PW Consulting: Trial Process Management System Market Set for Rapid Growth — 13.18% CAGR Forecast for 2026–2032

Other |

2026-07-02 15:38:08

As organizations prepare their 2026 strategic plans, the tax software market demands renewed attention. PW Consulting’s latest market research—anchored in historical performance from 2020–2025 and forecasting to 2032—reveals a durable, technology-driven expansion. The market has grown substantially in recent years and, under a base-case trajectory, is expected to continue expanding at an annualized clip of roughly 9% through the forecast window. This preview outlines the strategic value of our full study for corporate leaders, finance chiefs, product owners, and investors while deliberately leaving detailed subsegment tables and granular splits for the full report.

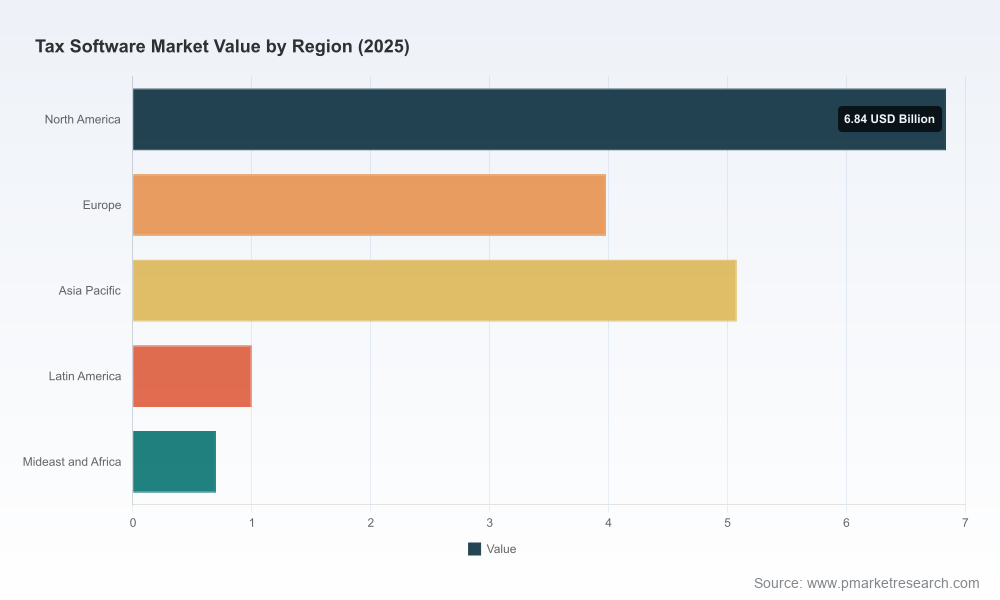

Tax Software Market

Tax technology is no longer a niche back-office cost; it is an operational lever that affects working capital, audit risk, compliance posture, and customer experience. Decisions made in 2026 about platform architecture, vendor partnerships, and implementation timelines will lock in returns (or costs) for multiple years.

Tax Software Market

Regulatory momentum—both in e‑filing standards and franchise tax processing—means vendors and enterprise buyers are operating in a shifting compliance landscape. Early alignment with evolving standards reduces disruption and can create competitive advantage.

Tax Software Market

Market concentration and vendor dynamics favor informed partner selection. Our analysis synthesizes competitive positioning to help buyers distinguish established incumbents from niche specialists and emerging challengers.

Since 2020 the market has experienced sustained expansion, driven by cloud adoption, automation of preparatory workflows, and heightened compliance complexity. The market’s scale increased materially across the five-year historical window and continued momentum into the base year. Using our central scenario, the market is expected to grow at an average annual rate of about 9% across 2026–2032, underscoring long-term investor and buyer interest.

For corporate strategic planners, the implication is clear: tax technology is a growth theme that warrants capital allocation and attention similar to other enterprise SaaS categories. At the same time, predictable growth does not eliminate disruption—advances in API integrations, real-time e‑filing validation, and embedded tax services will reshuffle competitive advantage.

Regulatory and compliance dynamics: The IRS’s requirements for Modernized e‑File (MeF) participation and the Assurance Testing System (ATS) impose precise technical and data standards. Beyond federal rules, state-level mandates—such as approved provider lists for franchise tax filings—create additional technical and validation requirements. Buyers must prioritize vendors with proven MeF/ATS experience and state-level certification roadmaps.

Product architecture shift: Cloud-native platforms now dominate new deployments, offering elastic scaling for seasonality and rapid update capabilities for tax law changes. However, hybrid and on‑premises footprints remain relevant for firms with sensitive legacy processes or strict data residency needs.

Operational economics: Labor and licensing remain central to total cost of ownership. Professional preparers continue to use specialized packages with multi‑user licensing arrangements; our market conversations and benchmarking show recurring annual licensing ranges for professional multi‑user setups in the mid-hundreds to low‑thousands of dollars per seat. That range directly affects the ROI of automation initiatives and influences vendor pricing strategies.

