Gate Bipolar Transistors STATCOM Market — Strategic Preview for 2026 Decision‑Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a condensed, decision‑focused preview of our Gate Bipolar Transistors (GBT) STATCOM Market study. This preview is designed to demonstrate the depth and practical utility of the underlying research while preserving the proprietary, segment‑level intelligence that drives tactical and transactional action. The full dataset and vendor scorecards are available on the source page; the text below explains why that work will be material to boardrooms, procurement teams, and product leaders throughout 2026.

Gate Bipolar Transistors STATCOM Market

Macro snapshot you can rely on

Our market modelling — using 2025 as the base year (historical window 2020–2025; forecast 2026–2032) — shows a structurally growing market. Total industry revenues expanded from approximately USD 163 million in 2020 to about USD 215 million in 2025, and our central forecast points to a continuation of that trajectory to roughly USD 345 million by 2032. That pathway implies a compound annual growth rate (CAGR) of ~6.98% across the forecast period. These topline dynamics frame every strategic option: vendor selection, R&D prioritization, procurement timing and capital planning.

Gate Bipolar Transistors STATCOM Market

Why this research matters to executives in 2026

- Procurement optimization: The report translates market growth and vendor capabilities into tender strategies and timing windows that materially reduce TCO for large STATCOM procurements.

- Technology selection: It isolates when GBT‑based STATCOM architectures (notably 3.3 kV Si‑IGBT topologies) are the most defensible choice versus alternatives, based on overload performance, lifecycle costs and regulatory compliance.

- Risk mitigation: A supply‑chain heatmap and supplier risk scoring let you pre‑empt single‑source exposure during a period of accelerating grid modernization spend.

- Commercial playbooks: For OEMs and integrators, the report provides GTM frameworks and partner‑selection criteria tuned to regional procurement rules and TSO tender dynamics.

- M&A and JV screening: We identify capability clusters and target profiles likely to yield accretive combinations in a fragmented market.

What the full study delivers (practical, executable content)

- Methodology and assumptions: Transparent definitions (base year 2025), data sources and sensitivity checks for scenario‑based forecasts across 2026–2032.

- Topline market evolution: Annualized market sizing from 2020 through 2032, with scenario bands and drivers that explain the 6.98% CAGR.

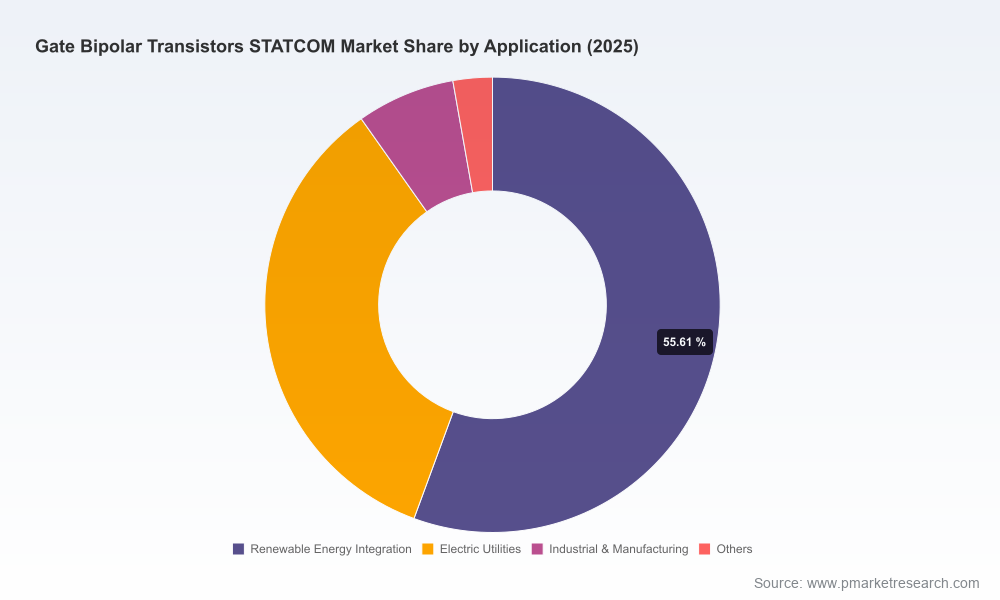

- Segment‑level analytics: Regional and application segmentation, demand drivers, deployment archetypes and growth pockets (note: segmented numerical tables are reserved for the full report).

- Technology decision toolkits: Comparative matrices for Si‑IGBT GBT designs versus SiC MOSFET alternatives, including thermal, overload and harmonics tradeoffs.

- Regulatory and standards matrix: Actionable compliance checklists tied to the evolving standard environment and procurement mandates.

- Vendor scorecards and shortlists: Capability assessments, delivery footprints, warranty and service comparatives, and partnership suitability filters.

- Procurement playbooks: Tender response templates, bid‑evaluation rubrics, capex/OPEX modelling spreadsheets and contracting options that protect against performance risk.

- Case studies and deployment blueprints: Sample specifications, commissioning checklists and O&M best practices derived from recent grid integrations.

