Malaysia Elderly Care Market Insights and Growth Trends

Other |

2026-06-08 02:20:26

As enterprises plan product roadmaps, supply-chain commitments and M&A activity for 2026, the PC power supply market offers a mix of steady expansion, technology-driven churn and supply-side risk. Our analysis — anchored to a 2025 base year, with a 2020–2025 historical window and a 2026–2032 forecast horizon — shows a reliably growing market driven by higher-power desktop/workstation requirements, the formalization of ATX 3.1 and PCIe 5.x power interfaces, and regulatory tightening on no-load and efficiency metrics. The market has expanded materially over the last half-decade and is projected to continue doing so at a mid-single-digit compound annual growth rate (CAGR) through the early 2030s, supporting both incumbent ecosystem plays and specialist entrants focused on high-efficiency, high-wattage, modular solutions.

PC Power Supply Market

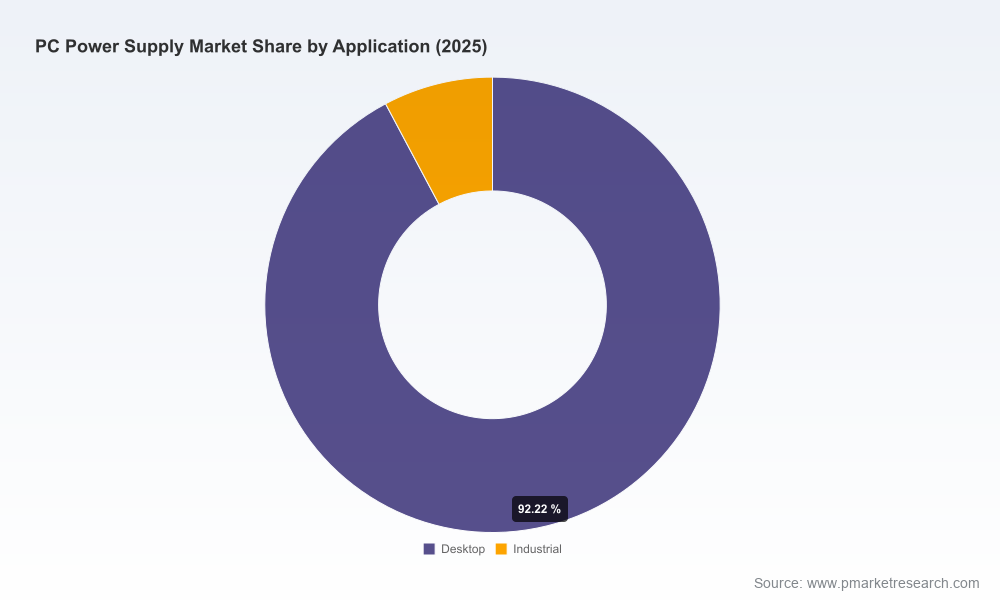

Measured on a consistent USD (Million) basis, the PC power supply market grew from a lower base in 2020 to a substantially larger industry by 2025. From that 2025 base, our forecast to 2032 shows steady expansion underpinned by a roughly 4.9% CAGR, yielding a sizable increase in absolute market value by the end of the forecast window. This trajectory reflects two parallel dynamics: increasing per-unit power and complexity for high-end consumer and workstation systems, and a widening set of enterprise-grade applications that expect server- and AI-capable power delivery inside small-form-factor or on-premise systems.

PC Power Supply Market

Market concentration remains meaningful but far from monopolistic: the top-three and top-five players account for a clear minority share, leaving significant addressable space for differentiated product strategies, OEM partnerships and regional OEM/ODM wins. For leaders and challengers alike, that concentration profile creates both opportunity — the ability to scale quickly once a technical or channel advantage is secured — and risk, where supply constraints or regulatory missteps can amplify share movements.

PC Power Supply Market

Standards and product design: The ATX 3.1 specification, introduced in 2023, and the industry move toward PCIe 5.x power interfaces materially alter PSU design imperatives — faster transient support, revised connector topologies and shorter hold-up tolerance. Product teams must integrate those electrical and mechanical constraints now to avoid late-stage redesigns.

Regulatory tightening: Ecodesign updates in Europe and California Title 20 changes are accelerating adoption of digital control loops and synchronous rectification. Compliance is becoming a product differentiator, not just a cost of entry.

Commodity and component pressure: Passive component indices and specific inputs such as ferrite cores have shown recent, material price volatility. A higher input-price baseline and episodic spikes in 2024–2025 have forced manufacturers to re-evaluate procurement strategies and bill-of-materials (BOM) design choices.

Workload-driven demand: AI-focused desktop workstation builds and on-premise appliances require higher continuous and transient power, opening a premium segment for PSUs that combine efficiency, thermal headroom and PCIe 5.x readiness.

