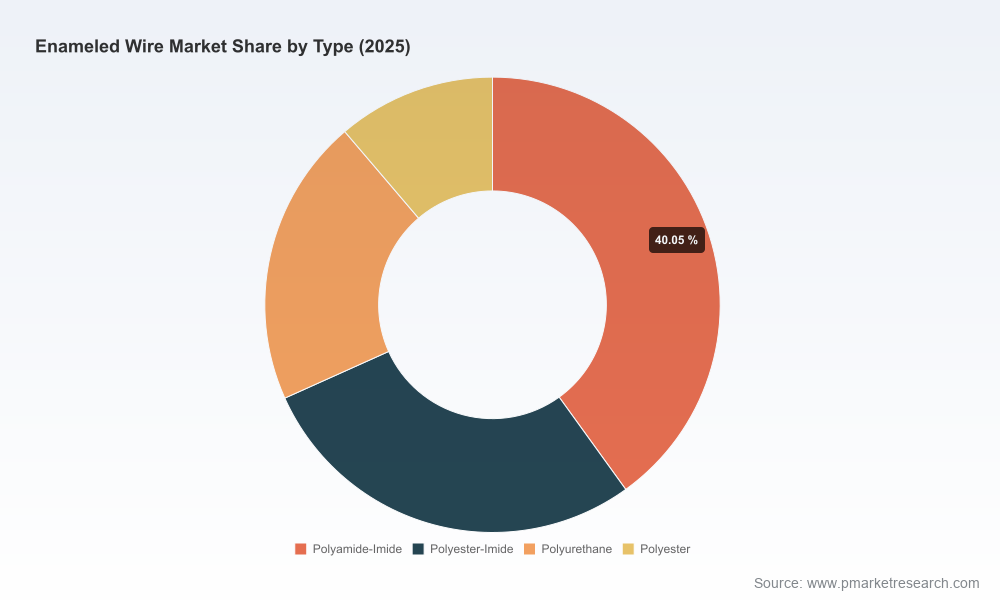

The enameled wire market has moved from steady recovery to structural expansion over the past half decade. From a measured base in 2020, industry revenue accelerated through 2024–2025, reaching a pivotal base year size in 2025. PW Consulting projects the market to continue expanding across the 2026–2032 forecast window at a compound annual growth rate (CAGR) of approximately 6.3%, with market value rising materially by 2032 under our central scenario.

Enameled Wire Market

Implication: a sustained growth runway at mid-single-digit CAGR shifts strategic priorities from short-term cost management to medium-term capacity planning, product differentiation, and vertical partnership strategies. For capital-intensive suppliers and OEMs, the 2026 planning cycle must explicitly factor in multi-year lead times for specialty coating lines and precision rectangular-wire tooling—delays that will translate directly into lost share where demand densifies (e.g., traction motors, high-efficiency transformers, and automation motors).

Enameled Wire Market

Timing of investments: Capital allocation decisions initiated in 2026 will settle into production between 2027–2029. Given the projected growth path, first-mover capacity expansions coupled with targeted quality differentiation will capture disproportionate upside.

Customer structuring: EV OEMs and large industrial buyers are contracting multi-year supply agreements. Suppliers who can demonstrate technical capability (fine gage, rectangular wire, tight enamel tolerances) and traceable cost structures will win preferred-supplier status.

Margin dynamics: Input-cost volatility and regulatory shifts create asymmetry between low-cost producers and premium-differentiated players. Firms must choose a defensible margin strategy—cost leadership through scale or value leadership through product-system integration.

We structured the study to translate market intelligence into direct executionables for 2026 decision cycles. Highlights include:

Demand modelling and scenario decks—historical reconciliation (2020–2025) and three forward scenarios (conservative, central, accelerated) with buildable drivers that allow clients to stress-test topline and capex outcomes.

Supply-side maps—global plant-level capacity, lead-times for coating and annealing lines, and a prioritized list of pinch-points by production technology (fine/ultra-fine, rectangular/specialized geometries).

Cost-pass-through and pricing sensitivity tool—dynamic Excel model linking copper and chemical enamel indices to finished-wire pricing under multiple contractual arrangements.

M&A and JV target shortlists—screened by technology gap, geographic footprint, and integration upside accompanied by valuation multiples and integration risk notes.

Regulatory and trade-impact playbook—actionable mitigations for tariff shifts, certification changes, and regional trade agreements tailored to procurement and sales operations.

