PW Consulting Insight: Fibrinogen Concentrates Market — Strategic Imperatives for 2026

As health systems tighten budgets while procedural volumes and the complexity of bleeding management increase, fibrinogen concentrates occupy an outsized strategic position for manufacturers, hospital systems, and investors. Our latest PW Consulting market study — grounded in historical performance (2020–2025) and forward-looking scenario analysis (2026–2032) — demonstrates a resilient growth path for the category, with a mid-single-digit compound annual growth rate (CAGR) and a near-term market expansion that materially alters competitor economics and go-to-market choices through 2026 and beyond. This briefing synthesizes the report’s high-conviction insights and outlines the decision levers executives should prioritize in 2026. For the granular tables, regional and application splits, and downloadable financial models, refer to the full study.

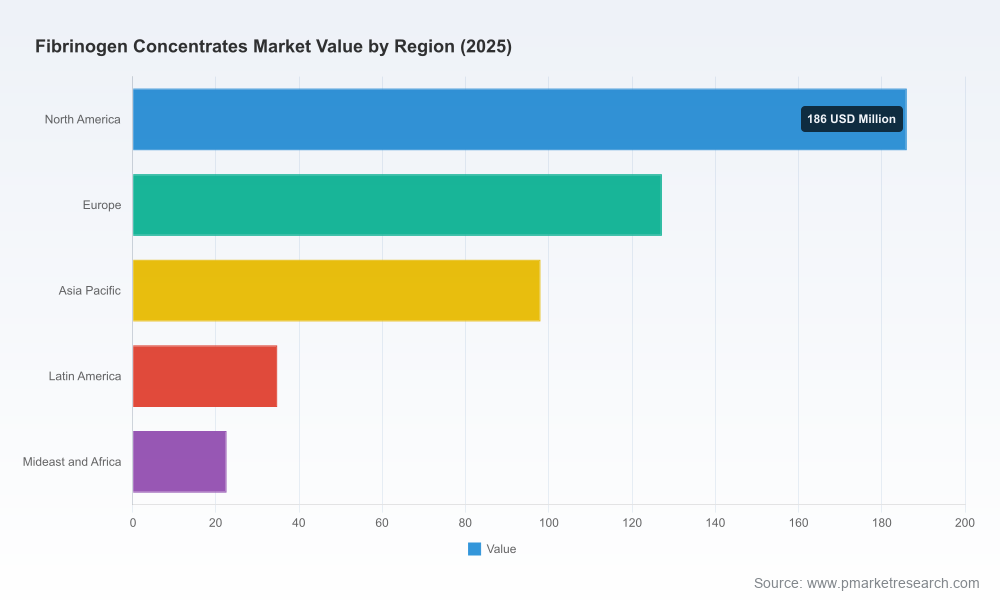

Fibrinogen Concentrates Market

Market trajectory: durability under cost pressure

Between 2020 and 2025 the fibrinogen concentrates market exhibited steady expansion from a base in 2020 to a materially larger global market in 2025. PW Consulting’s forecasts, which incorporate evolving regulatory approvals, presentation innovations, and pricing dynamics, project continued growth through 2032 at a CAGR of approximately 5.96%. By 2032 the market reaches a substantially larger scale than it was in 2025 — a trajectory that validates sustained strategic investments in manufacturing capacity, clinical development, and market access programs.

Fibrinogen Concentrates Market

This growth is not homogenous. It is driven by a convergence of clinical demand (both congenital and acquired indications), improved regulatory clarity, and product-level innovation such as higher-dose or more convenient presentations that reduce administration complexity and procedural overhead. At the same time, upward pressure on raw material and fractionation costs — especially plasma sourcing — and variable reimbursement environments create two parallel realities: stable global demand and uneven commercial returns depending on strategy execution.

Fibrinogen Concentrates Market

Dynamics reshaping strategic choices in 2026

- Regulatory and reimbursement inflection points. Recent regulatory developments have accelerated the commercial runway for leading products. Notably, two regulatory milestones in late 2025 and early 2026 expand therapeutic reach and create differentiated reimbursement profiles for approved products. Additionally, HCPCS coding adjustments implemented in 2026 for a newly approved product alter hospital billing pathways and will materially affect uptake in certain payer segments. These shifts create both opportunities for higher utilization and risks around formulary placement.

- Product presentation matters. Presentation formats that simplify dosing or reduce preparation time (for example, higher‑gram single vials) are increasingly influential in purchasing decisions in high-volume surgical and trauma centers. Manufacturers introducing such presentations stand to capture share through operational value-adds even where unit pricing is under negotiation.

- Cost of therapy and raw-material concentration risks. A standard multi-gram dose represents a meaningful line-item in hospital therapy budgets, and plasma raw material represents the majority component of fractionation costs. This combination constrains hospital willingness to absorb price increases and raises supplier exposure to raw-material price volatility. Organizations that can stabilize plasma sourcing, negotiate long-term supply agreements, or pursue cost-efficient fractionation methods will improve margin resilience.

- Consolidation yet open competition. Market concentration is moderate and concentrated at the top tiers; the three largest players control a meaningful share, with the top five encompassing nearly half the market. That structure favors scale advantages in plasma sourcing, regulatory resources, and commercialization, but still leaves room for regional champions and niche innovators to expand via differentiated clinical propositions and targeted reimbursement strategies.

