Intelligent Parcel Locker Market — Strategic Preview for 2026 Decision Makers

As organizations recalibrate last-mile logistics, property services, and e‑commerce delivery strategies for the post‑pandemic era, intelligent parcel lockers have moved from a tactical convenience to a strategic infrastructure asset. PW Consulting’s latest market study — the Intelligent Parcel Locker Market (base year 2025; historical 2020–2025; forecast 2026–2032) — frames the sector’s trajectory and delivers the pragmatic intelligence leaders need to make high‑stakes choices in 2026. Key macro takeaways: the global market surpassed USD 1.2 billion in 2025 and is expected to grow at a compound annual growth rate (CAGR) of approximately 12.5% over the forecast window, reaching well into the multi‑billion dollar range by 2032. The market is meaningfully fragmented (CR3 ≈ 25%; CR5 ≈ 35%), leaving room for regional champions, niche specialists, and integrators.

Intelligent Parcel Locker Market

Why this report matters for 2026 strategy

- Investment timing: 2026 represents an inflection point where pilots must scale into repeatable deployments. Capital allocation decisions taken this year will determine which operators capture enduring operational leverage.

- Procurement cycles: Public transport authorities, multi‑family housing managers, and large retailers are consolidating locker procurement into multi‑year programs. Delivering the right vendor selection framework in 2026 shortens time to revenue and reduces retrofit costs.

- Integration imperative: Locker hardware is increasingly a node in a broader digital ecosystem (TMS, WMS, carrier APIs, building management). The strategic priority in 2026 is choosing platforms that minimize lock‑in while enabling rapid feature rollouts.

Market dynamics shaping decisions

- Automation reduces last‑mile labor cost: Parcel locker adoption lowers repetitive doorstep stops, enabling carriers and postal operators to rebalance routing and labor allocation. This dynamic has immediate P&L implications for delivery networks and municipal operators alike.

- Urban logistics and infrastructure economics: Smart lockers reduce curbside dwell time and vehicle miles in dense corridors. For cities and property owners prioritizing congestion and emissions reductions, lockers are an economic lever as much as a convenience feature.

- Regulation and data sovereignty: European regulatory developments (including expanded universal service approaches and stricter data handling rules) are shaping both procurement specifications and technical architectures. Expect contracts to demand local data residency, audit trails, and certifiable privacy controls.

- Connectivity and IoT enablement: Advances in low‑power wide‑area networking, and permissive spectrum/regulatory regimes for IoT, make real‑time status, telemetry and remote diagnostics standard‑issue capabilities — changing O&M cost models.

- Product differentiation via modularity and functionality: From refrigerated lockers for fresh food to solar‑powered and off‑grid installations, suppliers are expanding beyond commodity metal boxes to deliver verticalized solutions that solve specific operating problems.

- Consolidation pressure: With moderate concentration metrics, we expect a mix of targeted M&A (to acquire route networks, software IP, or regional footprint) and partnerships between hardware‑centric vendors and platform/software players.

Competitive landscape — who wins and why

The competitive field blends hardware manufacturers, software platform providers, postal incumbents, and agile new entrants. Each archetype pursues a distinct route to value:

Intelligent Parcel Locker Market

- Network and software‑first players: Companies that prioritize carrier‑agnostic networks and a software management layer can scale quickly across property portfolios and carriers. Their value proposition is convenience for end users plus low friction for carriers.

- Hardware innovators: Suppliers investing in modularity, IP protection for outdoor use, off‑grid power (including solar), and thermal management (refrigeration/cooling) are winning contracts where site constraints or unique use cases exist.

- Postal partnerships and operator exclusives: Vendors that secure preferential relationships with national postal operators or large couriers often gain rapid nationwide footprint through existing delivery networks and property relationships.

Representative examples from the market illustrate these archetypes and tactical moves:

Intelligent Parcel Locker Market

- ZHILAI (China): Positions itself with a broad product portfolio that includes solar‑powered and refrigerated models. Its emphasis on hardware breadth and last‑mile adaptability targets integrators and logistics providers needing tailored site solutions.

- Quadient / Parcel Pending (France/Global): Focuses on software‑driven scale — an open, carrier‑agnostic network model combined with deployment experience across residential, retail and transport nodes. Their recent large‑scale deployments with rail operators and carriers illustrate a network playbook that prioritizes reach and interoperability.

- OMNIC (Europe): Competes on ruggedized indoor/outdoor designs with IP54 options and off‑grid capabilities — appealing to logistics players deploying in varied environmental and infrastructure settings.

- KEBA (Austria): Leverages partnerships with postal operators and parcel networks to secure supplier exclusivity in certain markets, demonstrating the value of channel relationships for rapid penetration.

- Postal Source (United States): Focuses on secure parcel management and operator workflows — a fit for mid‑market commercial and institutional buyers that prioritize operational simplicity.

Near‑term M&A and partnership activity (observed in the last 12–24 months) underscores two strategic patterns: consolidation to secure geographic scale and capability acquisitions to add software, thermal or power innovations. Notable moves in 2025 — network expansions, operator supplier selections, and acquisitions by prominent locker network operators — are consistent with the market’s move from proof‑of‑concept to networked infrastructure.

