Breaking: The Automotive Fastening Assembly Equipment Market on a Rapid Growth Trajectory

Other |

2026-05-18 09:56:59

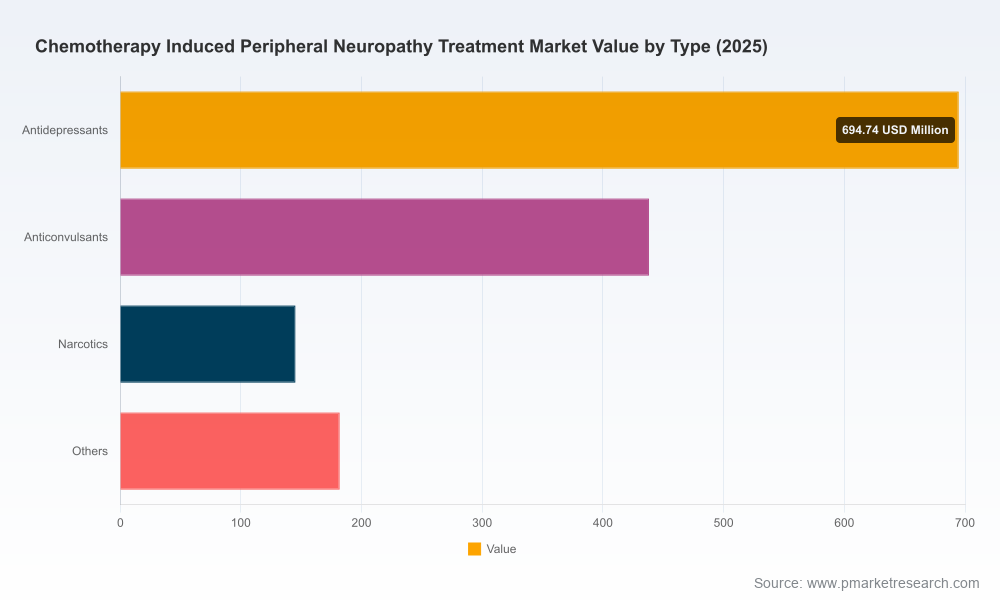

As oncology care continues to extend survival across multiple tumor types, the clinical and economic burden of chemotherapy‑induced peripheral neuropathy (CIPN) has moved from an under‑recognized complication to a boardroom issue. PW Consulting’s latest market study — with base year 2025 and a detailed 2026–2032 forecast horizon — synthesizes clinical, regulatory and commercial vectors that will determine winners and losers in the CIPN treatment space. The overall market expanded steadily from 2020 to 2025, reaching an estimated USD 1,460 Million in 2025, and our scenario frameworks project continued growth at a compound annual growth rate of approximately 6.5% through the forecast window. This preview explains why the study matters for 2026 decisions, what practical intelligence it delivers, and how executive teams should mobilize resources in response.

Chemotherapy Induced Peripheral Neuropathy Treatment Market

Inflection in clinical readouts and regulatory clarity: 2025–2026 has produced a distinct acceleration in activity — from an FDA draft guidance on CIPN development issued in January 2025 to multiple late‑stage and regulatory‑designated programs in 2026. These events compress decision timetables: assets with Phase 2b/Phase 3 momentum are now front‑of‑mind for partners, acquirers and payers.

Chemotherapy Induced Peripheral Neuropathy Treatment Market

Market scale and predictable expansion: an established base market in 2025 provides a reliable foundation for investment decisions. With our modeled CAGR of ~6.5% across 2026–2032, boards can plan multi‑year return horizons while stress‑testing outcomes against clinical trial success or failure scenarios.

Chemotherapy Induced Peripheral Neuropathy Treatment Market

Consolidation pressure and opportunity windows: the market shows a moderate level of concentration, with the top three and top five companies accounting for a meaningful share of commercial influence. That concentration translates to both acquisition targets and competitive barriers that must be anticipated in licensing and pricing negotiations.

Market sizing & forecast engine: base year 2025 calibration, historical time series, and probability‑weighted projections across 2026–2032. Models are delivered in a format that allows clients to swap clinical success probabilities and alternative pricing assumptions to test downside and upside pathways.

Clinical & regulatory tracker: live‑timeline mapping of ongoing trials, regulatory milestones, designations and guidance. This module highlights readout windows, enrollment status and regulatory events that materially affect commercial timelines.

Competitive intelligence packs: disciplined profiles of active and near‑market developers (mechanism of action, development stage, strategic dependencies, partnership history and commercialization readiness). These profiles are annotated with our assessment of strategic options for partnering, co‑development or acquisition.

Payer & access playbook: reimbursement archetypes, HTA trigger points, and differentiated evidence requirements for launch. The playbook covers contracting tactics, outcomes‑based constructs and early value dossiers aimed at oncology and neurology payer audiences.

Go‑to‑market and commercial readiness templates: channel mapping, KOL engagement blueprints, patient journey analytics, and a stepwise launch framework for staggered regional rollouts.

