Automotive Industry: Designing Effective Go-to-Market Strategies Through Strategic Intelligence

Other |

2026-03-12 09:23:36

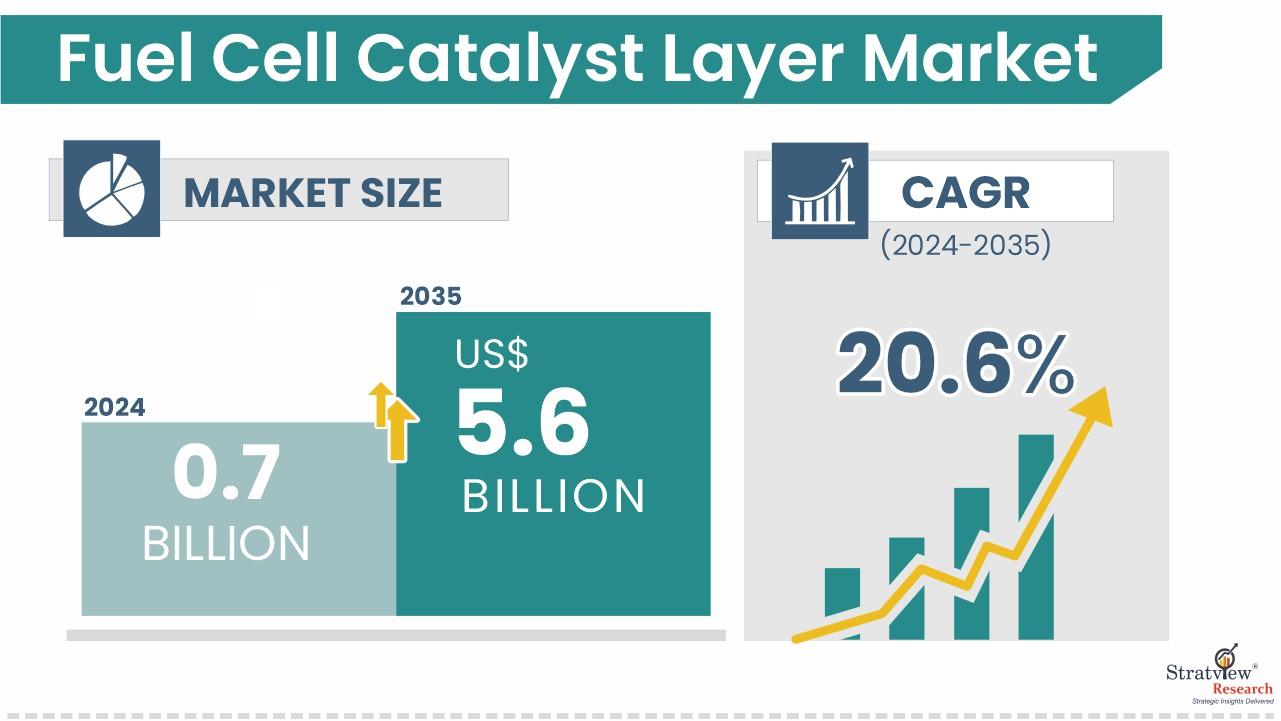

The Fuel Cell Catalyst Layer Market was valued at USD 0.7 billion in 2024 and is likely to reach USD 5.6 billion by 2035. The market is forecast to grow at a CAGR of 20.6% during 2024-2035. The Fuel Cell Catalyst Layer Market is expected to grow at a CAGR of 20.6% during 2024-2035. This growth trajectory is linked to clean energy demand and hydrogen fuel cell adoption.

In market forecast terms, Fuel Cell Catalyst Layer Market size is expanding because catalyst layers determine fuel cell performance, efficiency, and lifespan. These layers support electrochemical reactions that produce electricity by enabling fuel breakdown and reduction-oxidation processes. Request a free sample report: https://www.stratviewresearch.com/Request-Sample/fuel-cell-catalyst-layer-market#form

The Fuel Cell Catalyst Layer Market is segmented by Fuel Cell Type (PEMFC (Proton Exchange Membrane Fuel Cell), SOFC (Solid-Oxide Fuel Cell), PAFC (Phosphoric Acid Fuel Cell), MCFC (Molten-Carbonate Fuel Cell), DMFC (Direct Methanol Fuel Cell), and AFC (Alkaline Fuel Cells)), by Application Type (Transportation, Stationary, and Portable), by Base Material Type (Platinum-based, Palladium-based, Non-precious Metal Catalysts, and Other Base Materials), and by Region.

