Acerola Extract in Food Supplements Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-28 03:57:10

As macro headwinds converge with shifting regulatory priorities and evolving construction-material preferences, 2026 will be a make-or-break year for leaders in the fiber cement value chain. PW Consulting’s latest market study—anchored on a 2025 base year and a seven-year forecast to 2032—translates industry complexity into prioritized, executable choices for executives planning capital allocation, portfolio moves, and go-to-market plays.

Fiber Cement Market

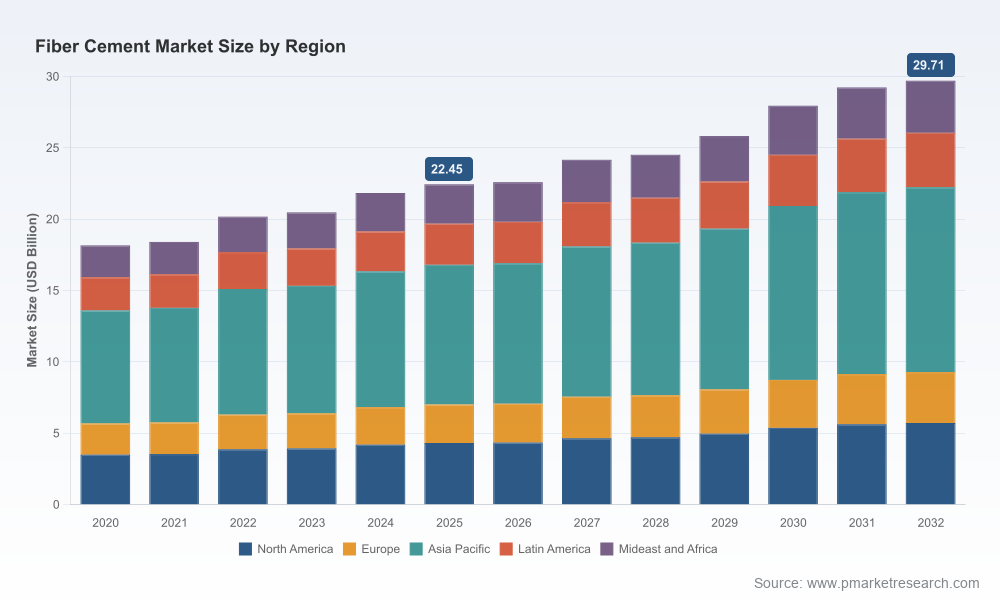

A clear short-to-medium term growth trajectory. Our topline synthesis shows the global fiber cement market expanding from a 2025 base to a materially larger market by 2032 at a steady mid-single-digit compound annual growth rate (CAGR of 4.08%). This steady expansion masks important tactical inflection points in supply, regulation and channel dynamics that will determine which competitors capture disproportionate share.

Fiber Cement Market

Concentration creates optionality—and risk. The market exhibits notable concentration among leading incumbents (the top three firms account for around 60% of market throughput; the top five about 70%). For investors and corporate strategists this translates into both a defensive moat for scale players and premium M&A value for bolt-on acquisitions that can shift local competitive balances.

Fiber Cement Market

Timing of investment matters. With growth steady but not explosive, 2026 becomes a year to optimize capacity utilization, lock in raw-material supply and selectively invest in differentiation—rather than blanket greenfield expansion. Decisions taken in 2026 will disproportionately shape 2027–2029 outcomes as the market enters a phase where incremental volume competes with margin compression driven by rising input costs and regulatory compliance investments.

The sector’s recovery since 2020 demonstrates resilience: from a historical trough to renewed demand by 2025, the industry has reabsorbed pandemic-era disruption and normalized construction cycles. Our forecast models anticipate continued expansion through 2032, reflecting steady demand in renovation and new-build segments, plus product substitutions where fiber cement competes with traditional wood and synthetic claddings. That said, growth is sufficiently measured that strategic differentiation and cost management are prerequisites for outperformance.

Regulatory pressure is rising. Recent regulatory activity—covering safe use and exposure to fibrous silicate minerals from national agencies and special provincial measures—will force manufacturers to accelerate compliance roadmaps, adapt manufacturing controls, and budget for third-party testing and certification. In parallel, testing and conformity criteria updates proposed by certification bodies introduce timing risk for product launches in combustible vs. non-combustible applications.

