How does Allurion Gastric Balloon Clinic enable powerful slimming results?

Health |

2026-05-08 09:48:09

As semiconductor and power-electronics architectures compress and electrification accelerates across consumer, automotive and industrial end-markets, polymer capacitors have become a strategic component class. Our PW Consulting market study — based on a 2025 base year, five-year historical tracking (2020–2025) and a 2026–2032 forecast horizon — shows a clear, sustained growth path: the polymer capacitor market expands at a compound annual growth rate (CAGR) of 8.2% through the forecast window. The market’s trajectory, from the mid‑hundreds of millions in 2025 to a high‑hundreds by 2032, creates distinct inflection points for procurement, product planning, qualification programs and M&A activity.

Polymer Capacitor Market

Timing convergence: 2026 is the first full year when a new wave of low-profile, high‑ripple polymer products and hybrid architectures become widely available at scale — forcing OEMs to reassess BOM choices, cooling strategies and supplier qualification roadmaps.

Polymer Capacitor Market

Risk management: Material-cost volatility and supplier lead times are materially higher than pre‑pandemic norms; treating passive components as strategic — not commoditized — items is now mandatory for resilient supply chains.

Polymer Capacitor Market

Regulatory inflection: Strengthened automotive and industrial reliability benchmarks (e.g., AEC‑Q200 expectations and elevated moisture‑resistance testing) are changing qualification calendars and supplier selection criteria.

Between 2020 and 2025 the market showed steady expansion as polymer technologies displaced older wet‑electrolyte designs in higher‑reliability and high‑efficiency applications. With a 2025 base supported by concrete adoption curves, our forecast to 2032 assumes an 8.2% CAGR driven by sustained electronics electrification, higher-density power conversion, and targeted automotive electrification programs.

Translating that growth into action: buyers should expect rising absolute demand that will intensify competition for qualified, automotive‑grade polymer parts; suppliers will face pressure to invest in capacity and qualification throughput; and strategic buyers will need to lock in multi‑year capacities or secure design wins earlier in product cycles to avoid lead‑time and price shocks.

Lead time pressure: Across capacitor technologies, average lead times approached almost five months (circa 19 weeks) as of late 2025. Procurement teams must now bake multi‑tier buffers into launch schedules and maintain dual‑source qualification plans where feasible.

Price dynamics and material inputs: Material cost pressures—particularly in tantalum and certain conductive polymers—prompted supplier price increases in mid‑2024 and continue to influence contract terms into 2026. Scenario planning in the report models several pricing paths and their P&L impacts on mid‑volume platforms.

Regulatory and test regimes: Automotive qualification via AEC‑Q200 remains a gating criterion for EV powertrain and ADAS applications. In parallel, new moisture‑resistance protocols (85°C/85% RH for 1,000 hours) are emerging as a benchmark for industrial‑grade polymers — extending qualification lead times and raising the bar on supplier test documentation.

Technology migrations: The market mix is shifting toward conductive polymer solids and hybrid polymer architectures that offer lower ESR, higher ripple tolerance and better thermal stability — enabling thinner power rails and smaller magnetics but requiring re‑evaluation of thermal and reliability tradeoffs.

The polymer capacitor competitive map is best described as fragmented at scale. Market concentration ratios indicate that the top three players control roughly a quarter of market revenue, with the top five expanding that modestly — confirming that regional specialists, legacy aluminum players and a mix of system‑oriented suppliers remain influential.

Our company coverage profiles include established multinational capacitor manufacturers and focused regional producers. Each of the leading firms brings a distinctive go‑to‑market posture:

Kyocera AVX: Offers a broad range of conductive polymer solid electrolytics, including automotive TCO/TCQ series and hermetically sealed, high‑reliability lines — positioning it for EV and aerospace applications.

Panasonic Industry: Leverages a portfolio spanning conductive polymer aluminum and tantalum solid capacitors, with recent launches of ultra‑low profile POSCAP variants tailored for USB PD and compact power modules.

Murata, Nippon Chemi‑Con, Nichicon and Rubycon: Each advances differentiated product families for automotive, industrial and consumer use cases, with strengthening capabilities around high‑temperature and immersion‑cooling formats.

Vishay, Wurth Elektronik, ROHM and quality-focused regional players: Serve industrial and aerospace niches while competing on reliability documentation, logistics and custom packaging solutions.

Recent product moves validate the strategic pivot to automotive and high‑density power: multiple firms announced automotive‑rated, low‑profile and high‑temperature polymer launches in 2025, underscoring a competitive rush to capture ADAS and EV power‑stage content.

Supplier scorecards: A templated evaluation matrix that weights AEC‑Q200 credentials, moisture‑resistance testing, cycle‑time, regional capacity and demonstrated automotive program experience — ready to drop into procurement RFx processes.

BOM sensitivity models: Interactive scenarios that quantify how tantalum and other material price moves propagate to unit costs and margins under multiple sourcing strategies.

Qualification roadmap templates: Accelerated test plans that reconcile OEM launch calendars with the new 85°C/85% RH endurance expectations and AEC‑Q200 gating checkpoints — reducing calendar risk by up to six months when applied rigorously.