Key market dynamics and technology drivers

Three structural forces are shaping GBT STATCOM choices in 2026:

Gate Bipolar Transistors STATCOM Market

- Renewable penetration and grid stability demand. Increased deployment of inverter‑based generation requires fast, localized reactive power support; NREL benchmarks indicate STATCOM systems with IGBT architectures must reliably deliver response times in the 1–5 ms window to satisfy modern voltage‑support requirements.

- Regulatory procurement regimes and harmonic control. New procurement frameworks (for example, Germany’s reactive power market tendering initiatives that took effect in the mid‑2020s) are shifting purchase decisions from bespoke bilateral deals to transparent, market‑based tender mechanisms. Simultaneously, harmonic limits governed by IEEE standards (including provisions in IEEE Std 519) are constraining converter designs and filter strategies.

- Design and device tradeoffs. Recent IEEE Power & Energy Society analyses highlight that T‑STATCOM converter structures using 3.3 kV Si‑IGBTs can deliver distinct overload advantages in high‑voltage installations compared with SiC MOSFET alternatives. That advantage, however, must be weighed against efficiency and future upgrade paths where SiC may become preferable.

Competitive landscape — strategic implications

The GBT STATCOM market is characterized by capable global incumbents, regionally strong manufacturers and a fragmented vendor base that leaves room for consolidation. Our concentration analysis shows the market is not highly concentrated; top players do not dominate the space (top‑3 and top‑5 combined shares are modest relative to other power‑systems sectors). That fragmentation creates tactical opportunities for agile entrants and for incumbents to secure share through service differentiation and integrated solutions.

- Siemens Energy (Germany): A global systems integrator with depth in high‑voltage grid projects and TSO tender experience — a natural partner for large utility deployments.

- ABB Ltd (Switzerland): Strengths in digital control platforms and modular converter architectures that simplify lifecycle services and remote operations.

- Rongxin Power Electronic and Sieyuan Electric (China): Cost‑competitive manufacturers with strong domestic footprints and growing export ambitions; important partners or competitors depending on localization policies.

- Hitachi Energy and Mitsubishi Electric (Japan): Engineering‑led incumbents with particular strengths in reliability, high‑voltage engineering and aftermarket services.

- GE Vernova (USA): Positioned to integrate STATCOM solutions with broader energy‑transition offerings; strategic for combined asset bids and hybrid solutions.

- Ingeteam (Spain) and Fuji Electric (Japan): Niche strength in renewable integration and inverter control systems, useful for co‑development in wind and solar‑rich grids.

- American Superconductor (AMSC), Hyosung Heavy Industries, S&C Electric Company (US & Korea): Focused plays on grid stabilization, distribution‑level solutions, and reliability services — attractive for microgrid and distribution operator partnerships.

Regulatory and standards watch‑list (operational guidance)

- Germany’s reactive power market reforms (TSO tenders) create discrete procurement opportunities — align bid teams to calendar windows and compliance checklists (Fraunhofer ISE, 2025).

- IEEE Std 519 developments (2014 baseline and subsequent updates through 2025) reinforce the need for early harmonic modelling and filter design validation in tender responses.

- EU market‑based procurement mandates (Directive 2019/944) mean transparency in pricing and performance guarantees will be evaluated formally in many European tenders.

How to use this work in 2026 — concise actions

- Prioritize pilot procurements now, timed to the 2026 budget cycle, that lock in scalable supplier options and preserve upgrade pathways (e.g., modular converter frames that allow future SiC retrofits).

- Mandate harmonics and response‑time acceptance tests (1–5 ms targets) as contractual deliverables tied to milestone payments; the report supplies recommended test protocols.

- For OEMs: allocate R&D budgets to exploit the operational benefits of 3.3 kV Si‑IGBT designs while preparing a roadmap to SiC where lifecycle economics justify.

- For investors and corporate dev: use the vendor scorecards to create a short‑list for M&A or minority investments that address capability gaps (software controls, installation services, local manufacturing).

- Engage regulators proactively: use the compliant procurement templates in the report to shape tender rules and ensure STATCOM specifications recognize real‑world overload and harmonic behaviour.

Final note — what is intentionally withheld here

This preview purposely omits the granular regional, type and application breakdowns, and it does not reproduce the vendor‑level pricing and project revenue tables included in the full study. Those segmental datasets and the proprietary vendor scorecards are the operational core that procurement, engineering and investment teams will use to execute in 2026. If you require the project‑level datasets, supplier‑response templates, or the full comparative financial models, the full report and accompanying data pack contain them and are accessible from the source page.

Next step

For teams who need an actionable briefing or a 90‑minute executive workshop built around this study (including live walk‑throughs of the procurement playbook and vendor scorecards), PW Consulting can deliver a custom session calibrated to your program timeline. The full report provides the numerical granularity and playbook tools required to move from strategy to contract in 2026.

For detailed analysis of this topic, please visit the official page:Gate Bipolar Transistors STATCOM Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com