Reliable Vehicle Shifting in India with Carbikemovers – Safe, Secure & Hassle-Free Car Transportation

Other |

2026-07-06 10:36:58

As health systems, industrial purchasers, and protective-equipment manufacturers plan capital allocation and commercial strategy for 2026, understanding the N95-grade medical protective masks market is now a table-stakes capability. This briefing previews PW Consulting’s full market study, delivering high-level, data-driven perspective and actionable strategic implications — while intentionally withholding the granular segment tables and regional breakdowns that are available in the full report.

N95 Grade Medical Protective Masks Market

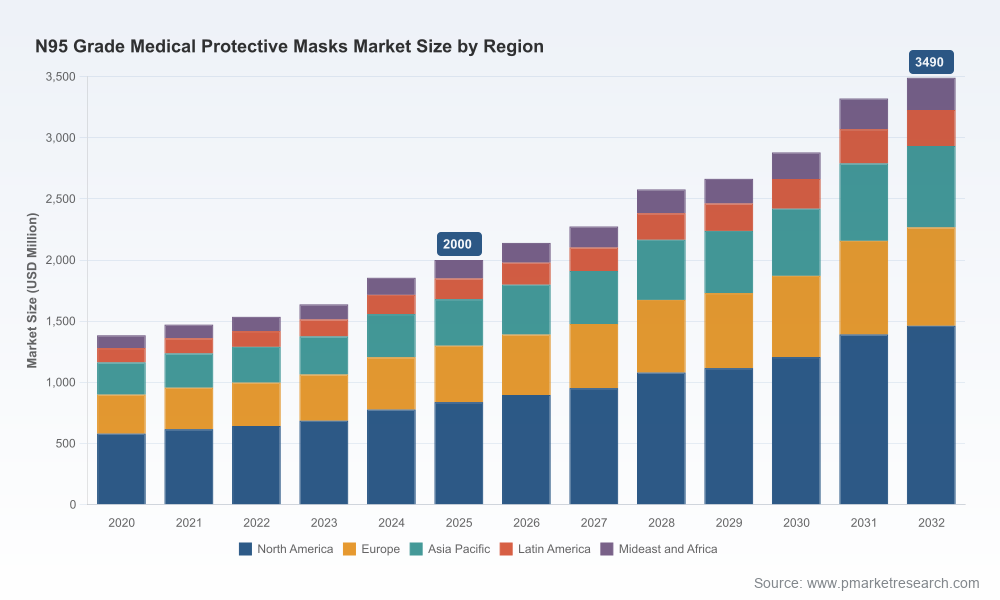

The N95-grade medical mask market has evolved from a pandemic-era anomaly into a structurally important product class for healthcare preparedness, certain industrial segments, and informed consumer demand. From a macro perspective, the market has demonstrated robust expansion across the historical period (2020–2025), reaching a $2.0 billion revenue base in our 2025 reference year. Looking forward, PW Consulting’s model projects continued growth through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of approximately 8.7%.

N95 Grade Medical Protective Masks Market

For leaders making 2026 decisions — whether procurement officers, corporate strategists, CFOs evaluating manufacturing investments, or private-equity sponsors assessing consolidation opportunities — several strategic realities are clear:

N95 Grade Medical Protective Masks Market

PW Consulting’s topline model captures the sector’s transition from emergency-driven production to a market exhibiting steady expansion. The $2.0 billion 2025 baseline reflects the aggregation of medical-grade and surgical N95 units across end users. Under our central scenario, the market expands modestly in 2026 and accelerates through the latter part of the decade as healthcare procurement policies, stockpiling strategies, and industrial respiratory programs institutionalize higher minimum inventory levels.

Interpreting the 8.7% CAGR: this rate implies sustained capital deployment across the value chain (filter media producers, converters, assembly), and it signals opportunities for differentiated producers — particularly those who can combine certified product portfolios with supply-chain resilience and cost discipline.

Three regulatory and standards realities will shape strategy in 2026:

Notably, the CDC-NIOSH certified equipment listing was updated in June 2026, underscoring that several established NIOSH-approved models remain in active production and certification — an important datapoint for compliance-conscious buyers evaluating supplier lists.

Material inputs — particularly electrostatically charged filter media — are the single largest determinant of product performance and perceived value. Industry data indicate that electrostatic media can halve breathing resistance for a given filtration efficacy while preserving required medical fluid-resistance performance thresholds. That technical advantage supports premium positioning, improves wearer compliance in clinical settings, and is a defensible basis for price differentiation.

From a manufacturing perspective, economies of scale in meltblown and spunbond production, as well as investments in automated assembly and quality assurance, create widening margins for larger-scale producers. Conversely, smaller or newer entrants can compete on private-label partnerships, niche ergonomic features, or faster speed-to-market for institutional tenders.

The market displays moderate concentration: the top three competitors command a meaningful portion of industry revenues while the top five account for a larger share — a structure that creates both competitive pressure and consolidation opportunity. Key players include long-established industrial and healthcare-focused producers with distinct strategic advantages:

For buyers and potential investors, competitive analysis should focus on: product approval breadth, manufacturing redundancy and geographic diversity, net working capital and inventory strategy, private-label capability, and contract-performance history.

PW Consulting recommends the following strategic approaches for different stakeholder groups as they make 2026 decisions:

The full study combines quantitative outputs with practical templates and due-diligence workstreams that buyers and sellers can deploy immediately when negotiating contracts, planning capex, or screening acquisition targets.

This briefing intentionally focuses on strategic interpretation of core market dynamics while omitting the granular regional and application-level splits that many teams require to model procurement or investment payoffs. The full PW Consulting report contains the detailed segmentation matrices, regional forecasts, supplier-level capacity tables, and unit-cost line items that underwrite high-confidence 2026 budgeting and bidding decisions.

If your 2026 decisions depend on: (a) precise regional demand outlooks by application, (b) supplier-specific capacity and approval timelines, or (c) a quantified view of price elasticity tied to raw-material scenarios — the full report delivers those inputs together with executable templates and risk mitigants.

The N95-grade medical mask market in 2026 will be defined by the intersection of durable institutional demand, certification-driven buyer behavior, and supply-chain resilience. Firms that align product portfolios with compliance requirements, secure critical upstream materials, and structure contracts to manage surge risk will capture disproportionate value as the market grows at an approximate 8.7% CAGR through the forecast window. PW Consulting’s full study equips decision-makers with the granular data and tactical tools needed to act with confidence; consider this briefing your strategic map, and the full report your operational compass.

For detailed analysis of this topic, please visit the official page:N95 Grade Medical Protective Masks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com