What the PW Consulting report delivers (practical, operational, and commercial)

We designed the study to be a decision‑support toolkit, not a textbook. The full report (and its associated appendices and downloadable assets) contains:

- Detailed market sizing and validated forecast models (2020–2032) with scenario analysis and sensitivity to key drivers such as e‑commerce penetration, urbanization rate, and average parcel size.

- Vendor scorecards and procurement templates: RFP language, technical checklists, security/cyber requirements, and SLAs tailored to operator, retail and residential use cases.

- Deployment playbooks: site‑selection criteria, O&M plans, remote monitoring configurations, installation phasing and cost models for retrofit vs new build.

- Commercial modeling tools: discounted cash flow templates, TCO comparisons across ownership and as‑a‑service models, and decision matrices for purchase vs lease vs managed service.

- Technology and integration guidance: API reference patterns, recommended connectivity stacks (including considerations for NB‑IoT/LTE‑M/Wi‑Fi), and edge vs cloud processing tradeoffs under various data sovereignty regimes.

- Regulatory and compliance playbook: checklist for EU data residency, telecom spectrum considerations for wireless telemetry, and procurement clauses to mitigate regulatory risk.

- Value chain and partner maps: channel strategies for integrators, carrier onboarding playbooks, and real‑world case studies of rail, retail, multifamily and campus deployments.

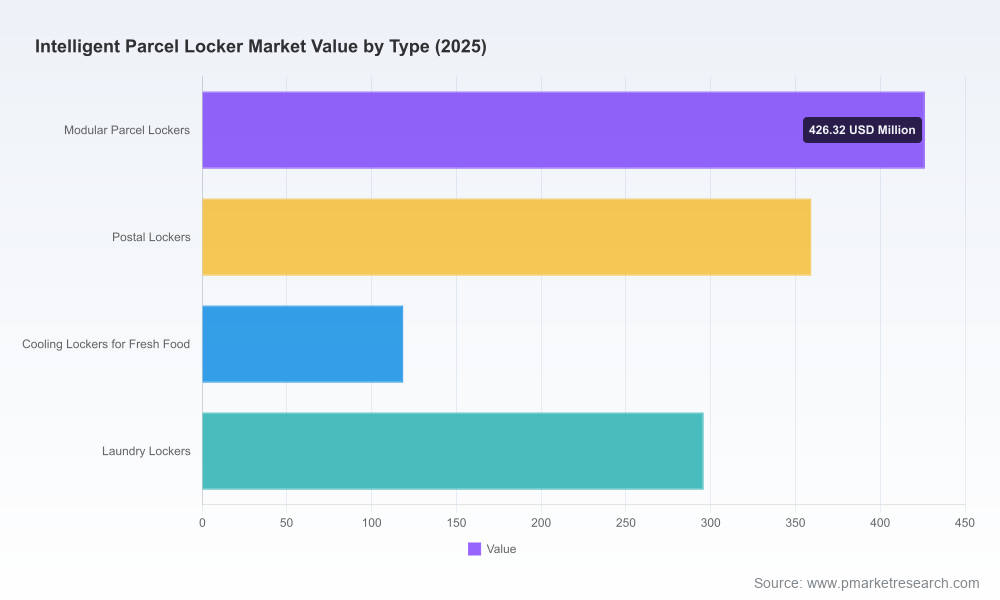

To preserve the tactical value of the study for licensed users, segmented line‑item tables (regional, type and application splits at annual granularity) are intentionally omitted from this preview; those datasets and vendor benchmarking matrices are available through the full report package.

Actionable recommendations for executives in 2026

- Adopt a two‑track rollout approach: Accelerate high‑impact pilots (transit hubs, dense multifamily, BOPIS retail) while negotiating scalable master service agreements for broader rollouts. Use time‑boxed pilots to validate O&M and customer experience assumptions.

- Prioritize interoperability: Require open APIs and carrier‑agnostic operational models to avoid future migration costs and to enable rapid partner onboarding.

- Make sustainability a procurement criterion: Favor systems with efficient power profiles, options for off‑grid / solar operation, and lifecycle recycling plans — both to reduce operating expense and to satisfy emerging ESG procurement standards.

- Embed regulatory and data controls in contracts: Specify data residency, encryption standards, and audit rights up front to prevent compliance surprises in cross‑border deployments.

- Use modularity to manage site variability: Select hardware that supports common base modules and optional thermal or power extensions to reduce SKU complexity and spare‑part overhead.

- Design for operational telemetry: Implement remote diagnostics and predictive maintenance from day one to minimize downtime and unit replacement costs.

Conclusion — the strategic opportunity

Intelligent parcel lockers are no longer peripheral conveniences; they are distributed infrastructure nodes that affect carrier economics, urban logistics, and consumer experience. The market’s strong growth trajectory (CAGR ~12.5% from the 2025 base), combined with fragmented supplier economics, creates a window in 2026 for bold, interoperable strategies that can capture lasting competitive advantage. Whether your objective is to reduce last‑mile costs, enhance property value, or build a resilient omnichannel delivery footprint, the right combination of product, partner and deployment model will decide winners in the next decade.

PW Consulting’s full Intelligent Parcel Locker Market report contains the data tables, vendor scores, procurement artifacts and deployment models that enable confident execution. Detailed segmented data and annualized breakdowns have been reserved for the full report; contact PW Consulting or visit our report page to access the complete intelligence package and the modeling tools that accompany it.

For detailed analysis of this topic, please visit the official page:Intelligent Parcel Locker Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com