Isoparaffin Solvents Market: Strategic Imperatives for 2026 Decision‑Makers

Executive snapshot

By 2025 the global isoparaffin solvents market had recovered to a renewed growth trajectory, reaching an estimated USD 905.16 Million. PW Consulting’s baseline (2025) view projects the market to expand at a compound annual growth rate (CAGR) of 3.5% across the 2026–2032 forecast horizon, arriving near USD 1.15 Billion by 2032 under our central scenario. Concentration metrics show a moderately fragmented supplier landscape (CR3 ≈ 28.3; CR5 ≈ 32.1), indicating room for consolidation, differentiated premium positioning, and regional plays.

Isoparaffin Solvents Market

Why this briefing matters in 2026

For executives planning capital allocation, sourcing strategies, or go‑to‑market shifts in 2026, the isoparaffin solvent market is at a strategic inflection. Incremental regulatory tightening on volatile organic compounds (VOCs), feedstock volatility, and product differentiation toward low‑odor, low‑aromatic grades are simultaneously compressing margins and creating premium niches. The analysis that follows synthesizes macro trajectory, competitive posture, and practical decision levers that will determine who captures the next layer of value.

Isoparaffin Solvents Market

Market trajectory and what the headline numbers conceal

The headline growth (CAGR 3.5% to 2032) masks divergent forces beneath the surface. A multi‑year recovery from USD ~761 Million in 2020 to USD ~905 Million in 2025 reflects demand resilience across industrial applications and reformulation pushes in coatings and cleaning segments. Looking ahead, demand drivers—regulatory substitution away from aromatics, expansion of industrial activity in select regions, and increasing uptake of higher‑purity grades—support steady expansion. At the same time, feedstock price swings and compliance costs will create episodic margin stress for commodity producers.

Isoparaffin Solvents Market

PW’s scenarios model both a baseline and two directional alternatives: an accelerated regulatory scenario (faster substitution toward high‑purity, low‑VOC grades) and a structural slowdown scenario (higher feedstock costs and slower end‑market growth). Each pathway materially alters unit economics for manufacturers and reshapes competitive advantage—details and model inputs are provided in the full report.

Dynamics shaping demand and supply in 2026

- Regulatory pressure is the proximate catalyst for reformulation: Tightening VOC regimes—especially updated limits in parts of South America and continued enforcement under U.S. EPA and EU directives—are accelerating adoption of high‑purity isoparaffinic grades as compliant replacements for aromatic solvents. This creates premiumization opportunities for suppliers with low‑aromatic, low‑odor product lines.

- Feedstock and margin volatility: Isoparaffins remain sensitive to upstream hydrocarbon feedstock prices and refining economics. Our margin simulations show that modest feedstock shocks materially compress profitability for commodity grade offerings, increasing the strategic appeal of differentiated, specialty grades with value‑added formulation attributes.

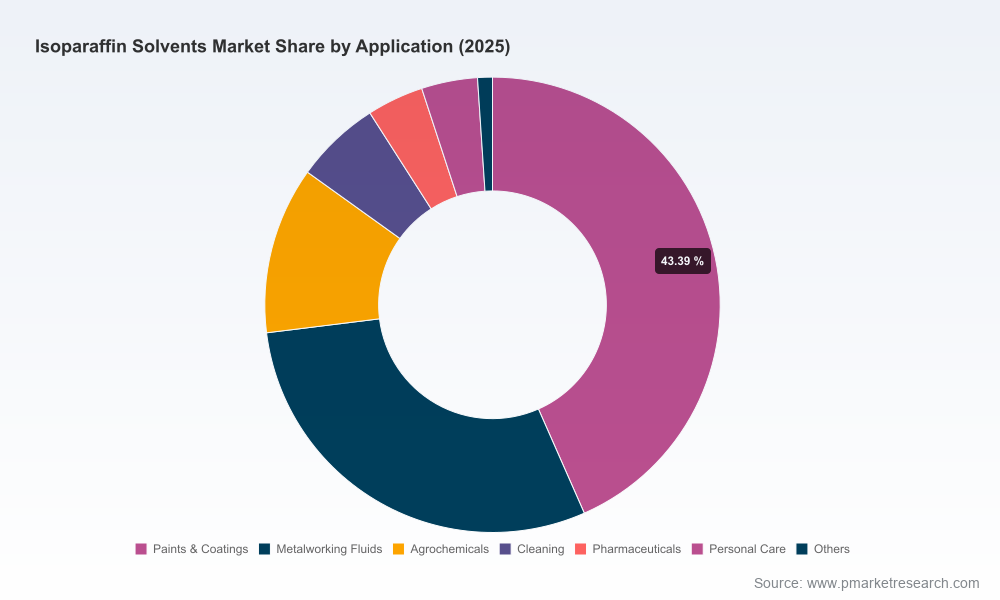

- End‑market formulation shifts: Continuing reformulation in paints & coatings, metalworking fluids, agrochemicals, and several specialty cleaning applications favors grades that balance solvency power with low odor and regulatory compliance. Personal care and pharmaceutical uses, while smaller in volume, are important for margin and branding due to strict purity specs.

- Regional supply reconfiguration: Recent capacity moves and plant investments are changing logistics and feedstock exposure for global players. These shifts affect local availability, lead times, and the cost base for regional customers—making sourcing strategies and dual‑sourcing arrangements critical in 2026.

