Fresh Meat Packaging Market: Strategic Outlook for 2026 Decision‑Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused strategic brief designed to orient executive teams, investors and supply‑chain leaders making consequential decisions in 2026. This analysis synthesizes a multi‑year market view, regulatory inflection points and competitive dynamics to surface practical actions — while preserving the detailed segment tables and exact regional splits for readers who access the full Fresh Meat Packaging Market report.

Fresh Meat Packaging Market

Market snapshot: growth trajectory and competitive structure

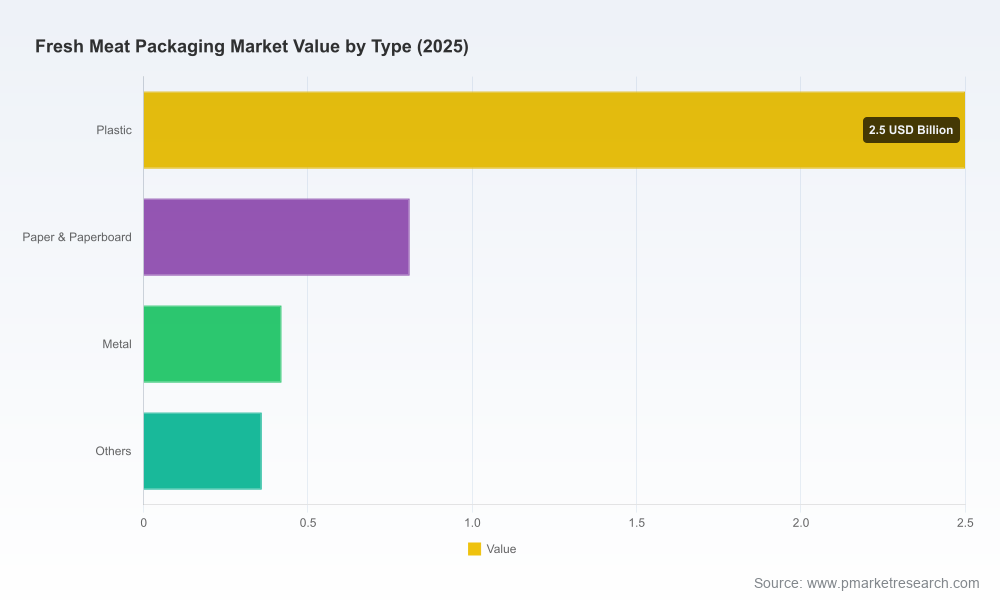

Our market sizing shows a steady expansion of the global fresh meat packaging market, with the industry growing from roughly USD 3.12 Billion in 2020 to USD 4.09 Billion in the base year 2025. Under central assumptions, the market is expected to continue expanding through the forecast horizon (2026–2032), reaching approximately USD 5.79 Billion by 2032. The compound annual growth rate (CAGR) across the forecast window is modeled at 5.12%.

Fresh Meat Packaging Market

Concentration metrics indicate a moderately consolidated supplier landscape: the top three players account for just under half of market value, while the top five approach the low‑fifties percentile. This structure creates predictable advantages for scale players (procurement leverage, distribution reach, and R&D investment), while simultaneously leaving space for agile specialists and new material entrants to capture niche growth.

Fresh Meat Packaging Market

Market dynamics that will determine winners in 2026

- Regulatory acceleration on recyclability and producer responsibility. Emerging Extended Producer Responsibility (EPR) regimes in the U.S. and binding rules under the EU’s Packaging and Packaging Waste Regulation (PPWR) are shifting cost and design incentives upstream. By 2026, producer fees, recycled‑content mandates and design‑for‑recyclability requirements will materially influence material choices and capital planning.

- Raw material pressure and substitution. Limited availability of PET and PE resins — with market impacts that have driven cost increases in the mid‑teens to low‑twenties percent range — is accelerating supplier and buyer interest in paper‑based and recycled polymer alternatives, as well as mono‑material constructions that simplify recycling streams.

- Packaging technology evolution. Vacuum skin packaging, mono‑material films, and fiber‑based tray systems are converging with automation (case‑ready lines, shrink tunnels, heat‑seal membranes) to deliver both shelf‑life extension and sustainability claims. Technology adoption will be a primary determinant of contract wins with major processors and retailers.

- Operational productivity and labor dynamics. Policy changes and processing efficiency initiatives — for example, adjustments to line speeds in select jurisdictions — are changing the total cost calculus for processors. Efficiency gains in slaughter and processing can shift demand profiles for certain packaging formats and automation intensity.

- M&A and strategic partnerships. Given the market’s moderate concentration and technology premium, expect continued deal activity: players seeking scale in high‑growth regions, access to fiber feedstocks, or proprietary film technologies will be active buyers.

What PW Consulting’s full report delivers (practical, decision‑ready assets)

- Executive summary with scenario outcomes tied to regulatory timelines and resin price bands.

- Market sizing and forecasting model (historical 2020–2025, base 2025, forecast 2026–2032) delivered as an interactive Excel workbook and annotated methodology.

