Why Is Rice Starch Market Expanding Across Food, Cosmetic, and Pharmaceutical Industries?

Networking |

2026-05-28 11:37:19

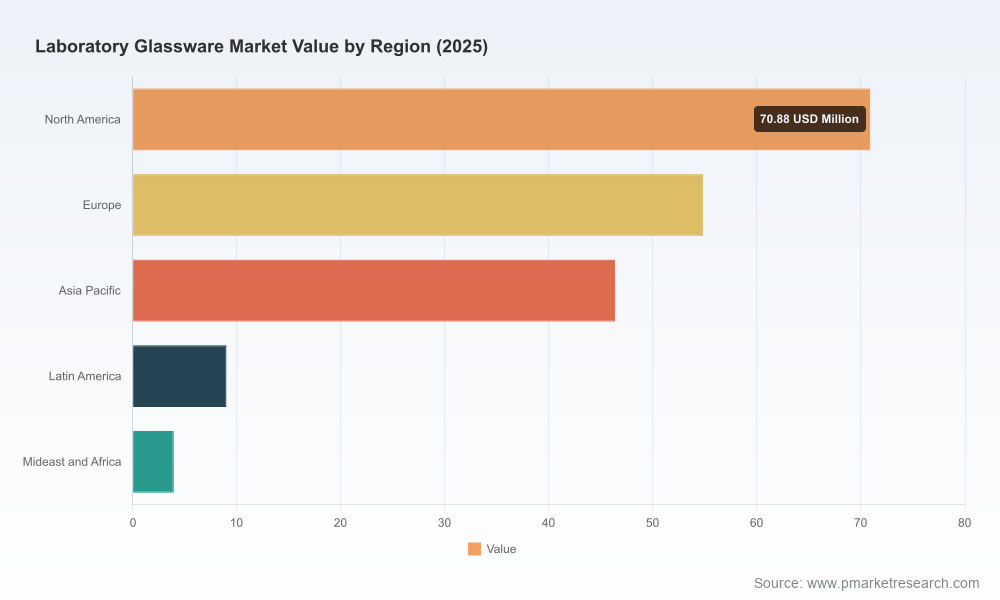

As PW Consulting's Senior Strategic Advisor and Head Industry Analyst, I present a focused, decision-grade introduction to our Laboratory Glassware Market research. The report synthesizes five years of historical performance (2020–2025, base year 2025) and delivers a practicable forecast through 2032 (forecast period 2026–2032). At the market level, the sector has demonstrated steady expansion driven by life‑sciences investment, R&D intensity, and regulated diagnostic throughput — evidenced by an aggregate compound annual growth rate (CAGR) near 4.7% across our forecast. The mid‑decade baseline and modeled scenarios reflect both durable demand drivers and episodic volatility that procurement, manufacturing, and corporate strategy teams must factor into 2026 plans.

Laboratory Glassware Market

Capital allocation: With the market scaling meaningfully from the early 2020s to the 2025 base year and continuing growth projected through 2032, boards and CFOs must balance modest organic growth expectations against targeted investments in product differentiation (e.g., coated bottles, traceable inventory) and supply‑chain resilience.

Laboratory Glassware Market

Procurement and supplier strategy: The industry’s concentration profile (CR3 ~45%, CR5 ~60%) indicates a market where top vendors exert material influence but meaningful fragmentation persists. Buyers should design multipronged sourcing strategies that combine preferred partnerships with niche specialists to mitigate risk and capture innovation.

Laboratory Glassware Market

Regulatory and standards compliance: New international standards for one‑mark volumetric flasks (prEN ISO 1042:2026 and related DIN texts) change baseline compliance obligations. Firms that move early to certify and redesign where necessary will avoid disruption and gain negotiating leverage in regulated markets.

Service and aftercare as a growth lever: As glassware commoditization competes with higher‑margin, differentiated offerings, aftermarket services (traceability, batch documentation, calibration and replacement programs) will be a primary battleground for margin expansion.

Our analysis shows the laboratory glassware market is fundamentally demand‑driven by pharmaceutical, biotechnology, and institutional research spending, while diagnostic volumes and educational procurement provide stable baselines. The primary material — borosilicate glass — continues to dictate manufacturing footprints because of its thermal and chemical performance. Meanwhile, regulation and certification regimes are tightening, notably in volumetrics standards and national conformity frameworks, increasing both compliance costs and barriers to entry.