Competitive landscape — strategic positioning of core players

The market is populated by global majors and regional specialists. Leading producers combine broad distribution, strong technical support, and branded high‑purity portfolios that command premiums; smaller players compete on price, niche grade supply, or proximity to local end‑markets. Recent industry developments illustrate these dynamics:

- Shell plc (The Hague): Shell’s ShellSol portfolio emphasizes high purity and low odor. Their 2025 plant inauguration in Brazil expanded local production capacity significantly and complements product datasheet updates that position ShellSol for surface‑coatings and regulatory‑sensitive applications. Strategically, these moves reduce regional logistics exposure and strengthen compliance‑focused differentiation.

- Chevron Phillips Chemical Company (The Woodlands): Chevron Phillips has incrementally increased manufacturing capacity, underscoring a bet on continued industrial demand and the value of operational scale. Their Soltrol® grades are positioned as low‑odor, broadly compatible solvents for cleaning and formulation use.

- Exxon Mobil Corporation (Irving): ExxonMobil’s Isopar™ fluids target high‑purity applications, with recent technical updates highlighting low aromatic content. The combination of global distribution and technical support makes ExxonMobil a preferred partner for formulation teams seeking regulatory certainty.

- Regional and specialty producers: Companies such as Braskem, TotalEnergies, INEOS, Idemitsu, Calumet, Sasol and SK Global Chemical maintain strategic footholds—either through integration with broader hydrocarbon portfolios, proximity to key feedstocks, or targeted product lines. Their roles range from local supplier to strategic partner for specific industrial ecosystems.

Recent tactical moves and their strategic signals

- Capacity additions and plant inaugurations in 2025 show incumbents preparing for regionally differentiated demand and regulatory-driven substitution. These investments tighten the link between manufacturing footprint and customer access.

- Product datasheet updates and technical repositioning highlight how manufacturers are monetizing compliance attributes (low‑aromatic, low‑odor) as a pricing lever.

- Incremental capacity increases by major chemical manufacturers suggest continued preference for scale, but CR metrics indicate that true consolidation has been limited—opening opportunities for M&A, JV, or offtake partnerships for scale‑seeking challengers.

What PW Consulting’s full report delivers (operationally usable)

Our full Isoparaffin Solvents Market report blends strategic insight with executable tools for 2026 planning, including:

- Validated historical time series and baseline forecasts (2026–2032) with scenario sensitivity to feedstock prices and regulatory tightening.

- Supply‑chain heat maps linking plant locations, modal logistics, and lead‑time risk by region.

- Competitive benchmarking with capability matrices covering product purity, narrow boiling ranges, technical support, and channel reach.

- Price and margin models that allow CFOs to stress test cost pass‑through under a range of feedstock and regulatory outcomes.

- Regulatory risk matrix and compliance playbooks tailored to the U.S., EU, and South American regimes—actionable for product managers and compliance officers.

- Commercial playbooks: recommended go‑to‑market strategies for premiumization, contract structure templates (volume discounts, indexation to feedstock), and a shortlist of potential JV/M&A targets derived from capability gaps.

- Decision‑ready slides and an executive summary optimized for board discussions and CAPEX approval processes.

Recommended strategic moves for 2026

- Prioritize product‑grade differentiation: Allocate R&D and marketing resources to low‑aromatic, low‑odor grades that meet tightening VOC and solvent emission requirements. These grades justify higher gross margins and deepen customer switching costs.

- Reassess footprint and logistics: Use PW’s supply‑chain heat maps to identify plants where incremental local capacity or toll manufacturing partnerships beat long‑haul logistics—especially in markets with strict VOC controls.

- Hedge feedstock risk: Implement financial and commercial hedges (indexation clauses, strategic inventory, alternative feed sourcing) to stabilize margins during rapid hydrocarbon price swings.

- Commercial contracts as barrier‑to‑entry: Design multi‑year offtake agreements linked to technical support, co‑development, and formulation services to lock in strategic accounts in coatings and metalworking segments.

- M&A and partnership playbook: For mid‑sized players, pursue bolt‑on acquisitions that add technical grades, local capacity, or feedstock integration. For majors, consider minority stakes in regional processors to secure last‑mile access without full greenfield investment.

How PW’s insight reduces 2026 decision risk

In a market where regulation, feedstock dynamics, and end‑market formulations are evolving concurrently, executives face asymmetric information risk. PW’s integrated approach—combining macro forecasts, scenario models, regulatory mapping, and competitor capability matrices—reduces that risk by turning uncertainty into quantified options: where to invest, which grades to prioritize, and how to structure commercial terms to preserve margins.

Next steps — where to get the full intelligence

This article is a strategic preview of PW Consulting’s full Isoparaffin Solvents Market study. The complete report contains the granular segmentation, model inputs, and downloadable scenario workbooks that are essential for executing the 2026 strategies outlined above. PW’s report also includes the complete competitive dossiers and the proprietary cost‑curve analysis that we intentionally exclude from this preview to preserve the report’s actionable value.

For procurement, commercial, and corporate development leaders preparing plans in 2026, engaging with the full PW Consulting study will provide the playbooks and analytic templates necessary to convert the market’s structural shifts into competitive advantage.

For detailed analysis of this topic, please visit the official page:Isoparaffin Solvents Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com