Textile Chemicals Market — 2026 Strategic Preview

Market snapshot: what the numbers are telling senior leaders

The global textile chemicals market has transitioned from recovery into structurally stronger growth. After expanding from approximately USD 21.5 Billion in 2020 to USD 30.0 Billion in 2025 (base year), industry momentum continues into the forecast window. Our model projects the market to reach roughly USD 41.3 Billion by 2032, equating to a mid-single‑digit compound annual growth rate (CAGR) of 4.8% across the 2026–2032 period. Market concentration is moderate: the top three players account for around 45% of industry revenues and the top five about 55% — a profile that rewards scale and speciality capabilities while leaving latitude for nimble challengers and regional champions.

Textile Chemicals Market

Why this preview matters for 2026 enterprise decision-making

- Timing matters: 2026 is a pivot year — regulatory thresholds tighten, trade‑show calendars re‑align, and brands accelerate procurement audits. Decisions taken now on supplier strategy, product roadmaps, and compliance investments will determine cost and market access throughout the next planning cycle.

- Growth is selective: Aggregate expansion is healthy but uneven; pockets of premium demand (functional finishes, sustainable auxiliaries, performance dyeing) are expanding faster than commodity volumes. Identifying where to invest R&D or commercial focus requires forward-looking segmentation and price‑elasticity analysis.

- Risk vs return on sourcing: Raw material volatility, wastewater compliance and supplier audit burdens are increasing procurement TCO. Firms that quantify regulatory exposure and embed it into total cost models will command better margin preservation and fewer disruption events.

Key market dynamics shaping strategy in 2026

Three structural dynamics dominate the strategic landscape:

Textile Chemicals Market

- Standards and regulation are accelerating product obsolescence. 2025–2026 saw multiple important updates: national bans on certain chemistries, tightened limit values under certification schemes, and new mandatory due‑diligence expectations for organic textiles. These shifts shorten the runway for legacy chemistries and raise the bar for documentation, testing and supplier transparency.

- Sustainability is now table stakes for market access. Beyond brand positioning, compliance with wastewater guidance, microfibre research outcomes and traceability programmes is becoming a procurement filter for many buyers. Suppliers without scalable low‑impact formulations, clear chain‑of‑custody credentials, and supporting test data will risk losing preferred supplier status.

- Channel and service differentiation create premium pockets. Distributors and ingredient specialists that combine formulation expertise, regulatory advisory and local application support are retaining business even where prices compress. Conversely, pure commodity suppliers face margin pressure unless they pursue consolidation or downstream integration.

Regulatory & standards watchlist (what to build into 2026 plans)

- Certification regimes have tightened: expect new chemical input criteria and on‑site audit requirements for organic textiles to be enforced in the near term. Build a compliance roadmap that covers input approvals, audit readiness and substitution timelines.

- Substance restrictions are expanding rapidly: several jurisdictions have introduced bans or strict limits on legacy substances used for water- and stain‑repellency, and certification bodies have reduced allowable thresholds for endocrine‑active and persistent chemicals. Scenario‑planning for product reformulation is no longer optional.

- Collective wastewater and microfibre guidelines have moved from voluntary to de‑facto procurement requirements in many large accounts. Capital allocation for effluent treatment and testing partnerships should be evaluated against lost revenue risk.

Competitive landscape — actionable takeaways on leading players

The market combines global multinational scale players with strong regional specialists. While we withhold detailed share matrices in this preview, the following high‑level profiles frame partner and competitor assessment:

Textile Chemicals Market

- Archroma (Switzerland) — Global leader with a strong sustainability narrative and broad portfolio across dyes, colorants and performance chemistries. Their capability in regulatory‑compliant alternatives and application support makes them a go‑to for brand owners seeking fast substitution pathways. (https://www.archroma.com)

- Sarex Chemicals (India) — Specialist in textile auxiliaries and pretreatment chemistries with deep local market reach. Competitive where cost, local service and rapid on‑site troubleshooting matter.

- Fineotex Chemical (India) — Positioned across the value chain from pre‑treatment to finishing, with an emphasis on specialty and performance formulations tailored to regional supply chains.

- Azelis (Belgium) — Distributor with integrated supply solutions, enabling principals to reach fragmented processors. Expertise in formulation bundling and customer technical support reduces buyer switching costs.

- Huntsman Textile Effects (Switzerland/Germany) — Focused on functional dyes and finishing systems for performance apparel and technical textiles; strong R&D credentials underpin premium pricing in advanced applications.

- NICCA Chemical (Japan) — Known for scouring, dyeing and finishing chemistries with an emphasis on high‑precision processing and quality control in technical applications.

- CHT Group (Germany) — Specialist in auxiliaries and dyeing solutions with capability in both commodity and functional chemistries; appeals to processors needing integrated process support. (https://www.cht.com)

Strategic implications: alliances and co‑development agreements with suppliers that combine formulation expertise and compliance services can shortcut time‑to‑market for reformed chemicals. Distributors that can package technical service and regulatory assurance will expand margin opportunities even as raw material volatility compresses base chemistry pricing.

