Bone Cement Market: A Strategic Preview for 2026 Decision-Making

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise but strategically rich preview of our full Bone Cement Market research—designed to orient executive decision-making for 2026. This briefing synthesizes growth trajectory, structural dynamics, competitive posture, and near-term shocks that will materially affect how companies prioritize R&D, supply-chain investments, go‑to‑market tactics, and M&A activity in the year ahead.

Bone Cement Market

Why this study matters for 2026

- Actionable horizon: Our report uses 2025 as a base year, analyses the 2020–2025 historical period, and provides a 2026–2032 forecast horizon to align with near-term investment cycles and regulatory milestones.

- Decision relevance: By quantifying market momentum, concentration, and shock scenarios, the study equips executives to size inventory buffers, model alternative sourcing, and set prioritized product roadmaps before budget cycles close in 2026.

- Risk-to-opportunity framing: We translate supply disruptions, reimbursement shifts, and regulatory clearances into prioritized tactical responses—allowing commercial and operations leaders to move from contingency thinking to value capture.

Market trajectory at a glance

The bone cement market has demonstrated steady expansion through the pandemic recovery and into 2025. In nominal terms, global market revenue rose from approximately USD 986.72 Million in 2020 to USD 1,226.41 Million in 2025. Our base-case forecast projects the market will continue to grow at a compound annual growth rate (CAGR) of roughly 5.8% across the 2026–2032 forecast window, reaching about USD 1,823.54 Million by 2032 under the modeled assumptions.

Bone Cement Market

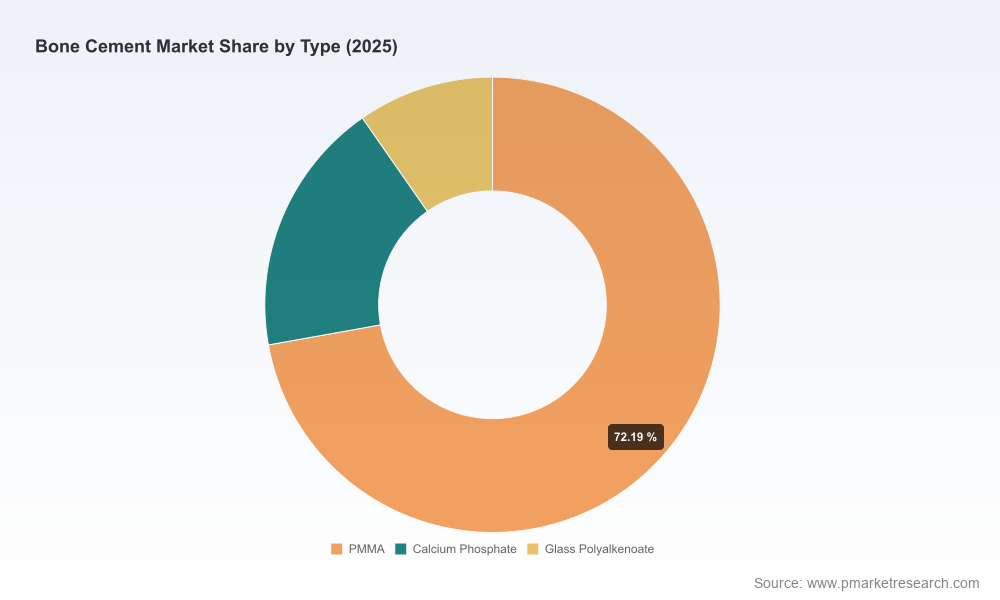

These macro dynamics reflect a combination of demographic tailwinds (orthopedic procedure volumes), technology substitution (antibiotic-loaded formulations, radiopaque blends, and spinal augmentation systems), and episodic market shocks that temporarily reallocate demand between suppliers. Importantly, market concentration is meaningful: the top three players account for approximately half of global revenues (CR3 ≈ 49.5%), and the top five approach roughly two‑thirds (CR5 ≈ 68.2%). This structure creates both barriers and opportunities: scale advantages for incumbents, and outsized reward for nimble challengers who can exploit short-term supply gaps and differentiated clinical positioning.

Bone Cement Market

What the full report contains (practical, transaction‑ready content)

- Comprehensive market model (2020–2032) with scenario toggles—base, downside, and accelerated adoption—that let you stress-test revenue and margin outcomes under alternative assumptions.

- Go‑to‑market playbooks by product type and clinical application that prioritize interventions with the highest near-term ROI (pricing levers, channel mix, KOL deployment, hospital bundling strategies).

- Supply‑chain resilience matrix that maps single‑sourced components, critical manufacturing nodes, and practical contingency steps (dual-sourcing triggers, consignment inventory thresholds, shelf‑life management).

- Regulatory and reimbursement tracker with impact scoring—linking MDR/FDA/NTAP events to revenue timing and payer negotiation strategies.

- Competitive intelligence dossiers on leading and challenger suppliers, including product line maps, pricing posture, patent landscape snapshots, and acquisition targets segmented by strategic fit.

