Clinical Mass Spectrometry Market: Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present this strategic preview to orient executive teams, corporate development groups, and clinical laboratory leaders preparing for critical 2026 decisions. Built on our comprehensive market study (base year 2025; historical window 2020–2025; forecast horizon 2026–2032), this piece distills the high‑value, decision‑grade takeaways without disclosing the granular segmentation that resides in the full report. Think of this as the trailer: rigorous, directional and actionable — intentionally withholding the detailed scene-by-scene analytics that drive transaction and deployment decisions.

Clinical Mass Spectrometry Market

Why this market matters in 2026

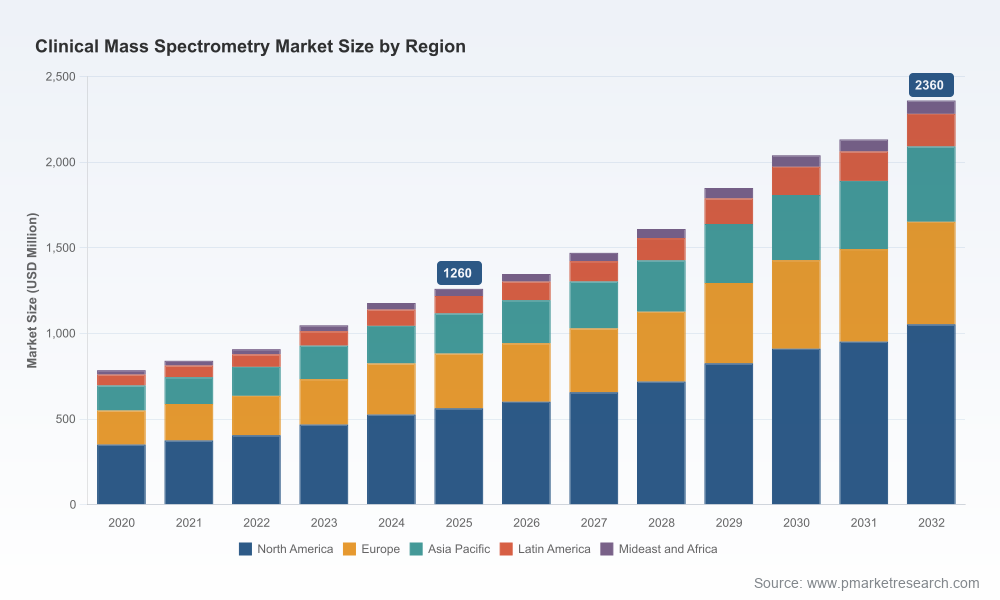

Clinical mass spectrometry is no longer a niche back‑office tool. Over the recent five‑year historical period, adoption accelerated as clinical laboratories sought higher accuracy, multiplexing capability and cost‑effective workflows for therapeutic drug monitoring (TDM), steroid profiling, vitamin D metabolites, newborn screening, and microbiology identification. Our 2025 base assessment pegs the global market at USD 1,260 Million (revenue unit: USD Million). With a compound annual growth rate (CAGR) of 9.35% across 2026–2032, the market is forecast to approach approximately USD 2,360 Million by 2032 — underlining sustained demand across clinical and reference laboratory settings.

Clinical Mass Spectrometry Market

That growth is not monolithic. It is driven by converging forces: regulatory clarifications that lower operational barriers, platform vendors commercializing automated IVD solutions, reimbursement code updates improving billing clarity, and the maturing of software and informatics ecosystems that reduce the integration friction for high‑throughput clinical labs. For executives evaluating capital allocation, partnerships, or M&A targets in 2026, those forces create discrete windows of opportunity and risk that our report maps in operational terms.

Clinical Mass Spectrometry Market

What the full report delivers (practical scope)

- Validated market sizing (2020–2025 historical) and forward projection (2026–2032) with scenario bands tuned to regulatory and reimbursement inflection points.

- Multi‑dimension segmentation by product type, clinical application and geography, plus sensitivity testing to highlight which subsegments drive value under alternate adoption curves.

- Competitive landscape and concentration analysis (market concentration metrics included) with vendor scorecards covering product breadth, go‑to‑market models, installed base, service footprint, regulatory filings and partnership pipelines.

- Regulatory and reimbursement matrix that crosswalks key jurisdictions, anticipated timelines for IVDr/IVD clearances, CLIA classification impacts, and CPT code implications for clinical billing.

- Operational playbooks — procurement, lab footprint optimization, automation and informatics integration — including modelled ROI and throughput break‑even analyses for common deployment scenarios.

- M&A and partnership screening framework that highlights targets by strategic fit (technology stack, customer overlap, or complementary service models) and an acquisition valuation primer.

- Primary interviews and case studies from reference labs, hospital systems and diagnostic OEMs to ground recommendations in real‑world constraints.

We deliberately do not publish the full subsegment tables in this preview; those are available through our report portal for teams that require line‑level numbers for diligence and budgeting.

Competitive dynamics: who matters and why

The market exhibits moderate concentration: the top three global vendors account for a meaningful share of commercialized clinical MS platforms and IVD workflows, with broader top‑five concentration reinforcing scale advantages in reagent supply, service, and regulatory resources. That dynamic creates defensible positions for incumbents, while also opening spaces for focused entrants that bring differentiated software, automation or application‑specific reagent packs.

