Bimetallic Bandsaw Blade Market — Strategic Briefing for 2026 Decision Makers

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a concentrated, executive-level briefing that synthesizes the research and strategic implications from our full Bimetallic Bandsaw Blade Market study (base year 2025). This note is designed to help industrial OEMs, distributors, procurement leaders, and private equity teams align 2026 plans to the most material forces shaping the market—while preserving the segment-level intelligence reserved for subscribers to the full report.

Bimetallic Bandsaw Blade Market

Top-line market context

The bimetallic bandsaw blade market has transitioned from fragmentation toward increasing consolidation while expanding in absolute scale. Our market model shows a progression from approximately USD 420.5 Million in 2020 to USD 555.0 Million in 2025 (base year). At a compound annual growth rate (CAGR) of 6.5% across the forecast horizon, the market is projected to approach roughly USD 860 Million by 2032. These dynamics make the segment attractive for margin capture, selective vertical integration, and differentiated product playbooks.

Bimetallic Bandsaw Blade Market

Why the 2026 inflection matters

- Timing for procurement cycles: Capital procurement and plant modernization plans initiated in 2026 will lock in blade and machine supplier relationships that can last multiple years. Early contractual advantages—pricing tiers, service SLAs, and joint inventory programs—translate directly to cost-per-cut outcomes.

- Cost volatility and hedging: Upstream cost pressures, notably in high-speed steel inputs, have created windows for strategic sourcing and long-term purchasing agreements. Buyers who integrate material-cost clauses and alternative-sourcing routes in 2026 will preserve margins as prices evolve.

- Automation adoption acceleration: Workforce shortages and automation mandates are catalyzing investments in automated sawing cells that run optimized bimetallic blades. Suppliers and users who act in 2026 can capture share by co-developing tooling-to-machine packages.

Key market drivers and dynamics

- Durability premium versus unit economics: Bimetallic blades continue to displace conventional options in high-throughput environments because of superior lifecycle and lower tool-change frequency. This is increasingly relevant where labor is constrained and uptime is prioritized.

- Raw material cost trends: Our sector analysis indicates that molybdenum-rich grades of high-speed steel advanced with a roughly 9.4% CAGR into 2025, reinforcing the relative value of bimetal formulations that leverage these alloys for improved edge life. Procurement and product managers must balance this raw-material inflation with premium pricing models tied to demonstrable life-cycle savings.

- Regulatory and energy efficiency drivers: Energy-efficiency mandates and production cost scrutiny favor tooling choices that reduce cycle-time and energy per cut. Bimetal blades—when matched to process parameters—offer quantifiable energy and throughput advantages that support justification for higher initial spend.

- Consolidation and market concentration: Market concentration is materially high: the top three competitors command a significant share of the market, and the top five raise that dominance further. This concentration creates both risk (price setting, OEM-distributor dynamics) and opportunity (M&A, white-space for niche specialists).

Competitor landscape — what we observed

The competitive environment is anchored by established Western manufacturers complemented by regional producers who compete aggressively on cost and service. Key players profiled in our research include (company HQ and web presence):

Bimetallic Bandsaw Blade Market

- Lenox Tools (United States) — https://www.lenoxtools.com

- M.K. Morse Company (United States) — https://www.mkmorse.com

- DoALL Sawing Products (United States) — https://www.doallsaws.com

- Wikus (Germany) — https://www.wikus.de

- L.S. Starrett Company (United States) — https://www.starrett.com

- Bahco (Sweden) — https://www.bahco.com

- Eberle (Germany) — https://www.eberle-augsburg.de

- Simonds International LLC (United States) — https://www.simondssaw.com

- Bichamp Cutting Technology Co Ltd (China) — https://bichamp.com

- Honsberg (Germany) — https://www.honsberg.de

These vendors pursue differentiated plays: technological leadership through advanced tooth geometry and materials; channel strength via distribution and fleet-support models; cost leadership via regional manufacturing and supply-chain optimization; and application specialization for sectors such as heavy fabrication, aerospace, and automotive. Recent vendor activity—particularly from a leading German supplier—shows intensified engagement in trade shows and industry events throughout 2025 to push new product generations and industry partnerships.

Recent industry signals to monitor in 2026

- Trade-show-led product introduction cycles: Major manufacturers used 2025 trade fairs to preview blade innovations and application-specific solutions; expect productization and commercialization announcements in 2026 that will influence sourcing decisions.

- Standardization of automation interfaces: As sawing cells are rationalized into automated lines, tooling suppliers that offer digital integration (predictive wear, remaining-life algorithms) will secure longer-term OEM ties.

- Supplier consolidation risk: Given the market’s concentration profile, strategic acquisitions or distribution realignments remain plausible—these would reshape pricing dynamics and access to technology.