From a macro perspective, the market progressed from a solid early‑2020s base into a stronger 2025 position and is projected to continue upward through 2032 under our central scenario. That trajectory masks short‑term oscillations and region‑specific demand cycles that create tactical buying and production windows for agile players.

We profiled a representative cross‑section of global and regional players to map capability clusters and strategic options:

Premium global brands (e.g., DWK Life Sciences): These vendors lead on brand recognition, proprietary coatings and safety technologies, and broad distribution. They are well positioned to monetize premium features (shatter protection, certified traceability) but face challenges in low‑cost markets unless they adopt hybrid commercial models.

Specialist and custom manufacturers (e.g., Ace Glass Inc., Bellco Glass): Firms focused on bespoke glass systems and integrated lab equipment can capture higher margins through engineering services and system integration, but they must scale digital order management and after‑sales support to be competitive.

Large regional suppliers (notably several Indian and Chinese manufacturers): These firms compete on lead times, local certification (including national standards like BIS where applicable), and price. They are increasingly adding value through catalog expansion, QR‑based traceability, and modular product lines to serve education and routine laboratory segments.

Mid‑market and niche innovators: Smaller players that focus on traceability, coatings, or specialty cuvettes can become acquisition targets or preferred suppliers for sophisticated research labs seeking integrated compliance and data capture.

Recent industry activity supports these dynamics: leading players showcased innovations at trade shows in 2026, product launches in 2025 emphasized safer, coated containers, and some manufacturers have upgraded catalogues with QR coding for traceability. These moves underscore a visible shift: product quality and data enablement are converging as competitive differentiators.

Supply‑chain resilience and raw‑material strategy: Given borosilicate’s primacy, firms should conduct immediate supplier risk assessments, secure alternative sourcing or strategic buffer inventories, and evaluate nearshoring production for critical SKUs where lead‑time sensitivity is high.

Standards and regulatory roadmap: Allocate budget and project resources to meet the new volumetric standards and national certifications. Compliance is not merely defensive — early certification reduces time‑to‑market for institutional buyers and can be packaged as a commercial offering.

Product and service innovation: Invest in traceability (QR, RFID), safety coatings, and calibrated services. These features convert transactional purchases into recurring service relationships and justify premium pricing.

Channel and commercial model redesign: For global vendors, adopt a two‑speed distribution approach — direct partnerships for large institutional customers and localized distributor networks for volume, low‑margin segments. For regional players, pursue certification and catalog digitization to win institutional tenders.

M&A and partnership playbook: Use the market’s mid‑level concentration as a signal: acquisitions of niche specialists (traceability, coatings, specialty glass) can rapidly bolster capabilities and create defensible differentiation. Conversely, large buyers should pro‑actively form strategic supply alliances to lock in capacity and price stability.

Our full study is designed for immediate operationalization by commercial leaders, procurement teams, R&D heads, and corporate development officers. Key deliverables include:

Procurement leaders: Implement a two‑tier supplier segmentation (strategic vs. tactical) and initiate contract talks with at least two strategic suppliers identified in the scorecards to secure 12–18 month capacity.

Product and R&D teams: Prioritize two product enhancements — a certified volumetric SKU aligned to new standards, and a QR‑enabled traceability pilot with top institutional buyers.

Commercial teams: Redesign bid templates to capture service revenues (warranties, calibration) and pilots that demonstrate lower total cost of ownership to large laboratory accounts.

The laboratory glassware sector in 2026 is neither a high‑growth disruptor nor a pure commodity; it is a market where incremental technical innovation, robust compliance, and superior commercial execution unlock disproportionate returns. The path to durable advantage runs through selective investment in product and service features, disciplined supplier strategies that reflect the market’s concentration dynamics, and rapid compliance to evolving standards. Our report equips decision‑makers with the analytical foundation and step‑by‑step playbooks to convert market trajectory into 2026 performance gains.

This introduction is intentionally selective — it demonstrates analytic depth and priority recommendations while reserving full segment tables, regional breakdowns, and detailed vendor benchmarking for the complete report. Access to the full dataset, model workbooks, and supplier scorecards will enable execution teams to convert strategy into measurable outcomes. Contact PW Consulting to obtain the complete Laboratory Glassware Market report and the accompanying operational toolkits.

For detailed analysis of this topic, please visit the official page:Laboratory Glassware Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com