- Thermo Fisher Scientific — A dominant systems and software supplier with vertically integrated offerings for quantitative LC‑MS workflows. Their focus on quantitative software and single‑quadrupole LC‑MS instrumentation positions them strongly in verification and precision medicine workflows where throughput and quantitative consistency are core purchase drivers.

- Waters Corporation — Strong in LC‑MS/MS platforms and clinical workflow solutions, with platforms that have been positioned toward therapeutic drug monitoring and biomarker workflows. Waters’ experience navigating regulatory submissions for clinical assays and their installed base in high‑throughput labs remains a competitive advantage.

- Bruker Daltonics — Notable for microbial identification solutions and software that target rapid organism ID/differentiation from clinical samples. Recent clearances have solidified Bruker’s position in clinical microbiology and opened up adoption in regulated laboratory settings.

- Roche Diagnostics — An emerging force in automated mass spectrometry for clinical use, pairing instrument platforms with IVD‑grade reagent packs and a broad hospital lab go‑to‑market reach. Roche’s integrated IVD approach — combining automation and prepackaged reagents — is reshaping expectations around ease‑of‑use for clinical MS deployments.

Each vendor presents a different proposition for potential partners or acquirers: from instrument OEMs emphasizing throughput and service economics, to diagnostics players prioritizing IVD reagents and automation that lower operator skill requirements. Our full vendor profiles benchmark these providers across commercialization vectors and highlight where third‑party reagent and software ecosystems could create disintermediation or new partnership layers.

Regulatory and reimbursement inflection points — 2025–2026 impact

Regulatory actions in late 2025 and early 2026 materially change the adoption calculus.

- CE Mark expansions for reagent packs on automated mass spectrometry platforms have broadened the IVD menu available to clinical labs, strengthening the business case for integrated instrument‑reagent purchases from major OEMs.

- FDA and CLIA actions that clarify complexity classification for certain MS assays reduce the skilled operator barrier, enabling broader deployment in routine clinical laboratories rather than limiting assays to specialized reference centers.

- Regulatory classification of microbial ID MS systems under special controls classifies the risk pathway for clinical microbiology platforms, giving hospitals increased confidence in adoption.

- CPT updates in 2026 that revise mass spectrometry coding introduce both clarity and short‑term billing variability across payers. For labs, the near‑term effect will be active billing optimization and test‑menu prioritization while payer policies stabilize.

For corporate strategists, the sequencing of approvals and code updates creates phases for go‑to‑market: initial IVD launches that target high‑value, well‑reimbursed assays; followed by broader automation and decentralization plays as CLIA complexity designations favor adoption by routine labs.

Strategic implications and 2026 playbook

Based on the synthesis of primary interviews, channel checks and market modelling, the following strategic priorities should guide 2026 decisions:

- Prioritize integrated IVD stacks for hospital and large reference lab partners. Vendors that pair automated platforms with validated reagent packs can shorten sales cycles and command premium positions in tender processes.

- Invest in software and automation that lower operator skill requirements. CLIA reclassification trends favor solutions that reduce the need for highly trained mass spectrometry specialists, expanding addressable markets into community labs.

- Engage payers and professional societies early on reimbursement strategy. CPT and payer policy volatility in the near term means commercial teams should model multiple reimbursement scenarios and secure early payer agreements for high‑value analytes.

- Adopt a modular partnership approach for service and reagent supply. For incumbents, defending installed base value requires bundled service agreements; for new entrants, developing reagent or informatics niches that attach to OEM hardware can be an efficient entry path.

- Use regulatory sequencing as a program management lever. Time product launches and market expansion to the expected cadence of regional regulatory clearances and local policy updates to maximize access and minimize launch risk.

- Consider targeted M&A to acquire clinical validation expertise or reagent portfolios rather than duplicating lengthy internal development — especially when pursuing IVD labeling and reimbursement traction.

Where our analysis adds immediate value

For teams constrained by runway or looking to prioritize a single strategic initiative in 2026, our research offers three immediate, operationally framed deliverables:

- Deployment playbooks with throughput and ROI models tailored to three archetypal lab sizes — enabling rapid CapEx/Opex modelling during budget cycles.

- Regulatory risk heatmaps that translate recent approvals and classifications into market access timelines by jurisdiction — critical for sequencing product launches and commercial investments.

- M&A target shortlists and valuation ranges for bolt‑on opportunities that accelerate access to IVD reagent menus, clinical validation cohorts, or specialized informatics software.

These deliverables are accompanied in the full report by the granular tables, scenario stress tests and appendix materials that corporate development, strategy and commercial teams require to move from strategy to execution.

Next steps and how to use this preview

This preview is designed to do three things: (1) provide an executive lens on market dynamics through 2026 and beyond; (2) surface the structural and regulatory levers that materially affect adoption and monetization; and (3) demonstrate the practical outputs available in the full PW Consulting report that support capital, partnership and operational decisions.

If your team is preparing a 2026 budget, a market entry plan, or diligence on an acquisition target in clinical mass spectrometry, the full study contains the granular segmentation, regional and application-level financials, and the decision‑grade annex that we intentionally omit here to preserve the strategic value of the primary intelligence.

Contact PW Consulting for access to the full Clinical Mass Spectrometry Market report, vendor scorecards and our interactive scenario model — or commission a tailored workshop where we apply the data to your organization’s specific portfolio and market objectives.

For detailed analysis of this topic, please visit the official page:Clinical Mass Spectrometry Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com