Commercial templates—RFP scorecards, sample long-term supply agreement clauses, and escalation matrices that reflect real-world negotiation leverage in 2026 market conditions.

Market structure shows a moderate concentration level; the three largest players do not dominate the majority of the market, and the top five capture a clear but not overwhelming share. This balance supports both scale-led competition and niche differentiation—creating room for both incumbents and aggressive mid-sized players to expand.

Key strategic patterns across the competitive set:

Technology differentiation: Firms that have invested in precision rectangular wire and ultra-fine round-wire capabilities are advancing into higher-value traction and semiconductor-equipment segments. These capabilities are delivered not just by machinery but by integrated R&D into enamel chemistry and deposition technologies.

Regional capacity plays: Several global players are expanding capacity across Asia and North America to capture localized EV and industrial demand while managing logistics and lead-time risk.

Product sustainability and circularity: New product launches using recycled content and lower-carbon enamels are emerging as price-premium differentiators in OEM sourcing decisions.

Elektrisola (Germany) — Best-in-class in ultra-fine and breadth of product types. Strategy: leverage technology leadership to price-premium segments, license process know-how, and shorten development cycles through co-engineering with EV motor suppliers.

MWS Wire Industries (US) — Strong inventory and custom-insulation capability. Strategy: monetize service and logistics advantage via JIT programs, and use surcharge mechanisms tactically to protect margins in volatile cost environments.

Sumitomo Electric, Fujikura, Hitachi Metals, Furukawa (Japan/Asia) — Large scale and focused on EV/semiconductor equipment. Strategy: integrate closer with OEMs through long-term supply contracts while optimizing regional footprints under RCEP and local certification regimes.

Rea Magnet Wire, Essex Solutions, Condumex, Magnekón and others — Diverse players with strengths in niche product ranges or regional presence. Strategy: pursue targeted collaborations and bolt-on acquisitions to fill capability gaps rather than broad greenfield competition.

Chinese and Indian specialists — Cost and scale plays that will continue to pressure global pricing in non-differentiated segments. Strategy for Western and Japanese suppliers: continue to defend premium segments and pursue operational cost improvements.

Three near-term dynamics require immediate incorporation into planning models:

Input-price volatility: Recent price indices for copper-related cable sectors show month-on-month movement, impacting raw-material procurement costs. Hedging strategies, supplier partnerships for tiered pricing, and pass-through clauses in long-term contracts are essential.

Trade and tariff shifts: Regional trade agreements and tariff rebalances are changing import economics. Some tariff reductions lower landed cost from certain Southeast Asian suppliers, while targeted surcharges and operational levies by individual suppliers have appeared as defensive measures—each factor shifts landed-cost calculus and sourcing decisions.

Certification and compliance updates: New or updated electronics safety and product standards are now effective in key markets. Compliance lead times for certification and product requalification must be built into new product and market-entry timelines.

We recommend a prioritized, time-phased agenda that clients can operationalize in 2026:

Immediate (0–6 months): Update procurement contracts with indexed pass-through clauses, initiate raw-material hedging pilots, and complete a critical supplier continuity review assessing capacity and certification status.

Near term (6–18 months): Commit to selective capacity expansions where lead-time windows align with forecasted demand at premium price points; negotiate partnership agreements with OEMs for co-designed wire products (rectangular and high-temper enamel systems).

Medium term (18–36 months): Execute targeted M&A or JV to secure technology gaps and regional supply resilience; implement product-line rationalization to focus on higher-margin, differentiated offerings.

Our full report provides the confidential data, segmented forecasts, plant-level supply maps, and modeller assets necessary to convert the strategic priorities above into board-level decisions and operational plans. The public preview you are reading intentionally omits the granular regional, type and application splits and the downloadable Excel models—these are embedded within the client deliverable to preserve analytical integrity and commercial sensitivity.

The enameled wire market in 2026 sits at the intersection of technological demand (EV and high-efficiency motors), supply-chain reconfiguration, and regulatory/trade shifts. The path from 2026 to 2032 will reward firms that pair capital discipline with targeted technology and commercial partnerships. PW Consulting’s full study equips executives with the scenarios, cost models, and tactical playbooks to convert the market’s steady mid-single-digit CAGR into actionable growth and margin expansion—provided decisions are made now with a multi-year horizon.

To access the full dataset, segmentation breakdowns, and the scenario modelling toolkit referenced in this preview, please visit the PW Consulting report portal or contact our advisory desk for a briefing and controlled access to the deliverables.

For detailed analysis of this topic, please visit the official page:Enameled Wire Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com