In Fuel Cell-Type Analysis, PEMFC, SOFC, PAFC, MCFC, DMFC, and AFC define the market structure. PEMFCs are expected to be the demand generator for the global catalyst layer market due to their overall dominance in the fuel cell market. Their demand profile is supported by transportation, portable, and stationary power applications.

In Application-Type Analysis, Transportation, Stationary, and Portable define end-use demand. Transportation is anticipated to be the largest application employing the catalyst layer. The rise of fuel cells in mobility contributes heavily to market expansion, especially as hydrogen fuel cell vehicles require durable and efficient catalyst layers.

In Base Material-Type Analysis, Platinum-based, Palladium-based, Non-precious Metal Catalysts, and Other Base Materials define the material landscape. Platinum-based materials have dominated the market in the past and will continue to reign during the forecast period. Their superior performance keeps them central, even as players work on Non-precious Metal Catalysts and lower-cost alternatives.

Asia-Pacific is expected to maintain its reign over the forecast period. The region remains the most crucial driver of the Fuel Cell Catalyst Layer Market due to its fuel cell technology adoption rate, favorable governments, and evolving hydrogen infrastructure. China, Japan, and South Korea are key contributors to catalyst layer demand through hydrogen FCEVs, stationary fuel cells, and renewable power initiatives.

Asia-Pacific is projected to experience the highest market growth. China is expanding hydrogen production and deploying fuel cell buses and trucks. South Korea’s hydrogen economy plans and Japan Hydrogen Society Roadmap further support regional growth. These developments strengthen Asia-Pacific’s position in regional analysis and reinforce its role in the market outlook through 2035.

Industry trends are centered on cleaner energy choices, material efficiency, and reduced dependence on high-cost precious metals. Innovations in material technology, including Non-precious Metal Catalysts, are emerging to replace high-cost precious metals such as platinum. This supports a more cost-focused industry outlook while keeping catalyst layer performance central to fuel cell adoption.

The competitive landscape is also being influenced by advanced materials, supply chain strengthening, and production-cost reduction. Recent market activity shows interest in catalyst supports, fuel cell materials, and green fuel cell catalyst production. Product development is focused on improved efficiency and lifespan, which directly supports the long-term Fuel Cell Catalyst Layer Market forecast.

Johnson Matthey

Umicore

BASF SE

3M

Huntsman International LLC

Heraeus Holding

Haldor Topsoe

Clariant

Tanaka Holdings Co., Ltd.

Ballard Power Systems

Plug Power Inc.

Nisshinbo Holdings Inc.

De Nora

Fuel Cells Etc

Sunrise Power

The Fuel Cell Catalyst Layer Market presents a high-growth market forecast, rising from USD 0.7 billion in 2024 to USD 5.6 billion by 2035. With a CAGR of 20.6%, the market is shaped by clean energy demand, hydrogen fuel cell adoption, material innovation, and renewable energy investment. Strategic insights point to catalyst performance, cost reduction, and Asia-Pacific leadership as core market themes. The industry outlook remains closely tied to fuel cell commercialization.

The Fuel Cell Catalyst Layer Market was estimated at USD 0.7 billion in 2024. It is likely to reach USD 5.6 billion in 2035.

The Fuel Cell Catalyst Layer Market is expected to grow at a CAGR of 20.6% during 2024-2035. This growth is supported by hydrogen fuel cell adoption and material technology advancements.

Growth is driven by clean energy demand, supportive government policies, green hydrogen objectives, and fuel cell adoption in transportation and stationary power. Catalyst layers remain essential because they influence performance, efficiency, and lifespan.

Asia-Pacific leads the Fuel Cell Catalyst Layer Market. China, Japan, and South Korea support regional demand through hydrogen FCEVs, stationary fuel cells, and renewable power initiatives.

The investment outlook is linked to material technology, renewable energy, fuel cell-based electricity generation, and hydrogen infrastructure. Challenges include high production costs, complex manufacturing, raw material shortages, and competition from alternative energy solutions.