Capacity and lead‑time playbook: Tactical interventions (safety‑stock rules, consigned inventory triggers, capacity‑lease clauses) that procurement and operations teams can implement to blunt 19‑week lead‑time effects.

M&A and partnership screening: A structured filter for inorganic growth that prioritizes bolt‑on technologies (e.g., immersion‑cooling compatible designs), regional certifications and IP‑protected high‑reliability portfolios.

We detail three plausible scenarios in the report — conservative, base, and accelerated adoption — each tied to different assumptions about EV scale, consumer‑electronics power density, and material cost trends. Under all scenarios the key strategic imperatives converge:

Move from single‑source dependency to at least two qualified suppliers for any program with automotive or industrial requirements.

Prioritize supplier certifications and documented life‑test data over short‑term price gains when the target application carries long‑tail reliability risk.

Embed polymer selection early in power‑stage design to capture PCB area and thermal synergies rather than retrofitting modules late in development.

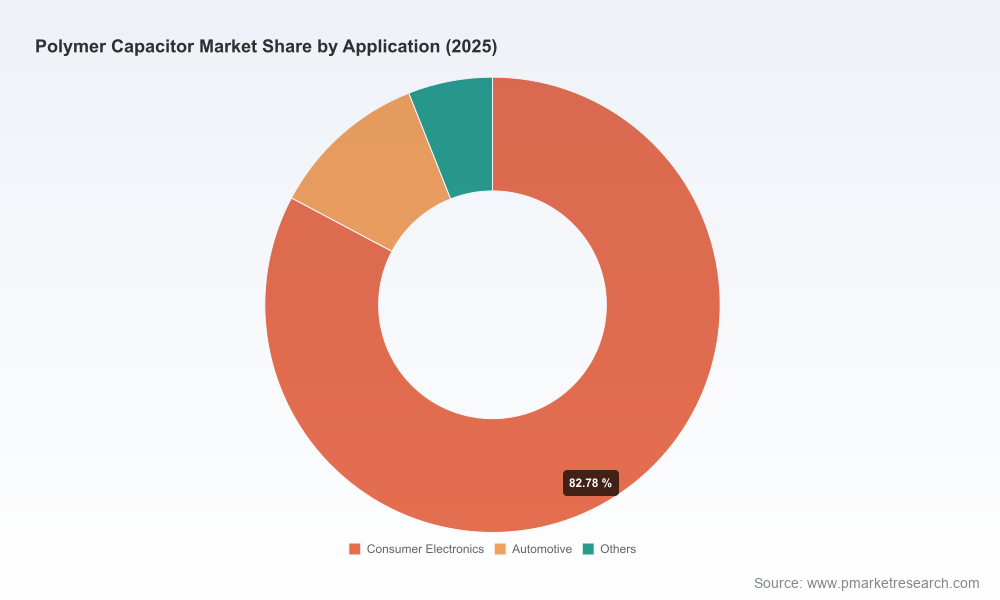

Full market sizing (historical 2020–2025 and forecasts through 2032) with demand‑side drivers and addressable TAM by major application buckets (note: detailed subsegment tables and supplier share matrices are included in the full report).

Operational playbooks: qualification checklists, BOM stress tests, supply continuity clauses and tactical negotiating language for price‑increase events tied to material indices.

Supplier dossiers on the major manufacturers, with capability maps, recent product launches, HQ locations and links to product pages to accelerate due diligence.

Regulatory and testing annex: AEC‑Q200 pathways, moisture‑resistance protocol interpretation and suggested lab partners for accelerated testing.

Financial implications: scenario P&L sensitivity, capex sizing for captive polymer capacitor capacity, and an M&A heat map for strategic buyers.

Cross‑functional briefing: Use the report’s qualification roadmap and supplier scorecards to align engineering, procurement and program management before Q2 2026 RFQs.

Cost‑to‑serve recalibration: Leverage BOM sensitivity outputs to decide where to absorb short‑term price rises and where to pass through costs to customers or redesign to lower‑cost alternatives.

Strategic sourcing sprint: Run a focused 12‑week supplier qualification sprint for any product family slated for production in H2 2027, using our templated test plan and supply‑continuity clauses.

This article offers an operationally focused preview: it outlines market scale, growth dynamics and the practical levers procurement and engineering teams must pull in 2026. To preserve the commercial edge that detailed subsegment metrics and supplier share tables confer, we’ve intentionally withheld the granular segmentation tables and exact supplier revenue splits from this primer. The full PW Consulting Polymer Capacitor Market report (base year 2025; historical 2020–2025; forecast 2026–2032) contains those datasets, alongside downloadable templates and supplier dossiers to operationalize the strategies summarized here.

If your 2026 planning cycle includes new power‑stage architectures, automotive electrification programs, or industrial reliability upgrades, schedule a briefing with our sector team. We will walk you through the full dataset, apply scenario models to your specific product family, and provide an actionable 90‑day implementation plan calibrated to your supply‑chain footprint and risk tolerance.

For detailed analysis of this topic, please visit the official page:Polymer Capacitor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com