Serums For Skincare Hydration And Advanced Skin Care Routines

Other |

2026-05-29 16:53:49

This briefing frames the strategic value of PW Consulting’s full Dimethyl Carbonate (DMC) Market study for executives making resource-allocation, capacity, and commercial decisions in 2026. It highlights the macro trajectory, structural dynamics, competitive posture, and the practical actions that leaders — producers, battery manufacturers, chemical distributors, investors and policy teams — must prioritize this year. Per our “trailer” principle, we demonstrate the analytical depth and the types of insights included in the report while intentionally withholding the granular segment-level tables and proprietary split data to encourage access to the full study.

Dimethyl Carbonate (DMC) Market

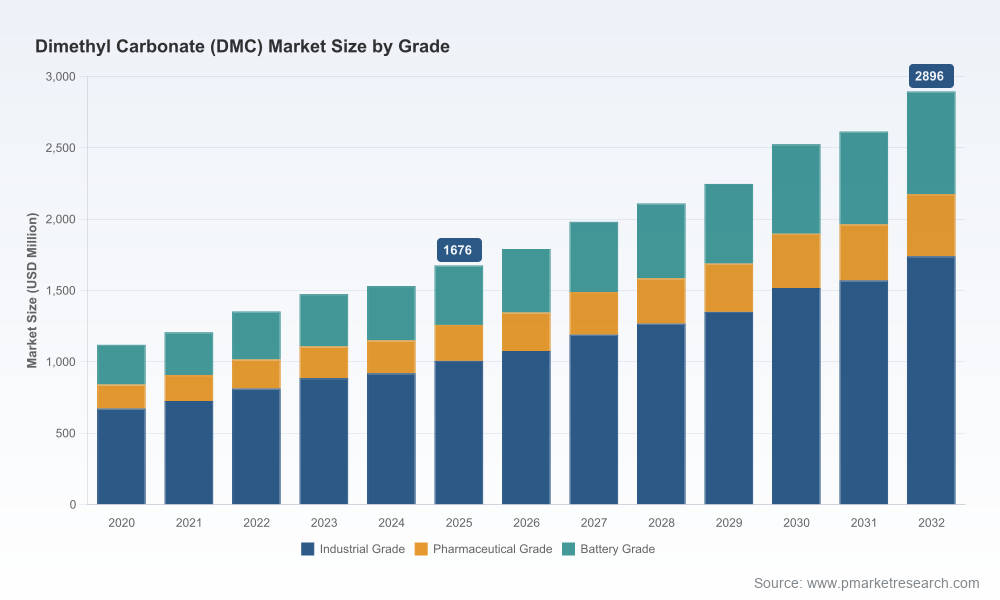

DMC has shifted in 2020–2025 from a modest specialty chemical to a strategic intermediate with cross-industry demand. The market expanded from roughly USD 1,120 Million in 2020 to USD 1,676 Million in 2025 (base year), reflecting accelerating adoption across battery electrolytes, polycarbonate synthesis and specialty solvent applications. Our forecast period (2026–2032) assumes a compound annual growth rate of 8.1%, taking the market to roughly USD 2,896 Million by 2032 under the base case.

Dimethyl Carbonate (DMC) Market

Two structural facts matter for planning in 2026: first, the market is growing at a pace that justifies new upstream investments and product-differentiation strategies; second, market concentration remains low-to-moderate (top-three and top-five shares are modest), indicating an industry where scale helps but where nimble, differentiated plays can still capture value. That fragmentation creates distinct tactical opportunities — and execution risks — for players across the value chain.

Dimethyl Carbonate (DMC) Market

Feedstock volatility and margin pressure — Methanol is a primary upstream input for many commercial DMC routes. In early‑2026 methanol spot prices rose sharply (with China figures moving above the USD 400/MT range amid geopolitical and supply disruptions), and Northeast/South Asia FOB differentials widened materially. These swings convert directly into cost-of-goods variability for DMC producers and change the economics of long-lead capacity projects. Our report includes forward-looking feedstock scenarios and playbooks for margin protection.

Policy and regulatory tailwinds — Regulatory agencies are increasingly recognising DMC as a lower-toxicity alternative to traditional solvents. Recent actions in 2025–2026 (including targeted customs classifications and environmental guidance) are accelerating interest from formulators seeking compliant solvent systems. This creates demand optionality — particularly for high-purity, low-impurity grades required by pharmaceutical and battery customers.

