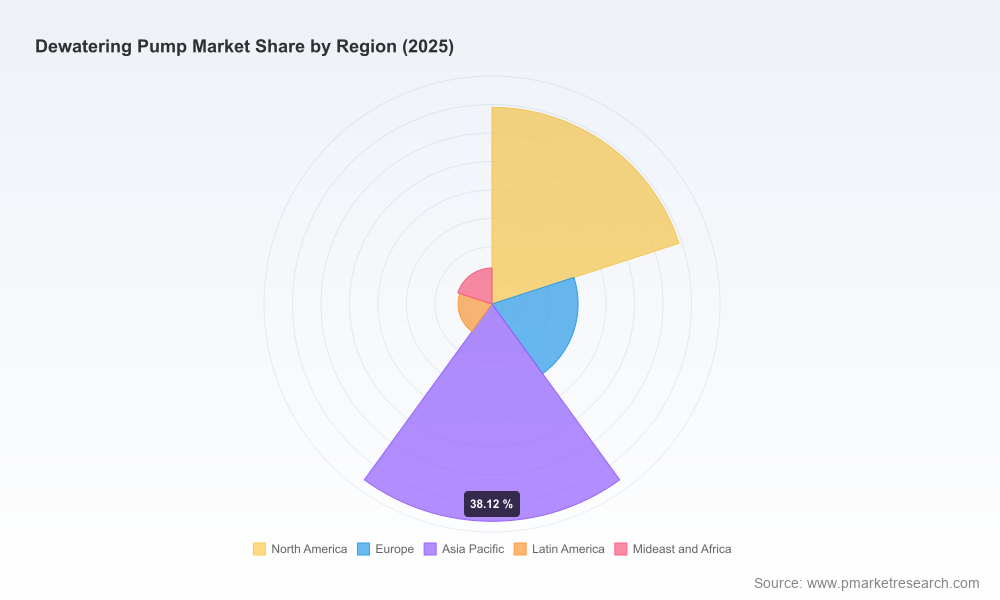

Dewatering Pump Market: Strategic Intelligence for 2026 Decision-Making

As PW Consulting’s lead industry analyst, I present an executive introduction to our latest Dewatering Pump Market research — a decision-grade briefing designed to inform corporate strategy, capital allocation, and commercial execution plans in 2026. This briefing synthesizes five years of historical performance and a forward-looking scenario through 2032, combining rigorous market modelling with pragmatic, actionable guidance for operators, OEMs, investors, and procurement leaders.

Dewatering Pump Market

Market trajectory at a glance

Between 2020 and 2025 the dewatering pump market demonstrated steady recovery and structural expansion, with the global market moving from approximately USD 6.17 billion in 2020 to USD 7.87 billion in 2025 (base year). Our forecast period (2026–2032) uses 2025 as the baseline and projects the market to continue growing at a compound annual growth rate (CAGR) of 6.4%, resulting in a materially larger addressable market by 2032. The near-term dynamic through 2026 reflects modest, resilient growth as electrification, digitalization, and tighter environmental compliance reshape demand patterns.

Dewatering Pump Market

Why this research matters for 2026 corporate decisions

- Investment prioritization: 6.4% CAGR signals a growth market, but not a broad-based boom. Firms must prioritize product lines and geographies where return on invested capital aligns with internal hurdle rates. Our modelling isolates where incremental demand and price resilient niches will arise.

- Technology and compliance timing: Tighter emissions and water-discharge regulations are accelerating the shift away from legacy diesel-only solutions toward electric, hybrid, and smart-managed systems. Corporates need timing windows for product transitions so compliance drives become revenue opportunities rather than cost burdens.

- Service and aftermarket economics: With market concentration moderate (CR3 ≈ 35%; CR5 ≈ 48%), scale matters but differentiated service networks and OEM-certified on-site capabilities are powerful margin levers. Our analysis quantifies how service penetration influences lifetime value and aftermarket margins.

