Agarose Market 2026: Strategic Imperatives for Decision-Makers — A PW Consulting Perspective

Executive snapshot

The global agarose market has moved from a niche reagent to a strategically important upstream material for both life-science research and bioprocessing. PW Consulting’s latest study shows the market accelerating from a historical base in 2020 to a 2025 market size of USD 215.0 Million (base year 2025), and—under the scenarios modelled—expanding to approximately USD 344.8 Million by 2032. That trajectory reflects a compounded annual growth rate (CAGR) of roughly 6.98% through the forecast window. For leadership teams making 2026 investment, sourcing, and portfolio decisions, these high‑level dynamics translate into tangible strategic choices: where to allocate R&D and CapEx, how to structure supplier relationships, and which competitive moves are most likely to protect margin and market access.

Agarose Market

Why this study matters for 2026 corporate strategy

- Market momentum frames resource allocation: The mid-single-digit-plus CAGR signals sustained, above‑inflation demand across core end‑uses—enough to justify targeted capacity investments but not so high as to eliminate the need for disciplined commercialization and margin management.

- Risk is concentrated upstream: Raw material exposure (seaweed-derived inputs), geopolitics and logistic cost volatility are systemic risks that propagate through price, lead times and quality variability. Companies that act preemptively to diversify suppliers or vertically integrate selective inputs will gain a structural cost/availability advantage.

- Innovation bifurcation opens differentiation paths: One avenue centers on high‑performance agarose resins for bioprocessing (affinity and chromatography beads). The other continues to be routine and convenience formats (precast gels, standardized powders) for molecular labs. Each pathway demands distinct go‑to‑market and operational capabilities.

What PW Consulting’s report delivers (practical, actionable content)

Our full report is designed as a toolkit for commercial, supply‑chain and M&A decision makers, structured around reproducible analyses and executable playbooks. Key components include:

Agarose Market

- Market sizing and trend decomposition — a validated top‑down and bottom‑up view of the market, including historic growth drivers (2020–2025) and scenario-based forecasts (2026–2032).

- Demand segmentation framework — demand drivers and elasticity analysis across product types and end‑use categories, with forward-looking adjustments reflecting automation and throughput trends in molecular labs and bioprocessing.

- Supply‑chain mapping and vulnerability heatmap — an operational breakdown from seaweed sourcing to finished agarose formats, highlighting single‑point failures, freight and tariff exposures, and unit‑cost drivers.

- Competitive benchmarking — positioning of incumbent and emerging players across capability matrices (R&D, manufacturing scale, regulatory footprint, channel strength, and specialty resin know‑how).

- Commercial playbooks — pricing levers, contract structures (consignment vs. framework purchasing), and channel strategies for private‑label vs. branded offerings.

- Regulatory & certification matrix — expected 2026 regulatory touchpoints, compliance trajectories, and country‑level sensitivities that materially affect time to market.

- M&A and partnership screen — target profiles, valuation heuristics, and integration checklists for bolt‑on acquisitions in chromatography resins, raw material suppliers and niche consumables.

- Scenario stress tests — combined supply/demand shocks (e.g., export restrictions, fuel spikes), with contingency roadmaps tailored to different firm archetypes (supplier, OEM, distributor).

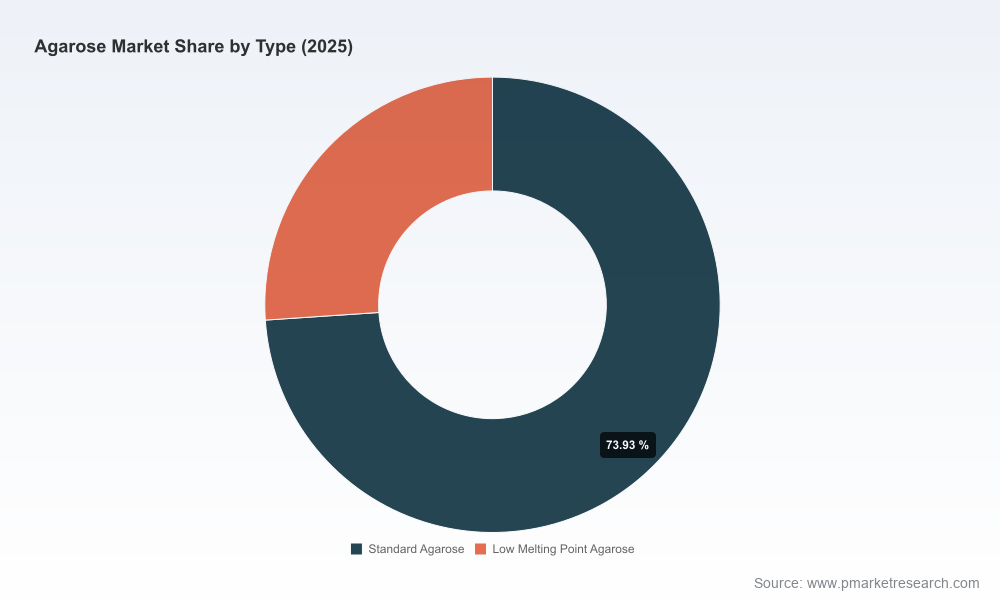

Note: this article intentionally omits granular sub‑segment figures and region/application share data; the full breakouts and transaction‑level tables are available in the report portal.