What 2026 means for executive strategy

- Prioritize portfolio and presentation strategy. For incumbents and new entrants alike, differentiating by presentation (dose strength, reconstitution time, cold-chain profile) will drive hospital procurement decisions. Investment in higher-dose vials or lower-prep-time formats should be modeled not only for incremental unit sales but also for procurement positioning in bundled surgical invoices.

- Lock in plasma supply and optimize fractionation economics. Given that plasma-derived inputs account for the lion’s share of fractionation cost, securing diversified, cost-competitive plasma streams and improving yield efficiency are top priorities. Strategic options include long-term supplier contracts, investments in upstream donor recruitment, and selective vertical integration.

- Embed evidence-generation into reimbursement strategy. Real-world evidence demonstrating reduced transfusion requirements, shorter OR times, or improved perioperative outcomes translates directly into stronger hospital value propositions and payer willingness to reimburse. Plan pragmatic RWE programs alongside pivotal regulatory submissions to accelerate uptake once approvals land.

- Negotiate on total cost of care, not unit price. Winning hospital tenders increasingly requires articulating system-level savings (reduced blood product use, decreased surgical complications). Contracts tied to pathway outcomes or bundled payments can justify premium pricing while protecting hospital budgets.

- M&A and partnership optics. Given the moderate top-tier concentration and technical barriers to entry, 2026 is favorable for strategic bolt-on acquisitions: either to secure plasma collection capacity, expand into complementary hemostatic portfolios, or obtain regulatory footholds in high-value jurisdictions. Partnerships with hospital networks for pilot programs can accelerate adoption while de-risking broader rollouts.

Competitive landscape: profiles to watch

The competitive environment blends global plasma-derived specialists, European blood‑product groups, and regional manufacturers. A few illustrative strategic positions:

- CSL Behring (King of Prussia, PA). As an early entrant with a clinically established fibrinogen concentrate, CSL holds a durable advantage in clinician familiarity and global distribution. Their global plasma-derived portfolio offers cross-leverage for plasma sourcing and regulatory know-how.

- Octapharma AG (Lachen, Switzerland). Octapharma’s strategic moves include broader indication approvals and higher-dose presentations that play directly into hospital workflow optimization. Their product profile emphasizes virus inactivation and supply continuity — attributes that resonate in risk-averse procurement settings.

- Grifols, S.A. (Barcelona, Spain). A recent regulatory win in late 2025 has strengthened Grifols’ U.S. positioning. Their broad plasma capabilities and existing hospital relationships make them a formidable competitor for acute bleeding indications, particularly where HCPCS coding and reimbursement pathways align.

- LFB Group, Shanghai RAAS, and Biotest AG. These regional and European players leverage localized manufacturing, established reconstitution formats, and targeted clinical programs to defend and expand share in specific markets. Their strategies emphasize regulatory breadth and tactical partnerships rather than broad global scale.

Collectively, market leaders exhibit a mix of scale (in plasma supply and distribution), regulatory depth, and product innovation — a combination that will define gatekeepers in key hospital systems through 2026. For challengers, differentiation via faster preparation, targeted clinical evidence, and focused hospital pilot programs remain viable paths to share gains.

Report contents: actionable modules designed for 2026 decisions

Our full PW Consulting report is structured to be directly operational for strategy teams preparing 2026 plans. Key modules include:

- Market sizing and forecast model (2020–2032) with scenario toggles for pricing, uptake, and presentation shifts.

- Detailed segmentation by region, product presentation, and clinical application — with downloadable datasets for investment diligence (note: we do not reproduce these detailed splits here to preserve the integrity of the proprietary models).

- Competitive landscaping with strategic profiles, capability matrices, and M&A target scoring.

- Payer and reimbursement playbooks, including coding implications and hospital contracting templates tied to total cost-of-care metrics.

- Supply-chain risk matrix quantifying plasma sourcing exposure and production bottlenecks with mitigation pathways.

- Commercial playbooks for launch sequencing, field-force sizing, and tender strategies applicable to regional market archetypes.

- Scenario analyses and sensitivity testing for raw-material cost shocks, presentation adoption rates, and regulatory timing shifts.

How PW Consulting can support your 2026 execution

Actions that typically deliver measurable returns in the coming 12–18 months:

- Rapid scenario modeling to quantify the commercial impact of a new presentation or indication, including price-volume tradeoffs and tender outcomes.

- Supply-chain stress-testing and plasma sourcing optimization to reduce raw-material cost exposure and margin variability.

- Targeted due diligence for M&A candidates with a focus on production economics, regulatory pathways, and hospital adoption risk.

- Design and implementation of payer evidence programs that tie clinical outcomes to procurement decision-making and reimbursement flows.

Decisions made in 2026 will lock in capacity allocations, commercial footprints, and R&D prioritization for the better part of the coming decade. The fibrinogen concentrates market offers predictable aggregate growth, but not uniform returns; competitive advantage will accrue to organizations that align product innovation, plasma economics, and payer strategy into a single, executable plan.

Next steps

Download the full PW Consulting market study for the exhaustive datasets, regional and application splits, and interactive financial models that underpin these conclusions. If you are evaluating an entry, an extension, or an M&A opportunity, PW Consulting can rapidly deliver custom valuation models, scenario analyses, and a 90‑day launch readiness program tailored to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Fibrinogen Concentrates Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com