- Competitive benchmark: capabilities matrix, product portfolios, go‑to‑market coverage and technology roadmaps for leading suppliers.

- Supply‑chain stress test and procurement playbook (resin risk, alternate suppliers, contract clauses to hedge price volatility).

- Regulatory compliance roadmap (EPR & recycled‑content timelines mapped to product redesign milestones and CapEx triggers).

- Cost‑curve and margin model for common packaging formats that supports pricing and innovation investment decisions.

- M&A target screen and integration checklists — financial and operational red flags tailored to packaging buyers and processors.

- Commercial due‑diligence templates, retailer RFP readiness checklist and sample specification language for recyclable/mono‑material claims.

Note: The public overview intentionally omits granular regional, material and application splits; these are included in the licensed data tables and forecasting model available with the full report.

Competitive landscape: capabilities and recent strategic moves

The competitive map is characterized by global packaging incumbents that combine material science, automation and distribution reach, alongside regional specialists focused on niche formats and service models. Key companies profiled in the report include:

- Amcor plc (Zurich, Switzerland) — global leader in recyclable and mono‑material flexible and rigid solutions for fresh meat.

- Sealed Air Corporation (Charlotte, NC, USA) — specialist in Cryovac vacuum skin technology and integrated equipment solutions.

- Berry Global Group, Inc. (Evansville, IN, USA) — innovation focus on next‑generation vacuum skin and recyclable flexibles.

- Pactiv Evergreen Inc. (Lake Forest, IL, USA) — manufacturer of trays, films and case‑ready systems for processors and retailers.

- Huhtamaki Oyj (Helsinki, Finland) and Mondi plc (Weybridge, UK) — advancing fiber‑based and mono‑material paper solutions.

- Winpak Ltd (Winnipeg, Canada), Sonoco (Hartsville, SC, USA), Coveris (Vienna, Austria) and Edelmann Group (Heidenheim, Germany) — regional and product specialists with targeted investments in sustainability and vacuum technologies.

Selected recent moves underline strategic priorities: Mondi’s partnerships and acquisition activity to secure pulp feedstock and develop recyclable mono‑polypropylene solutions; Coveris’ launch of a recyclable paper‑flexible range and expansion of vacuum skin capacity in the UK; and continued product innovation from several incumbents focused on mono‑material trays and films. These developments affirm the dual market pressures of sustainability compliance and shelf‑life / cost optimization.

Immediate implications for 2026 strategic choices

- Material roadmap and product portfolio prioritization: By mid‑2026, firms should have a prioritized roadmap that sequences transition to recyclable or mono‑material constructions for SKUs exposed to producer fees, while preserving higher‑margin proprietary formats where warranted.

- CapEx targeting and automation: Investments in forming and sealing equipment optimized for vacuum skin and mono‑material films deliver both pack performance and lower end‑of‑life treatment costs. CapEx decisions should be aligned to regulatory milestone dates to avoid stranded assets.

- Procurement and supply‑risk mitigation: Locking multi‑year agreements with diverse resin suppliers, expanding recycled content sourcing, and developing fiber feedstock partnerships will reduce exposure to upstream cost shocks.

- Commercial alignment with retailers and processors: Co‑develop sustainability claims and shelf‑life performance metrics with key customers to secure premium listings and avoid chargebacks under EPR schemes.

- M&A and partnership playbook: Prioritize targets that provide either feedstock security (pulp, r‑PET), differentiated film technologies, or geographic footholds in fast‑growing processing clusters.

- Scenario planning and pricing discipline: Build price‑pass frameworks that reflect resin volatility bands and regulatory fee phases, while keeping an innovation cushion for new pack claims.

Risk watchlist for board and executive briefings

- Regulatory timing risk — implementation delays or accelerated timetables for EPR and recycled‑content mandates will affect redesign timelines and cash flow.

- Raw material shocks — sustained PET/PE scarcity could pressure margins and force faster migration to alternatives.

- Technology execution risk — scaling mono‑material or paper‑based solutions without compromising seal integrity, barrier performance, and shelf‑life.

- Market access and claims compliance — inconsistent national recyclability standards and retailer verification requirements can limit claims portability.

- Consolidation and competitive displacement — targeted roll‑up activity among regional specialists could alter supplier leverage dynamics.

How PW Consulting helps: data, execution and assurance

For leadership teams evaluating product, sourcing or M&A choices in 2026, the combination of a robust forecasting model, a regulatory calendar mapped to product roadmaps, and competitor technical profiles is indispensable. Our full report packages the quantitative models, supplier scorecards and tactical playbooks needed to convert strategy into executable plans — including sensitivity analyses that show when to accelerate investment versus when to adopt a wait‑and‑watch posture.

To preserve competitive integrity for early adopters, this public brief omits granular regional and application splits; those datasets, alongside scenario‑specific P&L impacts and supplier‑level margins, are available in the licensed report. Contact PW Consulting to obtain the complete market model, competitor dossiers and a tailored 90‑day action plan that aligns packaging investments to your 2026 growth and sustainability targets.

For detailed analysis of this topic, please visit the official page:Fresh Meat Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com