Industrial Cable Storage Market to Reach $3.55 Billion by 2035

Other |

2026-06-18 08:55:07

As companies, regulators and laboratory networks move into 2026, the demand for high-fidelity mercury measurement and continuous monitoring is becoming a defining axis of environmental compliance and quality assurance strategy. PW Consulting’s Mercury Analyzer Market — Mercury Analyzer Market (base year 2025; forecast 2026–2032) — provides the structured intelligence to convert regulatory change and technological evolution into actionable decisions. Our analysis synthesizes historical performance, a probabilistic forecast (2026–2032) and a practical playbook for procurement, R&D prioritization and commercial deployment.

Mercury Analyzer Market

At a macro level the market shows steady expansion: after a measured recovery through 2020–2025, our forecast path to 2032 is underpinned by a compound annual growth rate (CAGR) of 6.58%. That trajectory reflects a blend of regulatory enforcement, replacement cycles in regulated industries, and growing adoption of real‑time and portable measurement solutions by private and public sector buyers.

Mercury Analyzer Market

Compliance momentum is uneven but real: Regulatory tightening in some regions (including recent revisions to industrial emissions regimes and ongoing Minamata Convention implementation) is expanding demand for continuous emissions monitoring systems (CEMS) and ultra‑trace laboratory analyzers. At the same time, deregulatory moves in other jurisdictions create a multi-speed market that requires scenario planning.

Mercury Analyzer Market

Procurement risk management: With instrument lifecycles and aftermarket services representing a significant portion of total cost of ownership, procurement teams need forward-looking TCO models and vendor‑service bundling options, not just unit price comparisons.

R&D and product roadmap alignment: Manufacturers and corporate R&D organizations must decide whether to prioritize ultra-trace sensitivity, portability, automation, or connectivity. Our report quantifies the tradeoffs and includes a technology roadmap to inform CapEx decisions across short, medium and long horizons.

M&A and partnership screen: Market concentration metrics show meaningful dominance by a small set of global players — a structural dynamic that shapes valuation multiples, potential consolidation targets and white‑space opportunities for niche specialists.

Transparent market sizing and forecast: End‑to‑end revenue modeling from 2020 to 2032 with base‑case, upside and downside scenarios driven by regulatory, industrial and technological levers.

Methodology and data sources: Detailed description of primary interviews, vendor validation, public contracts and regulatory signals used to build the forecast — enabling reproducibility and auditability for internal stakeholders.

Buyer and use‑case playbooks: Procurement templates, evaluation checklists and TCO models for environmental labs, incineration and utilities, pharmaceuticals and oil & gas customers.

Vendor scorecards and go‑to‑market maps: Comparative assessments of technology fit, service footprint, regulatory certifications and aftermarket economics for the leading instrument providers. (Note: detailed segment‑by‑segment revenues are reserved for the full report.)

Regulatory action matrix & monitoring calendar: A living tracker of global regulatory milestones (including industrial emissions standards and pharmaceutical elemental-impurity limits) with implications for instrument demand triggers.

Commercial playbooks: Channel strategies, pricing frameworks and maintenance‑service models tailored to vendors seeking to expand in regulated markets or to capture aftermarket revenue streams.

Risk and sensitivity analyses: Stress tests against key uncertainties — enforcement intensity, energy transition pathways, and capital spending cycles among utilities and industrial emitters.

Regulatory duality: Two concurrent dynamics define near‑term demand. In multiple jurisdictions tighter industrial emissions rules and ongoing Minamata Convention enforcement sustain replacement and upgrade cycles for monitoring equipment. Conversely, regulatory rollbacks in certain markets create a two‑speed adoption curve that must be modeled regionally in investment plans.

Sectoral drivers: Pharmaceutical quality control is emerging as a steady, long‑term source of demand driven by elemental impurity limits (ICH Q3D), while environmental and industrial emissions applications continue to dominate cyclical procurement patterns.