Deal and valuation tools: pricing scenarios, revenue waterfall templates, and deal comparators to support licensing, minority investments and M&A deliberations.

Risk matrix and mitigation roadmap: clinical, regulatory, manufacturing and market adoption risks with prioritized mitigations and contingency thresholds tied to cash‑flow and capital need triggers.

The current pipeline is heterogeneous in mechanism and developer profile, creating a mosaic of strategic choices rather than a single dominant pathway. Recent and high‑impact developments include:

Dogwood Therapeutics: advancing a Nav1.7 inhibitor (Halneuron) with positive interim Phase 2b signals and over 50% enrollment achieved in a pivotal study. Dogwood has also licensed a biologic candidate (SP16) from an innovation partner and is positioned to run a Phase 1b enrollment starting mid‑2026. Strategically, Dogwood represents a company with both near‑term pivotal readouts and a diversification of modality exposure.

Serpin Pharma: achieved FDA IND clearance for SP16 and secured external grant funding to support early clinical development. Their position as an innovator with a clinically validated path to human proof‑of‑concept makes them an attractive partner for later‑stage developers seeking complementary assets.

Sironax: an emerging entrant with a SARM1 allosteric inhibitor granted FDA Fast Track designation. Regulatory acceleration through Fast Track can materially shorten the path to broader development engagement and increase transaction interest.

Asahi Kasei Pharma: initiated a Phase 3 prevention study of a biologic therapy in a country‑specific program. A late‑stage prevention program introduces a different commercial calculus (prophylaxis vs symptom management) that incumbent and new entrants must factor into product positioning and evidence generation strategies.

WinSanTor and AlgoTherapeutix: represent topical approaches with varying development momentum—these programs underscore the diversity of formulation and delivery strategies being explored, and they signal the need for differentiated clinical endpoints and market access narratives.

Collectively, these developments create a dynamic where strategic partners and potential acquirers will be discriminating on three axes: evidence quality (robust clinical endpoints and responder analyses), regulatory positioning (designations and alignment with the FDA’s draft guidance) and commercial defensibility (pricing, indication breadth and payer acceptability).

Reprioritize R&D roadmaps around near‑term readouts. If your portfolio includes assets with Phase 2b/3 potential, increase investment in endpoint optimization, statistical robustness and subpopulation analyses now — not later. A positive top‑line in the next 12–18 months will materially revalue development programs.

Engage regulators early and often. The FDA’s 2025 draft guidance has clarified expectations; sponsors should adopt an engagement plan focused on trial design alignment, endpoint validation and patient‑reported outcomes to reduce regulatory execution risk.

Calibrate partnering and M&A frameworks to market concentration dynamics. Given the current concentration among a handful of players, strategic combinations and licensing deals will shape access to commercial channels. Prepare tiered offer strategies that reflect clinical milestone achievement.

Build payer evidence in parallel with clinical development. Payer conversations should start in Phase 2 with well‑crafted HEOR endpoints and early real‑world evidence (RWE) plans to support reimbursement negotiations post‑launch.

Differentiate by mechanism and indication. Prevention vs symptomatic treatment, systemic vs topical modalities, and neuroprotective vs neurorestorative mechanisms will command different market access and pricing strategies. Investors should value platform versatility.

Create contingency playbooks. Run stress tests on cash runway, enrollment delays and negative readouts, and define pre‑negotiated cost containment and asset rationalization actions to preserve optionality.

Our report is designed for immediacy: quantitative models that are plug‑and‑play for corporate finance teams, regulatory trackers that feed into program roadmaps, and commercial playbooks that can be operationalized by the end of Q3 2026. Clients receive scenario dashboards that let them answer questions such as: “If Halneuron achieves its expected Phase 2b outcome, what is the implied revenue uplift under conservative payer uptake assumptions?” or “What premium should we offer in a licensing term sheet to secure first negotiation rights on a promising Phase 1 candidate?”

Importantly, while this preview presents the strategic architecture and headline market trajectory, core segmented intelligence — including granular regional and application‑level splits, detailed product‑level revenue waterfalls, and actionable company valuation matrices — is intentionally reserved for the full report to protect client value and to support informed, confidential decision‑making.

2026 will be a pivotal year for CIPN therapeutics. The combination of clearer regulatory expectations, a growing pipeline that spans small molecules, biologics and topicals, and imminent trial readouts creates compression across development and commercial timelines. Boards, R&D leaders and corporate development teams must move from passive monitoring to proactive positioning: aligning evidence plans with payer expectations, sharpening partnering proposals, and preparing for accelerated commercialization pathways. PW Consulting’s full study provides the calibrated models, regulatory intelligence and commercial playbooks needed to turn these strategic imperatives into executable plans.

For executives preparing capital allocation and partnership strategies in 2026, accessing the complete report and interactive toolset will convert the market’s macro trends and clinical newsflow into confident, defensible decisions.

For detailed analysis of this topic, please visit the official page:Chemotherapy Induced Peripheral Neuropathy Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com