Agarose Market

Competitive landscape — selective strategic reads

The agarose value chain is populated by a mix of specialized, vertically integrated and diversified players. Market concentration metrics indicate meaningful but not prohibitive leader advantage—enough room for specialists and fast followers to carve sustainable niches.

- Agarose Bead Technologies (ABT) — a Spain‑based specialist focused on high‑performance agarose resins for bioprocessing. Recent capacity expansion and continued trade‑show visibility underscore a growth posture aimed at bespoke resin solutions for biologics purification. Firms evaluating partnerships should treat ABT as a potential supplier or contract‑manufacturing partner for affinity resins.

- Purolite (part of Ecolab) — leveraging patented production technologies, Purolite is advancing high‑precision agarose chromatography resins for MAb purification and downstream bioprocessing. Its product launches demonstrate a play towards higher‑value, volume‑sensitive applications where performance characteristics command premium pricing.

- Lonza — with product offerings tailored for nucleic acid electrophoresis, Lonza occupies a middle ground between research consumables and specialised analytical materials, benefitting from reputation and broad distribution networks.

- Bio‑Rad Laboratories — a well‑established supplier of molecular biology agaroses and consumables; its brand strength in electrophoresis formats continues to confer channel advantages in research and diagnostic labs.

- Thermo Fisher Scientific — scale and systems integration are the company’s differentiators, with UltraPure grades and precast systems that favor customers seeking throughput and standardized workflows.

Strategic takeaway: incumbents with deep channel relationships and manufacturing scale compete on reliability and product breadth; specialists compete on custom performance and faster time‑to‑spec for bioprocess needs.

Dynamics shaping risk and opportunity

- Raw material policy and supply: National initiatives to expand seaweed production (for example, recent European roadmaps) and shifting import/export classifications in major markets are reshaping upstream availability and price volatility. Purchasing and sourcing teams must treat these policy moves as medium‑term supply shocks, calibrating contracts to include flexible volume and indexation clauses.

- Geopolitics and trade costs: Rising freight and tariff pressures since 2024 have already increased landed costs for many producers. For manufacturers, this validates strategies such as regionalized production hubs, freight optimization, and dual‑sourcing models to reduce exposure.

- End‑user evolution: Increased automation in molecular diagnostics, higher throughput in sequencing and expanding biologics pipelines are pushing demand towards higher‑specification agarose grades and resins. Companies able to package product performance with workflow integration (precast gels, consumable systems) capture disproportionate share of wallet.

- Consolidation potential: Market concentration metrics point to clustering at the top but significant mid‑market fragmentation. Expect opportunistic consolidation around specialized resin capabilities and distribution networks through 2026–2028.

Practical strategic recommendations for 2026

- Supply‑chain resilience as capital investment: Secure multi‑year supply agreements with indexation clauses and build spot buffers for critical inputs. Consider near‑sourcing or regional micro‑factories for high‑margin product lines where lead time and duty are material to customer retention.

- Segmented product strategy: Separate routes to market—one focused on premium chromatography resins with technical service and partnership models; the other on standardized consumables sold through distributors and e‑commerce—each with tailored margin and working‑capital profiles.

- R&D prioritization: Invest selectively in performance attributes that matter to upstream bioprocesses (binding capacity, bead uniformity, robustness under CIP) and to downstream lab workflows (ease of use, precast format reliability).

- Commercial levers: Implement value‑based pricing for specialty resins and subscription/consumable models for routine formats. For distributors, offer exclusivity and volume rebates in exchange for inventory commitments to stabilize demand.

- M&A and partnerships: Target bolt‑ons that add technical depth (resin chemistry), channel access (regional distributors), or raw‑material control (seaweed processing facilities). Use earn‑outs tied to integration milestones and supply‑continuity KPIs.

- Regulatory monitoring and advocacy: Actively engage with national seaweed roadmaps and classification discussions in major markets. Early regulatory clarity or co‑investment initiatives can convert policy risk into supply advantage.

How to use PW Consulting’s report in your 2026 planning cycle

- Strategic planning: Use our scenario outputs to stress‑test three capital allocation priorities—capacity expansion, M&A, and product development—across upside and downside demand cases.

- Procurement playbook: Leverage the supplier heatmap to rebalance sourcing and to construct contract terms that limit cost pass‑through exposure.

- Commercial execution: Apply the go‑to‑market frameworks to restructure sales incentives and to pilot value‑based contracts in two priority geographies or customer segments.

- M&A screening: Utilize our target persona profiles and valuation ranges as a shortlist for due diligence and rapid integration planning.

Final note — the limitations of a preview and where to go next

This article is intentionally calibrated as a strategic preview: it highlights the macro trajectory (2020–2025 historic growth and a 2026–2032 outlook driven by a near 7% CAGR) and the forces that will shape winner strategies in 2026. To preserve actionable advantage for our subscribers, detailed sub‑segment tables, regional shares, application breakouts and transaction‑level comparables have been omitted from this summary. Those detailed analytics, scenario models (including sensitivity matrices) and downloadable supply‑chain schematics are available in the full PW Consulting Agarose Market report and companion data pack.

For executives preparing 2026 budgets and roadmaps, PW Consulting can run a concise 2–4 week diagnostic (supply exposure mapping, commercial opportunity sizing, or target screening) that customizes the report’s insights to your asset base and strategic priorities. Contact our industry practice to schedule a briefing and obtain the full dataset.

For detailed analysis of this topic, please visit the official page:Agarose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com