- M&A and partnerships: Consolidation is selective. The CR metrics show space for bolt-on acquisitions and regional champions. Our market map highlights target profiles that generate the fastest payback for acquirers focused on mining, tunneling, or municipal wastewater niches.

Demand drivers and technology inflection points

The market is being reshaped by a handful of intersecting forces:

Dewatering Pump Market

- Regulatory pressure: Environmental frameworks — from EPA-driven discharge standards to EU water directives and emissions limits — are compelling investment in energy-efficient pumps, filtration integration, and real-time monitoring. Compliance is becoming a source of specification for procurement teams rather than a mere checklist.

- Electrification and hybridization: Progressive tightening of diesel emissions standards in construction and mining is increasing demand for electric submersible and hybrid systems. OEMs with validated electric portfolios and smart power management options can capture premium placements on larger projects.

- Material and wear-cost economics: Abrasive slurries in mining and quarries drive demand for high-chrome alloys (e.g., Cr27) with predictable wear lives. Our modelling integrates material replacement cycles and cost-per-hour metrics to show how material choices affect total cost of ownership.

- Digitalization and remote operations: Smart controls, telemetry, and predictive maintenance are shifting purchase criteria. Solutions that lower downtime risk and reduce on-site labor intensity get preferential entry into EPC and rental fleets.

Competitive landscape — what the leading vendors are doing

The dewatering pump field combines global incumbents with specialist regional players. Below is a concise strategic reading of the core market participants covered in the report.

- Xylem Inc. (USA): Leverages a broad portfolio spanning self-priming and submersible dewatering pumps, with strong position in municipal and industrial channels. Their emphasis on smart systems and sustainability aligns with regulatory-driven demand; expect continued platform investments and aftermarket expansion.

- Sulzer Ltd. (Switzerland): Competes on engineered centrifugal and sludge solutions plus embedded controls. Sulzer’s positioning is strong in heavy-duty mining and tunneling where reliability and tailored hydraulics command pricing power.

- Grundfos (Denmark): Known for energy-efficient electric units and global service network; well placed as the market migrates toward electric alternatives. Their R&D posture is an advantage in specification-dominated municipal projects.

- Atlas Copco (Sweden): Through its WEDA line, Atlas Copco targets mining and tunneling with robust electric submersible ranges. Integration with site electrification strategies enhances its appeal in projects seeking lower emissions footprints.

- Tsurumi (Japan): A specialist in submersible dewatering and slurry pumps with strong OEM reputation in construction and wastewater. Its product reliability under abrasive conditions keeps it relevant in rental and contractor channels.

- Gorman-Rupp (USA): Focused on centrifugal and self-priming pumps for municipal and industrial users; the company’s channel strength in the Americas is a competitive moat for infrastructure projects.

- Weir Group (UK) & KSB (Germany): Both emphasize heavy-duty slurry and industrial dewatering solutions. Weir’s mining heritage and KSB’s hydraulic expertise position them for specification wins where solids handling and energy efficiency are critical.

- Ebara & Wilo (Japan/Germany): Serve municipal and industrial water management needs with broad submersible portfolios; their global reach supports large EPC projects needing standardized equipment sourcing.

- Pioneer Pump (Franklin Electric): Increasingly differentiated via certified drinking-water products and a nascent expert services network offering 24/7 support — a clear play for higher aftermarket revenue and tender competitiveness.

- Flowserve & Wacker Neuson: Provide centrifugal and construction-oriented submersible pumps respectively; both are relevant in process and infrastructure subsegments where integration with broader asset fleets is required.

Across vendors, winning propositions combine reliable hydraulic performance, energy efficiency, robust wear materials, and increasingly, embedded digital controls. Scale matters for capital-intensive mining contracts, but agility and service responsiveness open routes to market for specialist players.