Electrification and battery chemistry dynamics — Battery-grade DMC demand is growing as lithium‑ion electrolyte formulators seek cost‑competitive carbonate co-solvents. Producers that can guarantee battery-spec purity and continuity of supply are capturing disproportionate margin; conversely, suppliers exposed to feedstock swings without grade-certification capability face pricing and contractual risk.

Capacity projects and geography — New capacity announcements and partnerships are already reshaping regional supply balances. High‑visibility moves announced in late‑2025 and early‑2026 signal that strategic producers are positioning close to battery OEM hubs and premium end markets to shorten lead times and de‑risk logistics.

The competitive field combines multinational specialty players, integrated petrochemicals groups, and regional Chinese producers. Several company archetypes emerge:

Large multinational integrators — Companies with global footprint and multiple production routes can flex feedstock sourcing, qualify multiple grades rapidly, and supply battery and pharma customers. Their advantage is supply security and the ability to underwrite capital-intensive projects in strategic regions.

Regional cost leaders — Producers leveraging oxidative carbonylation at scale in regions with competitive methanol or integrated upstream chains often compete on price for industrial-grade demand. These firms play a vital role in balancing global spot markets and act as liquidity providers.

Specialist high‑purity suppliers — Firms focused on transesterification or post‑treatment for ultra‑low impurity grades cater to pharmaceutical, laboratory and battery electrolytes. Their prowess is in process control, certification and traceability — attributes that command premiums with OEMs and formulators.

Representative players and strategic notes (non‑exhaustive):

Producers investing in North American capacity to serve lithium-ion and semiconductor ecosystems are taking a deliberate demand‑capture approach. A recent greenfield in Louisiana (announced in early 2026) illustrates this model: sizable DMC and EMC capacity is being developed specifically to serve regional battery and specialty demand — a strategic move to reduce lead times and customs friction.

Korean and Japanese specialty houses continue to emphasize grade diversification, leveraging legacy technologies and distribution channels to sell both industrial and battery-grade materials to global customers.

Large Chinese chemical groups remain important swing suppliers: their scale provides volume optionality but also exposes them to feedstock price cycles and regional policy changes. Partnership announcements in 2025 that pair local producers with international technology licensors signal a pivot toward higher-purity, battery-focused production in China.

We model three actionable scenarios to inform 2026 decisions: base, upside (accelerated EV/battery demand) and stress (feedstock shock + regulatory constraints). Each suggests distinct near-term moves.

Base case (CAGR ~8.1%) — Priorities: rationalize expansion timelines, secure off‑take with battery and polycarbonate customers, and phase investments with milestone-linked capex to preserve optionality.

Upside case (faster electrification) — Priorities: accelerate battery‑grade qualification programs, co‑locate or partner with electrolyte makers, and pre‑negotiate long‑term tolling or partial‑take contracts to capture upside and avoid spot-market squeezes.

Stress case (methanol spike / trade disruptions) — Priorities: implement feedstock hedging or vertical integration, increase short-term inventory buffers for critical customers, and stress-test contractual terms for force majeure and price pass-through clauses.

Across scenarios, practical 90–180 day actions we recommend for executives in 2026 include:

The full report is structured to move readers from insight to execution. Highlights include:

Note: to preserve competitive advantage for subscribers and avoid replicating confidential data in a public briefing, the report does not release our full segment-by-segment tables in this summary. Those granular splits, supplier‑level volumes and contract‑level assumptions are available in the subscriber download and are essential for transaction-level underwriting.

Decision-makers face a narrow window in 2026 to lock in supply, secure premium-grade capacity, and hedge feedstock exposure before the next wave of capacity comes online and before further regulatory and trade shifts crystallize. The DMC market’s healthy near-term growth rate and the ongoing electrification of mobility create a durable demand base, but execution risk — around feedstock prices, certification timelines for battery‑grade materials, and regional trade friction — will determine winners and losers.

PW Consulting’s DMC Market study converts these macro and micro dynamics into commercial actions: where to place capacity, how to contract smarter, when to accelerate qualification, and which partner archetypes to pursue. Access to the full report provides the granular inputs and templates needed to execute with confidence in 2026.

For the complete dataset, segmentation tables, supplier-level profiles and execution templates, please consult the full PW Consulting DMC Market report available on our website.

For detailed analysis of this topic, please visit the official page:Dimethyl Carbonate (DMC) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com