Can Precision Analysis Expand the Infrared Spectroscopy Market?

Networking |

2026-07-03 07:11:55

As companies set strategy for 2026, the powder metallurgy (PM) industry is no longer a niche materials play — it is a competitive theater where materials science, manufacturing scale, and supply-chain geopolitics intersect. PW Consulting’s latest Powder Metallurgy Market study, benchmarked to base year 2025, synthesizes market history (2020–2025) with a robust forecast (2026–2032). The market expanded from roughly USD 5.6 Billion in 2020 to USD 9.08 Billion in 2025 and is projected to compound at about 12.8% annually, reaching an estimated USD 21.25 Billion by 2032. For executives making 2026 investment, sourcing, or M&A decisions, the implications are immediate: growth is strong, but strategically complex.

Powder Metallurgy Market

Actionable foresight under uncertainty — Our analysis translates a high-growth trajectory into practical choices: where to invest capacity, which product-to-market paths offer differentiated margins, and how to prioritize technology adoption to avoid costly strategic missteps.

Powder Metallurgy Market

Risk-aware growth playbook — Rapid expansion and adoption of additive manufacturing are creating new demand pathways while exposing companies to raw-material volatility, trade-policy shifts, and evolving standards. The study maps these risks to financial and operational levers that management teams can deploy.

Powder Metallurgy Market

Competitive positioning intelligence — With moderate market concentration (the top three firms account for approximately half of the market, and the top five around six-tenths), the industry rewards scale and specialization differently in each sub-segment. Our report dissects which capabilities yield defensive moats versus which invite fast-follow competition.

Transparent topline models: historical market sizing and an integrated forecast model (2026–2032) that links demand drivers to revenue scenarios. These models are designed for CFO and corporate development teams to run sensitivities on price, volume, and raw material inputs.

Scenario planning and stress tests: three forward-looking scenarios (accelerated adoption, policy-constrained, and stagflationary) with P&L and capex implications tailored to PM value chains.

Supply-chain & sourcing heatmaps: supplier dependency matrices, single-sourced node identification, and contingency playbooks for tariff- or embargo-driven disruptions.

Technology and product roadmaps: comparative ROI for investments into metal powders optimized for additive manufacturing (AM), metal injection molding (MIM), and sintered components, plus timelines for expected adoption and throughput break-even.

Commercial and go-to-market playbooks: pricing architecture, channel and OEM engagement templates, and near-term contract negotiating levers for suppliers and buyers.

Competitive benchmarking: an anonymized capability matrix and strategic actions mapped to four archetypes — global scale players, regional champions, specialty-material innovators, and contract-component specialists.

M&A and partnership frameworks: valuation ranges under different growth assumptions, integration checklists, and a prioritized list of target profiles (bolt-on capacity, technology accretors, and geographic entry pieces).

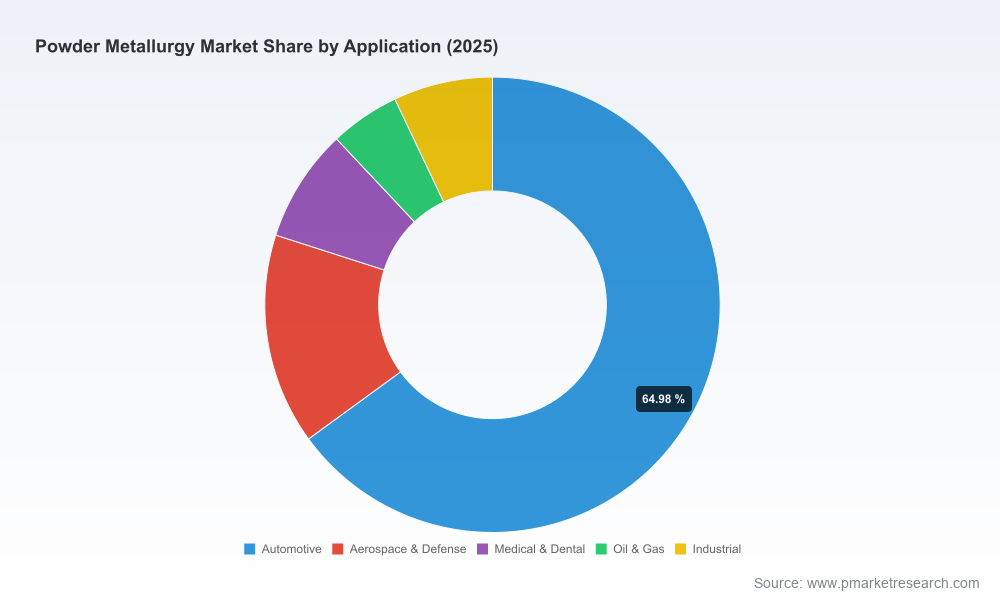

Demand transformation — Automotive electrification and broader drivetrain redesign, coupled with continued AM adoption in aerospace, medical, and industrial applications, are shifting demand from traditional sintered ferrous parts toward high-value powders and complex geometries. While ferrous powders remain central to many applications, the premium segments (high-performance alloys, refractory powders, titanium) are where margin expansion will be realized.