Recent market moves and what they imply

- Early‑2026 product updates and service network rollouts (notably by Pioneer Pump) indicate a trend: OEMs are monetizing reliability through certified on‑site support and product certification for regulated applications.

- Trade fair presences (IFAT, MINE & BUILD) from innovative mid‑tier manufacturers highlight continuing product-level innovation in sustainability and solids-handling — a signal to buyers that choice and differentiation will increase.

- New hydraulic and energy-efficiency product introductions (e.g., KSB’s generation launches) accelerate replacement cycles in large institutional clients, creating short-term retrofit opportunities for suppliers.

Supply chain, raw materials and regulatory risk

Operators must manage three supply-side realities: (1) wear-critical alloys and component lead times, (2) evolving emissions compliance costs, and (3) vendor concentration across key manufacturing geographies. High‑chrome alloy consumption patterns and price volatility materially affect operating expenditure in abrasive environments; our report integrates wear-life, replacement frequency, and per‑cycle cost to produce reliable TCO comparatives. Concurrently, emission regulations and water discharge standards can convert equipment specifiers into de facto compliance officers — a procurement behaviour shift that favors OEMs offering certified, monitored systems.

What PW Consulting’s full report provides (practical content)

Our Dewatering Pump Market study is structured to be immediately operational for corporate planning teams. Highlights include:

- Transparent market-sizing and growth model (base year 2025; forecast 2026–2032) with scenario variants and sensitivity tables to test regulatory or commodity shocks.

- Demand-driver analytics by end-use (construction, mining, municipal wastewater, oil & gas, and other niches), with project pipeline overlays and rental-fleet dynamics.

- Vendor scorecards and comparative benchmarking covering product breadth, service footprint, digital capability, and pricing posture.

- Supply chain heatmaps, critical raw-material risk indices, and suggested mitigation levers for procurement leaders.

- Actionable go‑to‑market playbooks for OEMs, equipment rental companies, and EPC contractors — including tender positioning, service monetization models, and channel optimization strategies.

- M&A and partnership screening frameworks tailored to buyer profiles, with worked examples of accretive acquisition candidates and integration risk checklists.

- Excel-based models and downloadable worksheets that allow internal teams to stress-test assumptions against their specific project book.

Note: Detailed segmental splits and vendor-level market shares are intentionally synthesized in the full report to support procurement and M&A decision-making; key segment data are not reproduced in this introduction to preserve the report’s role as the authoritative source.

How to use this intelligence in 2026

- Procurement: Use the report’s TCO matrices to shift tender evaluation from CAPEX-focused scoring to lifecycle cost and regulatory compliance metrics.

- Product strategy: Prioritize electrified and digitally-enabled platforms for projects exposed to emissions or discharge regulation risk; accelerate alloy upgrades within slurry lines where life‑cycle economics justify premiums.

- Service transformation: Build or buy expert field-service networks to capture higher aftermarket margins and lock-in fleet operators through multi-year service contracts.

- Investment & M&A: Target regional specialists with strong rental-channel relationships or OEMs with proprietary wear‑material capabilities that shorten payback horizons.

Conclusion — the strategic imperative for 2026

The dewatering pump market in 2026 offers growth, but it is a growth defined by selective winners. A 6.4% CAGR through 2032 creates attractive opportunities for firms that align product portfolios with regulatory trajectories, invest in service and digital differentiation, and manage raw-material and supply-chain risk proactively. PW Consulting’s full study translates these macro signals into executable strategies — from procurement scorecards to M&A screens — enabling executives to convert market momentum into durable advantage.

For procurement teams, product managers, and investment committees preparing 2026 budgets, this report provides the empirical foundation and the field-tested playbooks to make high‑confidence decisions. Access to the full report will unlock the detailed segment analytics, regional heat maps, and vendor-level models essential for execution — and PW Consulting stands ready to support bespoke scenario runs or strategy workshops tailored to your business priorities.

For detailed analysis of this topic, please visit the official page:Dewatering Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com