Consumer-facing programs and access: Public-sector initiatives such as IRS-sponsored free guided preparation programs create pricing pressure at the low end of the market, particularly for taxpayers under specific AGI thresholds. Vendors must therefore balance premium service offerings with lower-cost access points to preserve market share.

Vendor readiness and product updates: Major professional vendors continue cadence releases and client education. For example, Wolters Kluwer’s 2026 tax software update webinars highlight how incumbents operationalize law changes into product releases—an important indicator of vendor maturity and customer enablement.

Regulatory approvals as market validators: The IRS list of approved MeF providers and state-level approved provider lists for franchise taxes are practical gatekeepers—membership or approval is a de facto credential that simplifies procurement and integration risk assessment.

Continuous product maintenance among specialist vendors: Smaller but focused players release frequent point updates and tooling improvements to remain competitive on quality and compliance. Observed release activities in 2026 demonstrate that product agility is not confined to the largest incumbents.

The market exhibits a modestly high level of concentration among leading global and regional incumbents. A small group of well‑capitalized platform vendors capture a large share of commercial revenue, while a mix of specialist and vertical providers serve firm-level and regional niches. In other words, it’s a two‑tier dynamic: scale-enabled platforms compete on breadth and integrations, while niche vendors compete on depth and practitioner workflows.

Intuit: A dominant consumer and small-business presence with integrated consumer tax products and a professional line for preparers. Their network effects, brand recognition, and data-driven product enhancements make them a must‑evaluate partner for consumer-facing and SMB strategies.

H&R Block: A strong retail and assisted‑service channel combined with software offerings aimed at individual and small-business filers. Their hybrid service model is instructive for firms considering omnichannel distribution.

Wolters Kluwer and Thomson Reuters: These incumbents focus on CPA and professional workflows with mature suites for corporate, partnership, and complex returns. Their value proposition includes deep tax content, firm-level practice management, and integrated compliance controls.

Regional and specialist vendors (e.g., Drake, TaxAct, TaxSlayer, CFS, Advanced Tax Solutions): These companies remain relevant given their practitioner centricity, competitive pricing, and rapid responses to tax season needs. For some enterprise buyers, these firms are strategic partners for replacing legacy tooling at the practitioner level or for servicing specific filing segments.

Understanding when to partner with a scale provider versus a specialist vendor is one of the core procurement decisions the full report helps operationalize through scenario-based vendor scorecards, integration readiness matrices, and TCO models.

Executive decision frameworks: Procurement checklists and board-level risk summaries aligned to operating models for in‑house, co‑sourced, and fully outsourced tax functions.

Vendor assessment tools: Comparative scorecards emphasizing compliance certifications (MeF/ATS readiness), release cadence, integration APIs, security posture, and total cost of ownership across deployment models.

Implementation playbooks: Staged migration plans for cloud adoption, change-management templates tailored to tax season rhythms, and stepwise validation gates to reduce audit and filing errors.

Scenario-based financial models: ROI calculators that incorporate licensing, labor savings from automation, error-rate reduction, and audit risk mitigation—designed to support capital requests and vendor selection committees.

Regulatory trackers and impact notes: Consolidated view of federal and key state compliance changes (e.g., e‑filing requirements and franchise tax process updates) with recommended vendor and process responses.

Prioritize compliance-first procurement. Confirmation of MeF/ATS readiness and state-approved provider status should be a gating criterion for short‑listing vendors.

Invest in cloud modernization selectively. Use a hybrid roadmap that preserves continuity for mission‑critical legacy processes while accelerating new cloud-native capabilities for scale and faster law-change rollouts.

Embed tax into broader finance digitization programs. Tight integration between tax engines, ERP, and treasury systems reduces reconciliation effort and unlocks real-time cash-flow and tax provision insights.

Run a two-track vendor evaluation. Assess at least one large-scale incumbent and one specialist that demonstrates superior practitioner workflow efficiency. Use pilots that include seasonal peak testing and end-to-end e‑filing verification.

Budget for ongoing maintenance and training. Licensing is only one part of TCO; sustained product updates, staff certifications, and controlled release adoption are ongoing costs that materially affect outcomes.

The findings summarize historical data (2020–2025), a 2025 base year read, and a forecast covering 2026–2032. Our approach combines primary interviews with market participants, vendor financial disclosures, regulatory filings, and product release logs. Where public approvals and regulatory gates exist—such as MeF provider lists and state approved‑provider registries—we incorporate those as objective validation points for vendor claims.

This preview is intentionally strategic and directional. For procurement teams, investors, and product leaders who require the granular subsegment tables, regional and application splits, and the vendor-by-metric benchmarking used to derive our recommendations, the full report contains the complete data appendices, downloadable vendor scorecards, and implementation templates. Accessing the full dataset and proprietary segmentation will enable transaction-grade diligence and implementation planning.

PW Consulting stands ready to support scenario workshops, procurement RFIs, and implementation oversight informed by this research. For teams planning vendor selections or budget submissions in 2026, aligning early with these insights will reduce execution risk and increase capture of upside in a market that continues to expand at an above‑average SaaS growth rate.

For detailed analysis of this topic, please visit the official page:Tax Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com