Quantum Dots Market Trends in Flexible and Wearable Electronics

Other |

2026-06-14 18:20:14

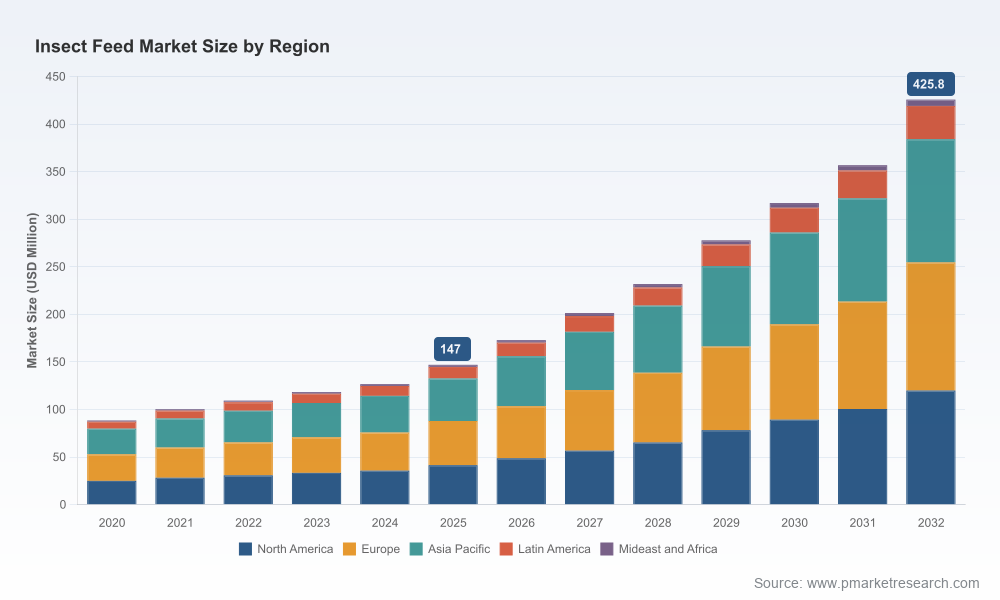

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present this strategic introduction to our latest Insect Feed Market research — a focused, decision-oriented briefing designed to orient corporate leaders, investors, and policy teams preparing for 2026. The market for insect-based feed ingredients has moved from niche innovation to commercial scaling. Our report uses a 2025 base year, tracks historical performance from 2020–2025, and offers a detailed forecast across 2026–2032. At a compound annual growth rate (CAGR) of 16.4%, the market expands from roughly USD 147.0 million in 2025 toward a multi-hundred-million USD opportunity by 2032, signaling both commercial upside and strategic complexity for first movers and incumbents alike.

Insect Feed Market

From pilot to procurement: Many organizations face the classic 2026 inflection — shifting from pilots and R&D to commercial procurement and long-term supplier commitments. Our analysis translates market-scale growth and regulatory inflection points into procurement timelines, price targets, and capacity contingency plans.

Insect Feed Market

Risk-managed scaling: Rapid growth (CAGR 16.4%) can obscure asymmetric risks — feedstock variability, biosecurity, regulatory nuance, and product consistency. The report provides a risk matrix and mitigation playbook tailored to feed manufacturers, aquafeed integrators, poultry and swine formulators, and pet food brands.

Insect Feed Market

Capital allocation & valuation: With the market expanding rapidly over the 2026–2032 horizon, investment choices made this year will disproportionately affect returns. Our model converts market growth scenarios into break-even timelines for brownfield expansions vs. greenfield plants, and into valuation sensitivities for M&A targets.

The market’s evolution between 2020 and 2025 demonstrates accelerating commercial adoption: from an early-stage USD market in 2020 to about USD 147.0 million in 2025. Projecting forward under base-case assumptions, the market scales materially through 2032. The underlying drivers are straightforward: stronger regulatory clarity in key markets, measurable life-cycle sustainability advantages against soy and fishmeal, and industrial innovations that reduce unit costs and increase throughput.

These headline figures are not mere vanity metrics. They represent expanding addressable demand across traditional animal nutrition segments and emerging specialty applications, and they justify investment in industrial-scale production, automation, and integrated supply chains. Yet they also imply the need for granular, scenario-driven planning — which is the operational value our full report delivers.

Regulation as an enabler: The EU framework that permits insect protein in aquaculture feed, and the widening approvals across member states for pig and poultry feed (including specified inclusion limits), have unlocked commercial formulations and offtake agreements across Europe. In the United States, FDA determinations and GRAS pathways have advanced approvals for certain insect proteins, expanding use cases into poultry and pet food.

Sustainability as a competitive moat: Life-cycle assessments show insect feed can reduce land and water use by substantial percentages and significantly lower CO2 emissions relative to conventional proteins. These quantifiable sustainability differentials are increasingly monetizable through procurement policies, ESG-linked finance, and brand-premium positioning.