For executives setting budgets and targets in 2026, three imperatives should guide capital allocation and commercial planning:

Product roadmap certainty: Prioritize ATX 3.1 and PCIe 5.x compliance across new SKUs and ensure digital control topologies are included in next-generation designs. Systems that can demonstrate compliance with new hold-up and transient requirements command a premium in gaming and workstation markets.

Supply-chain resilience and cost management: Move from transactional sourcing to strategic supplier partnerships for critical passives (ferrites, high-grade capacitors) and consider forward contracts or hedging where index exposure is material. Dual-sourcing and geographic diversification of subassembly capacity will mitigate episodic shocks.

Channel & aftermarket strategy: With market concentration leaving room for nimble entrants, differentiate through bundled software (fan and power telemetry), warranty/return policies and OEM co-development deals tailored for AI or ultra-quiet gaming segments.

The PC power supply vendor set is composed of established OEM/ODM manufacturers, premium branded suppliers and specialist boutique players. Across that field, several strategic archetypes are visible:

Premium brand-differentiators: Companies focused on flagship efficiency and quiet operation — offering Titanium/Platinum level units with full modularity — retain strong pricing power in the high-end gaming and workstation verticals. Their strength is brand equity, high-margin SKUs and rapid new-standard adoption.

Volume OEMs/ODM platforms: Large manufacturers with broad portfolios and high-wattage modules serve both consumer and commercial channels. Their ability to leverage scale and supply relationships positions them well for enterprise OEM contracts and commercial partnerships that require higher reliability and redundancy features.

Niche innovators: Smaller firms and specialist product lines compete on form factor (SFX), ultra-quiet acoustics or unique modular ecosystems. These players can capture premium niches or become acquisition targets for larger OEMs seeking technology or channel fill.

Recent product activity and trade-show presence illustrates where tactical advantage is emerging: several leading suppliers have launched or showcased ATX 3.1- and PCIe 5.x-ready units — including 2000W-class high-wattage flagships and ultra-quiet modular series — signalling that technical differentiation will be decided at the product performance and ecosystem-integration levels. For M&A teams, that makes late-stage startups with platform IP and unique cooling or telemetry features attractive targets. For product and engineering teams, it means accelerating validation cycles for hold-up time and transient response.

Design-to-cost and modular BOMs: Redesigning for fewer costly passive components while maintaining electromagnetic compatibility and thermal performance reduces exposure to commodity spikes.

Strategic inventory and capacity commitments: Early 2026 procurement steps — including strategic safety-stock positions for ferrites and high-spec capacitors — will smooth pricing and delivery across cyclical demand swings.

Compliance-by-design: Embedding power telemetry and software-controlled idle states facilitates adherence to no-load efficiency requirements while creating a route for value-added services and extended warranties.

Channel segmentation: Differentiate go-to-market motions for high-margin, tech-centric buyers (gaming/workstation) vs. enterprise/OEM channels (redundancy, service agreements, CRPS compatibility).

The full PW Consulting study — built on a 2025 base and extending forecasts through 2032 — provides the operational playbook required to convert insight into 2026 action. Key deliverables include:

A transparent market-sizing and forecast model (USD, Million) with scenario sensitivity to commodity-price and regulatory regimes;

A multi-layered supply-chain map identifying single-source exposures and Tier-1/Tier-2 risk nodes for critical passive components;

Technical checklists and test protocols addressing ATX 3.1 hold-up, PCIe 5.x power delivery, no-load efficiency, and digital-control integration;

Competitive benchmarking that synthesizes product roadmaps, channel footprints and recent product launches to prioritize acquisition and partnership targets;

Commercial playbooks for price-setting, channel incentive design and aftermarket service monetization tailored to 2026 market dynamics.

Executives should treat the findings here as a strategic filter: use the macro forecast and market-structure insights to set investment envelopes for R&D, capex and M&A; apply the operational levers to immediate procurement and product-scope decisions; and deploy the competitive and regulatory intelligence to refine go-to-market sequencing for 2026 product launches. Short-term moves that materially reduce exposure to passive-component volatility and accelerate ATX 3.1/PCIe 5.x compliance will yield outsized returns if demand continues along the central forecast path.

This briefing highlights the strategic contours and operational implications necessary for high-quality 2026 decision-making. To maintain the integrity of our segmentation and forecast granularity — and to support targeted commercial action — core disaggregated segment data, regional splits and SKU-level forecasts are reserved for the full report and model package. Access to the complete dataset and the interactive forecast tool is available through PW Consulting; the full deliverable includes downloadable models, test protocols and a prioritized action checklist tailored to your organization’s risk profile.

For detailed analysis of this topic, please visit the official page:PC Power Supply Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com