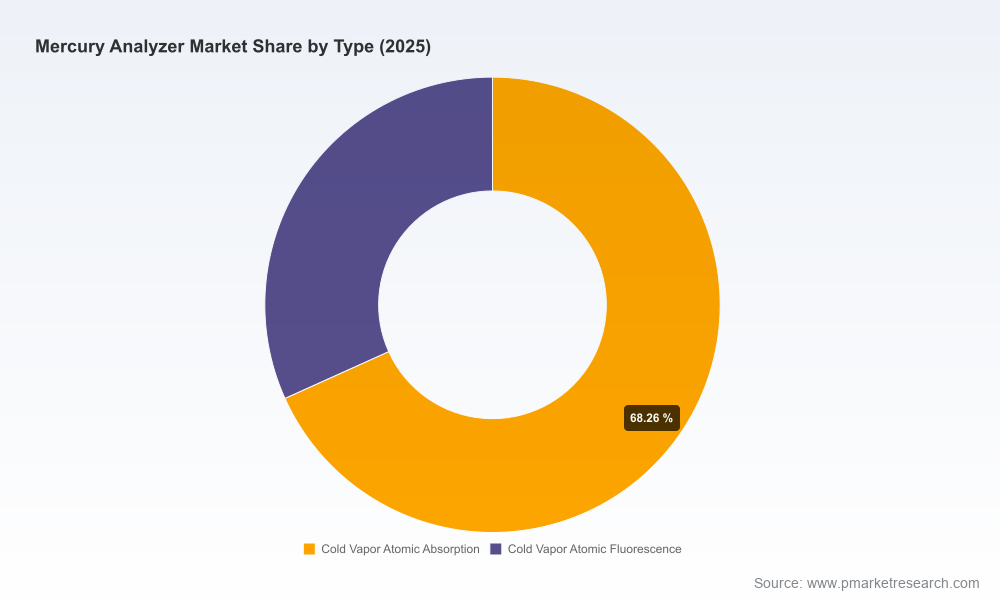

Technology consolidation and differentiation: Cold vapor atomic absorption retains a leadership position for routine laboratory and CEMS use due to sensitivity, cost‑effectiveness and automation. However, portable fluorescence and real‑time continuous monitors are expanding addressable use cases — particularly where on‑site rapid triage or process integration is required.

Market structure and competitive implications: Market concentration indicators point to a field where the top three vendors capture a majority share, and the top five represent a substantial bulk of industry revenue. For buyers, this translates into predictable service ecosystems; for challengers, it implies that differentiation beyond hardware — service, data, and regulatory certification — is essential.

Commercial signals: Recent vendor activities — targeted exhibitions, hands‑on training programs and public procurement contracts — provide near‑term demand signals and vendor strategy cues. These events frequently presage regional expansion plans, service rollouts and product refresh cycles.

Lumex Instruments (Canada): Known for Zeeman atomic absorption systems and portable lines that bridge laboratory and field use. Their visible emphasis on exhibitions and training reflects a strategy focused on technical credibility and hands‑on customer enablement.

Mercury Instruments GmbH (Germany): Specialist in portable analyzers and process monitors for industrial applications — well positioned where rapid, on‑site vapor detection and process integration are priorities.

Teledyne Leeman Labs (USA): Offers laboratory and environmental elemental analysis platforms with strong legacy recognition; suited to institutional lab buyers and regulated testing environments.

ENVEA (France): Focused on continuous emissions monitoring systems (CEMS) and ultra‑trace analyzers for industrial compliance — a strategic choice for utilities and large industrial emitters requiring certified stack monitoring.

Nippon Instruments Corporation (Japan): Holds a durable position in regulatory compliance applications with models targeted at government agencies and geological/laboratory end‑users; recent public contracts underscore their foothold in institutional procurement.

Thermo Fisher Scientific and PerkinElmer (USA): Large, diversified platform providers that integrate mercury analysis capabilities within broader spectroscopy and emissions monitoring portfolios — attractive to multisite laboratory networks seeking vendor consolidation.

Brooks Rand Instruments (USA): Specialist supplier with EPA‑certified analyzers and speciation systems; differentiation rests on method‑specific compliance and high‑precision applications.

Adopt scenario‑based procurement: Build procurement options that map to low, medium and high enforcement scenarios. Lock in modular service agreements and calibration schedules to protect uptime under regulatory uncertainty.

Prioritize interoperability and digital enablement: Instruments offering remote diagnostics, predictive maintenance and standardized data outputs deliver outsized value for multisite operators and environmental service firms.

Monetize aftermarket services: For vendors, service and consumables are the highest‑margin, stickiest revenues. For buyers, evaluate total lifecycle costs and prioritize vendors that demonstrate consistent service KPIs.

Use vendor scorecards in RFPs: Incorporate regulatory certifications, field training offerings, and data integration capabilities into weighted evaluation criteria rather than relying on price alone.

Protect technology roadmaps: R&D leaders should stage investments across sensitivity, portability, and connectivity, preserving optionality as markets bifurcate between high‑enforcement and low‑enforcement regimes.

This briefing is a strategic preview designed to orient 2026 planning cycles and procurement decisions. The full Mercury Analyzer Market report contains the complete, validated market model (base year 2025), granular regional and application splits, vendor scorecards, pricing decks and procurement templates — all curated to support operational implementation and board‑level decisioning.

For teams preparing capital budgets, vendor negotiations or market entry strategies this year, the full dataset and executable playbooks will materially shorten decision cycles and reduce execution risk. Visit the source page to access the complete report and the downloadable toolkits that accompany it.

For detailed analysis of this topic, please visit the official page:Mercury Analyzer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com