Feedstock economics: Industrial producers are leveraging upcycled organic waste substrates — food processing byproducts and agri-residues — reducing input costs materially versus conventional protein inputs. This upcycling model underpins unit-cost improvements and circular-economy narratives that buyers and regulators favor.

Market-sizing methodology and transparent assumptions (2020–2032) with scenario trees for conservative, base, and aggressive adoption paths.

Detailed supply-chain maps and bottleneck analysis: substrate sourcing, rearing capacity, processing steps, logistics, and quality assurance nodes.

Technology and process assessment: BSF (black soldier fly) systems, mealworm platforms, automated rearing lines, and downstream processing economics.

Regulatory playbook: jurisdiction-by-jurisdiction permissions, labeling implications, and pathways to expand approved applications.

Commercial go-to-market frameworks: pilot-to-scale templates, offtake contracting models, and procurement scorecards.

Investment cases & M&A diligence checklist: KPIs, capex benchmarks, integration risk matrices, and carve-outs to verify in target diligence.

Financial toolset: a modular financial model in USD (Million unit base) that allows firms to stress-test capacity additions, price trajectories, and margin evolution.

The ecosystem blends pioneering startups, industrial biotech players, and regional specialists. Leading companies are commercializing distinct platform advantages: local production footprints, proprietary rearing technologies, vertical integration into substrate supply, or partnerships with legacy feed leaders.

EnviroFlight (United States) emphasizes domestically produced black soldier fly larvae (BSFL) feed ingredients and early integration with petfood and animal feed value chains. Their focus on localized supply helps buyers reduce scope-3 emissions and logistics complexity.

Innovafeed (France) has moved decisively into North America with a new innovation center in Decatur, Illinois. The facility represents a strategic step toward localizing supply for large aquafeed and livestock partners, shortening commercialization timelines in the U.S.

Protix (Netherlands) positions itself on high-quality, low-impact BSF solutions and has secured industrial supply agreements with established feed players — illustrating a model of partnering rather than competing directly with incumbent ingredient suppliers.

Entobel (Singapore) combines functional ingredient development with B Corp-certification signaling a purpose-led commercialization path in Southeast Asia and beyond.

nextProtein, Hexafly, Beta Hatch, Nutrition Technologies (now rebranded) and others demonstrate diverse strategic approaches — from converting food waste into high-value protein and oils to industrializing mealworm production for zero-waste systems.

Recent corporate moves — Innovafeed’s North American facility commissioning, Entobel’s B Corp certification, Protix’s supply agreements with major feed formulators, and the rebranding of Nutrition Technologies — are not cosmetic. They indicate industrial maturation: scale-focused capex, certification and sustainability signaling, and integration into existing feed supply chains.

Secure strategic substrate partnerships. Prioritize long-term contracts with food processors and agri-waste aggregators to stabilize input costs and enable predictable unit economics.

Lock in offtake pilots with established feed formulators. A proof-of-performance window (typically 6–12 months) with validated nutritional and stability metrics accelerates commercial adoption.

Invest in regulatory engagement and certifications. Active participation in GRAS dossiers, feed labeling harmonization, and demonstrable LCA studies will be a competitive barrier in 2026.

Prioritize automation and biosecurity. Scale requires repeatable processes that limit biological variability and contamination risk — invest early to avoid expensive retrofits.

Embed sustainability verification into commercial contracts. Buyers will increasingly require third-party LCA verification and traceability to achieve ESG goals and access premium markets.

Months 0–3: Run a rapid supplier and substrate audit; initiate regulatory gap analysis in target jurisdictions.

Months 3–6: Launch controlled feed trials with pilot customers; finalize offtakeTermSheets with volume and quality KPIs.

Months 6–12: Execute capacity expansion or brownfield conversion; implement automated rearing subsystems and QA protocols; obtain necessary certifications.

Investors should prioritize targets with three defensible attributes: proprietary process control (automation and yield efficiency), secure substrate access, and validated offtake relationships with large feed formulators. The market remains relatively fragmented; consolidation and strategic partnerships are likely as incumbents secure supply for sustainability-driven procurement programs. Our full report includes a prioritized list of target archetypes and valuation frameworks aligned to 2026 exit horizons.

This preview frames the strategic stakes for 2026: a rapidly growing market driven by regulatory progress, sustainability economics, and industrial scaling. For operational teams and investors, the difference between a successful 2026 market entry and a costly lag will hinge on granular segmentation, price curve sensitivities, and region-specific regulatory timing — the core datasets and scenario models that we deliberately withhold here to preserve the report’s primary value. Access the full Insect Feed Market report for detailed segment economics, downloadable financial models, supplier directories, and our proprietary scenario toolkit designed to turn the 16.4% CAGR opportunity into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Insect Feed Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com