- M&A and partnership decision framework—valuation sensitivities, integration scorecards, and an initial shortlist of tuck‑in targets and upside pools.

Competitive landscape: what to watch in 2026

The market is shaped by a mix of global medtech incumbents and specialized biomaterials players. Established orthopedics firms maintain strong channel access and hospital relationships; nimble specialist companies focus on infection control, radiopacity, and spinal augmentation niches. The firms profiled in our report include, among others, Heraeus Medical, Zimmer Biomet, DePuy Synthes (Johnson & Johnson), Stryker, Tecres S.p.A., Biocomposites, OsteoRemedies, Medtronic Sofamor Danek, Arthrex, and Amber Implants.

- Incumbent strength: Large device companies bring integrated sales forces and broad hospital account relationships that help them convert rapid demand shifts into sustained volume gains.

- Specialist advantage: Companies focused on antibiotic-loaded formulations or delivery systems have disproportionate leverage when infection prevention and supply continuity become procurement priorities.

- Consolidation tailwinds: Strategic acquisitions and asset purchases are already evident; expect more M&A directed at infection-control technology and spinal augmentation IP.

Recent developments that rewrite near‑term assumptions

- Supply shock: In February 2026, a packaging fault at a major producer forced a temporary production halt for pouch bone cement, causing week-to-week procedural impacts in high-volume health systems. The interruption highlights how single-node failures can ripple across national provider networks.

- Buyer response: Large buyers and public systems moved quickly to procure alternatives from several established suppliers to maintain scheduled operations—demonstrating the speed at which procurement teams can reprioritize trusted brands during crises.

- Market acceleration by challengers: Select specialist manufacturers advanced launches of antibiotic-loaded variants into affected markets to capture emergent share during the supply shortage.

- Regulatory and reimbursement shifts: Notable approvals and reimbursement updates in 2024–2026—such as targeted NTAP-style add-on payments for new technologies used in acute trauma—create differentiated commercial economics for novel materials and procedures.

- Strategic transactions: Recent acquisitions to reinforce infection-control portfolios signal continued consolidation and bolster incumbents’ ability to offer bundled clinical solutions.

Strategic implications for 2026 planning

Below are priority actions that companies should consider to convert market dynamics into advantage during 2026 planning cycles. Each recommendation is linked to quantified levers in our full model.

- Embed supply resilience into commercial contracts: Negotiate tiered volume agreements with explicit alternative-supply triggers and penalty structures. Small investments in dual-sourcing and qualified secondary production lines can prevent outsized revenue volatility during acute interruptions.

- Prioritize infection‑management and value‑add formulations: Given payer interest and recent reimbursement examples favoring technologies that reduce complication costs, firms with antibiotic-loaded or bioactive cement lines should accelerate clinical evidence generation and HTA submissions.

- Leverage short-term demand surges to lock long-term contracts: Where competitors falter, convert emergency ordering relationships into multi-year preferred-supplier agreements via improved terms, integrated service offerings, and outcome-sharing pilots.

- Pursue bolt-on acquisitions that deliver immediate fill‑rate or technology differentiation: Targets that provide complementary IP in infection control, radiopacity, or spinal augmentation yield near-term revenue uplifts and reduce dependence on a narrow set of SKUs.

- Invest in modular packaging and logistics: Manufacturing changes that reduce single-point packaging risks (e.g., shift to dual‑format packaging validated under regulatory regimes) materially lower the risk of production halts.

- Design hospital‑centric commercialization: Offer peri‑operative bundles and supply‑chain transparency that align with hospital inventory management objectives—creating stickiness beyond commodity pricing.

How PW Consulting’s analysis accelerates your 2026 playbook

Our full Bone Cement Market report converts the macro picture into prescriptive decision assets: revenue scenario models ready for CFO review, M&A target shortlists calibrated to strategic fit, and an operational checklist for immediate supply‑chain hardening. The report’s layered deliverables—executive dashboards, playbooks, and competitor dossiers—are designed so that commercial, supply‑chain, and corporate development teams can act within weeks, not months.

Methodology, caveats, and next steps

The analysis leverages audited market revenue series (2020–2025), primary interviews with hospital buyers and KOLs, and a regulatory/reimbursement event tracker to inform our 2026–2032 scenarios. While this preview highlights macro growth and systemic risks, detailed segment-level datapoints, regional splits, and transaction‑level assumptions are intentionally omitted here to preserve the report’s proprietary value and to direct stakeholders to the full dataset for executable insights.

For executives planning investments, supply diversification, or M&A in 2026, the window for locking differentiated advantage is narrow. Short-term moves—strengthening secondary supply, accelerating regulatory filings, or selectively pursuing concerted acquisitions—can translate into outsized value as the market scales toward the 2030s.

Contact and call to action

Access to the full PW Consulting Bone Cement Market report provides the granular segmentation, pricing matrices, and competitor financial profiles needed to execute the recommendations above. Reach out to our market team to request the full dataset and a tailored 90‑day implementation workshop for your leadership team.

For detailed analysis of this topic, please visit the official page:Bone Cement Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com