Supply-side consolidation and specialization — The industry exhibits a mixed structure: incumbent global powder producers with integrated downstream assets coexist with agile specialists who command technical niches. This dynamic means incumbents can defend volume economies while specialists can be attractive partners or acquisition targets for technology acceleration.

Raw material and cost volatility — Feedstock price swings and shipping/logistics disruptions materially affect margin profiles, especially for powder producers with thin contract hedging. Management teams must explicitly embed raw-material sensitivities into product-pricing and contract terms.

Regulatory & geopolitical tailwinds — Trade policy and defense sourcing rules are already altering procurement strategies for critical powders (notably refractory metals). Standards (e.g., ISO particle-size methodologies) and public procurement clauses can create both compliance costs and protective barriers to entry for new suppliers.

Technology convergence — Additive manufacturing and powder metallurgy are increasingly intertwined. Investments into AM-capable powders and reproducible batch quality processes will determine which suppliers capture higher-margin, specification-driven demand.

The competitive field comprises several global leaders, regional titans, and nimble specialists. Each profile below highlights the strategic role these firms play in the ecosystem and what that implies for potential partners, suppliers, and buyers.

Höganäs AB — A global leader with deep capabilities in iron and alloy powders. Its scale and technical breadth make it a bellwether for pricing and innovation cycles; competitors should anticipate aggressive capability investments from such incumbents and prepare defensive or collaborative responses accordingly.

Sandvik AB — A diversified supplier with strong presence across PM and AM powders. Recent portfolio moves among large diversified suppliers signal a tightening of focus on high-margin AM/MIM niches.

GKN Powder Metallurgy — An integrated producer of powders and sintered components, offering a model of vertical capture that can be difficult for pure-play powder manufacturers to counter without strategic alliances or M&A.

Regional champions (e.g., major Asian and Russian producers) — These firms provide critical capacity and cost-competitive sourcing options. For buyers focused on resilience, blended sourcing strategies that incorporate regional champions can lower delivered cost risk while preserving technical flexibility.

Specialty innovators (e.g., titanium and low-carbon powder providers) — Firms advancing low-emission processes or novel powder chemistries represent asymmetric opportunities: they can command premium pricing or become acquisition targets for scaling partners.

Contract-component specialists — Producers focused on precision sintering and component assembly retain strong OEM relationships. For integrated players, securing downstream contracts is a viable route to stabilize demand for produced powders.

Portfolio reconfiguration and consolidation — Strategic transactions and carve-outs among established suppliers indicate a period of reallocation of assets toward higher-growth AM and MIM segments. These moves create windows for acquisitive players to capture capabilities at scale.

Capacity investments in key geographies — New facilities and commissioning of high-capacity equipment point to producers preparing for sustained demand; however, timing and ramp risk must be evaluated against forecast adoption curves and local policy incentives.

Policy and procurement effects — Tariffs and defense contract language have materially influenced sourcing of refractory and strategic powders; organizations reliant on such materials must now integrate policy scenario analysis into procurement and supplier scorecards.

Decide your ambition: Are you pursuing scale, specialization, or integration? Each demands a different capex and commercial approach; our report maps expected returns and break-even horizons for these paths.

Hedge supply risk: Establish dual sourcing for critical feedstocks, create contractual pass-through mechanisms for raw-material swings, and evaluate strategic inventory buffering at key nodes.

Prioritize technology bets: Allocate a portion of R&D and M&A budget to powders that enable differentiated AM capability or lower-carbon production — these will command price premiums and regulatory favor.

Use M&A selectively: Target bolt-on capacity that fills geographic or process gaps, and consider acquiring specialty powder innovators for intellectual-property ownership rather than licensing exposure.

Embed compliance and standards: Adopt ISO-compliant particle-size and quality verification processes proactively to reduce onboarding friction with major OEMs and regulated buyers.

Beyond narrative and high-level scenarios, the report provides the practical tools executives need to operationalize strategy in 2026: downloadable financial models, supplier heatmaps, an M&A due-diligence checklist tailored to powder metallurgy, and go-to-market playbooks for selling into automotive OEMs, aerospace primes, and industrial buyers. We intentionally withhold fine-grained segment tables in this executive summary to protect proprietary market intelligence. Full datasets, anonymized supplier benchmarks, and editable scenario models are available on the report landing page for licensed clients.

Decision windows in 2026 will close quickly for firms that want to secure scale or proprietary position in higher-value PM segments. The market’s high compound growth is real, but so are the structural choices: invest to capture premium AM and specialty powder demand, shore up supply-chain resilience, or pursue targeted acquisitions to fast-track capabilities. PW Consulting’s Powder Metallurgy Market study equips leaders with the market topology, financial levers, and risk-mitigation templates needed to convert growth into durable competitive advantage.

For access to the full dataset, scenario models, and bespoke advisory engagements, please visit PW Consulting’s Powder Metallurgy Market page or contact our industry team to schedule a briefings and download the licensed deliverables.

For detailed analysis of this topic, please visit the official page:Powder Metallurgy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com