Recent industry developments you cannot ignore

- Trade events are regrouping product categories: new dedicated segments for textile chemicals & dyes at major shows signal renewed B2B matchmaking and fast‑track customer discovery opportunities for product launches.

- Standards updates from major certifiers are tightening input approval and SVHC limits. These are triggers for immediate product portfolio reviews and supplier audits.

- Collective programmes on wastewater and microfibre mitigation have added new vendor‑level reporting obligations; early pilots are already affecting supplier selection for large contracts.

What our full report delivers — practical, executable content

We structured the full Textile Chemicals Market report to be a toolset for decision‑makers, not just a slide deck. Highlights include:

- Scenario models mapping demand, pricing and regulatory exposure across the 2026–2032 forecast horizon, enabling ROI calculations for reformulation and compliance capex.

- Supplier risk‑heatmaps and a vetted target list for M&A, joint ventures and distribution partnerships, with commentary on integration complexity and expected synergies.

- Procurement playbooks: total cost of ownership templates that embed testing, certification and wastewater treatment costs into supplier selection.

- Regulatory compliance checklists and substitution timetables aligned to the latest standards and national bans, designed for legal, procurement and R&D teams.

- Operational tools: application‑level technical briefs, pilot design templates, and sample specifications for low‑impact chemistries to accelerate trials.

- Commercial frameworks: pricing sensitivity matrices, channel‑go‑to‑market options, and customer segmentation to prioritise sales focus.

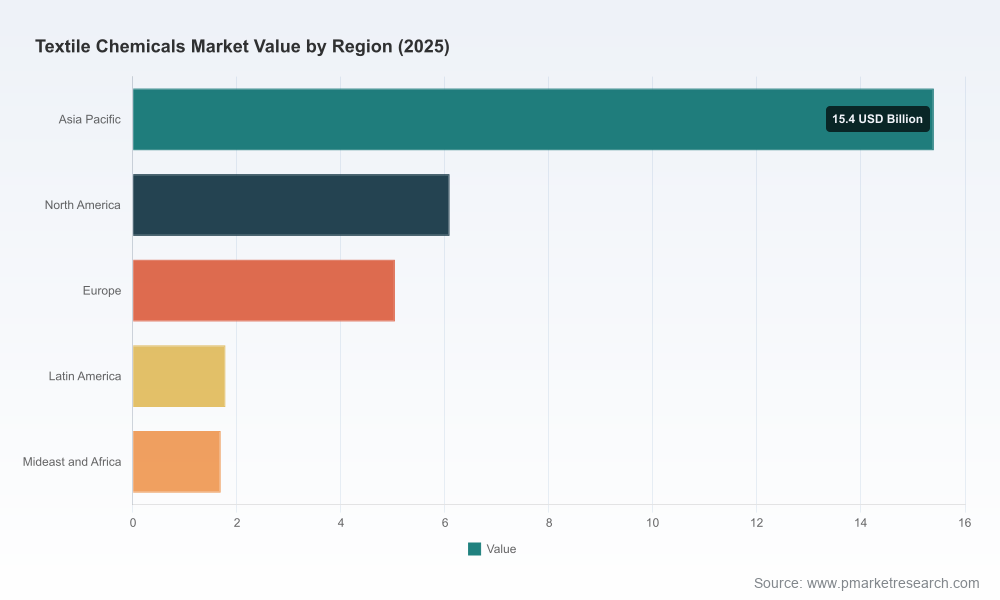

Note: this preview intentionally omits the granular regional, type and application splits included in the full study. The withheld detail is where we translate macro dynamics into precise market entry, pricing and portfolio decisions — access to that dataset is included with the full report.

Strategic playbook for 2026 — three priority actions

- Immediate (0–6 months): Run a rapid product portfolio audit against new certification thresholds and identify “no‑regret” substitutions that secure existing contracts. Concurrently, map the top 10 customers’ compliance expectations to avoid sudden delisting.

- Medium term (6–18 months): Invest in supplier partnerships for alternative chemistries and co‑fund pilots that demonstrate equivalence in performance and compliance. Tie distribution agreements to service KPIs (application support, documentation delivery, audit readiness).

- Longer term (18+ months): Consider bolt‑on acquisitions or minority investments to secure access to niche technologies (e.g., low‑impact fluorine‑free repellents, advanced wastewater additives) and to expedite market penetration where barriers to entry are rising.

How PW Consulting can help

For executives planning 2026 budgets and 3‑year roadmaps, the full Textile Chemicals Market report provides the granular segmentation, supplier benchmarking and scenario tools required to make confident capital, procurement and M&A decisions. This preview is designed to surface the strategic imperatives; the full deliverable converts them into executable actions, with downloadable models and supplier diligence packs.

Next steps

To obtain the full dataset (including the detailed regional, type and application splits), the editable models, and our supplier due‑diligence templates, access the complete report via our web portal. The full report is the only source for the subsegment granularity that will enable precise revenue impact analysis and contract‑level decisions for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Textile Chemicals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com