What the full PW Consulting report delivers (practical content)

Our full study is built for decision-use and includes the following operational modules:

- Market model and scenario forecasts (2026–2032) with sensitivity testing for raw material prices, automation adoption rates, and regional demand shifts.

- Supply chain maps and cost-to-serve benchmarks for OEMs and distributors, including freight, duties, and inventory stratification tactics.

- Channel and distribution playbooks—pricing strategies, bundle offers (blades + services), and aftermarket programs to increase customer lifetime value.

- Vendor scorecards and capability matrices that assess R&D depth, production flexibility, quality systems, and aftermarket support.

- Buying guides and procurement clauses—practical templates for long-term contracts, performance warranties, and inventory consignment models.

- Operational checklists for shop-floor optimization—recommended parameter ranges, changeover protocols, and a decision tree for blade selection by cut-type and material.

- Executive M&A and partnership roadmaps—identifying white-space targets, integration risks, and valuation levers specific to tooling businesses.

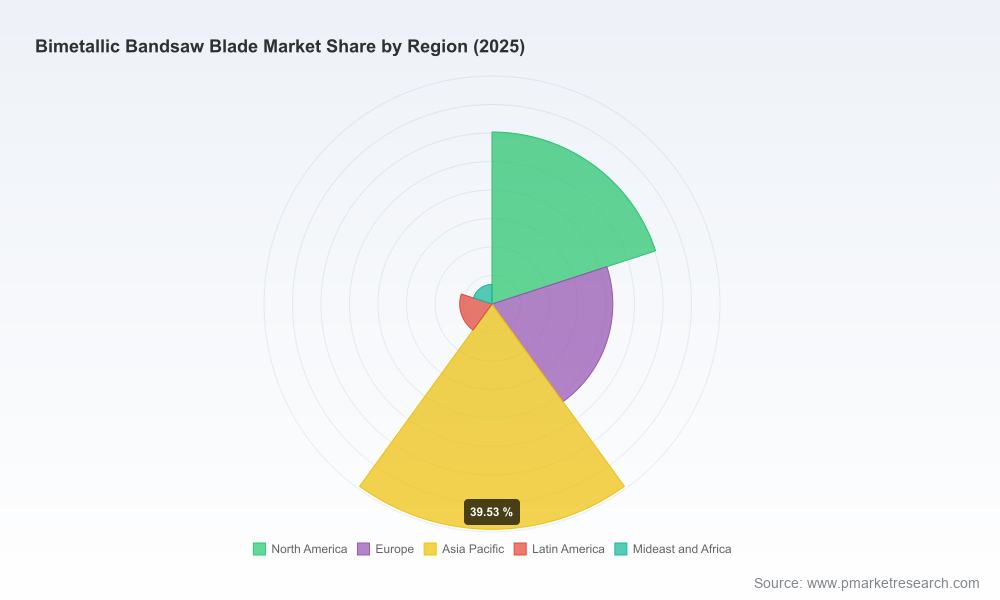

Note: Detailed regional split figures, application-level revenue breakdowns, vendor market shares by segment, and unit-volume price curves are intentionally omitted from this briefing to preserve the investigative value contained in the subscriber-only report.

How to use this intelligence in 2026 — tactical recommendations

- Operators and OEMs: Lock in supply agreements with tiered pricing tied to demonstrable life-cycle KPIs (cuts per blade, downtime reduction). Prioritize suppliers offering digital monitoring to reduce unexpected changeovers.

- Distributors: Reconfigure inventory to emphasize high-turn bimetal assortments and offer bundled service contracts that monetize shop-floor optimization expertise.

- Product teams: Invest in R&D that targets energy-efficiency claims and tooth geometries optimized for automated cells—these attributes will be primary purchase drivers for high-volume customers.

- Investors: Seek targets that combine channel strength with proprietary metallurgy or software-enabled service offerings. The combination de-risks commoditization and supports margin expansion.

Final strategic note — why our analysis matters to your 2026 planning

The bimetallic bandsaw blade market presents a classic industrial inflection: rising absolute demand, material cost pressure, labor-driven automation acceleration, and a competitive landscape skewed toward a handful of dominant suppliers. For stakeholders who must decide in 2026—whether to source, partner, invest, or consolidate—timing and specificity matter. Acting with precise, segment-level intelligence (product, region, and application) will materially alter procurement economics and growth outcomes.

PW Consulting’s full report provides the segmented datasets, vendor-level economics, and implementation playbooks required to convert strategic intent into operational advantage. For the granular tables—regional and application splits, vendor shares, pricing ladders, and the full scenario model—refer to the subscriber edition of the study or contact our team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Bimetallic Bandsaw Blade Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com