Input-cost volatility compresses margins. Volatility in cement and cellulose feedstocks, combined with varying labor cost trajectories across high-cost regions, drives heterogenous manufacturing economics. Companies that implement dynamic procurement strategies, hedging and substitution levers will protect margins and create short-term competitive advantage.

Channel and product innovation matter more than ever. As categories mature, incremental gains come from product-system thinking—integrated siding-and-trim solutions, engineered backer systems, and premium surface technologies. Strategic partnerships with builders, distributors and specification agents—rather than purely transactional sales—will accelerate adoption.

Consolidation signals opportunistic M&A. Given the market’s concentration, bolt-on acquisitions that offer adjacent geographic reach or capability—high-performance panels, prefabricated façade systems, or low-emissions cement blends—are high-impact levers for scaling faster than organic growth.

The competitive map is defined by a mix of global platform players and regional specialists. Leading multinational manufacturers bring scale advantages in raw-material sourcing, production efficiency, and distribution reach; regional players preserve agility and local specification know-how. Notable competitors profiled in our study include established manufacturers from Ireland, Belgium, France, Japan, Denmark, the United States and other geographies, each with distinct go-to-market specializations—siding systems, backer boards, high-performance panels, and exterior cladding ranges. These firms are active in product innovation, distribution agreements and brand-led marketing initiatives.

Recent industry activity underscores strategic themes: a major player unveiled new product lines at an international builders’ show in early 2025 and subsequently secured an exclusive multi-year distribution agreement; certification bodies proposed revised criteria late in 2025 that affect where and how fiber cement products can be specified for combustible construction. These developments highlight the interplay between product innovation, channel control and standards compliance becoming decisive competitive levers.

Actionable decision frameworks: scenario-based volume/margin models calibrated to 2026–2032 demand trajectories that allow management teams to stress-test capacity and pricing under varying raw-material and regulatory scenarios.

Supplier & procurement playbook: heatmaps that prioritize supplier relationships by risk and cost-to-serve, with tactical hedging and substitution recipes for cement, cellulose and specialty additives.

Regulatory readiness module: compliance timelines, certification pathways, and capital/operational cost estimates tied to recent agency guidance and proposed standard updates—translated into step-by-step mitigation plans for plant operators.

Commercial acceleration toolkit: GTM playbooks for channel segmentation, specification strategy for architects/specifiers, and builder-distributor partnership models to lift channel share without eroding margin.

M&A and portfolio prioritization lens: valuation multiples, integration risk checklists, and target criteria tuned to markets where consolidation yields the highest ROI given market concentration dynamics.

Benchmarks and KPIs: operations and sustainability benchmarks extracted from primary interviews, plant visits and industry-standard metrics to accelerate performance-oriented transformation programs.

1) Lock in upstream cost certainty: Negotiate multi-year supply agreements with indexed clauses and develop contingency sourcing for critical feedstocks. Consider vertical integration selectively where supplier concentration threatens continuity or cost competitiveness.

2) Fast-track regulatory compliance: Allocate an explicit compliance budget and a cross-functional governance team to navigate evolving standards. Early certification can be used as a commercial differentiator in tender processes.

3) Focus on system-level product differentiation: Shift R&D emphasis from commodity-grade sheets to integrated solutions—prefinished panels, tri-bonded backer systems and low-maintenance claddings that command price premiums.

4) Re-evaluate footprint vs. transport economics: Use the PW Consulting site-level model in the study to run breakeven analyses for regional production vs. centralized exports, driven by labor and logistic cost projections for 2026–2028.

5) Pursue targeted M&A to plug capability gaps: Prioritize bolt-ons that immediately improve distribution reach, specification channels or high-margin product portfolios rather than transformational multibillion-dollar acquisitions in low-growth pockets.

6) Monetize compliance and sustainability: Convert investments in cleaner processes and certifications into market-facing claims that improve sell-through with institutional buyers and premium residential segments.

To preserve the strategic value of the full study and to encourage evidence-based decision-making, this introduction purposefully omits granular segment-level shares, region-by-region dollar splits, and detailed price/volume tables. These are included in the full PW Consulting deliverable along with downloadable model templates that executives can adapt to their own operating assumptions. The summary above provides the strategic context and recommended actions; the full report provides the numerics and models required to operationalize them.

For 2026, the imperative is to move beyond descriptive market updates and adopt a hypothesis-driven implementation plan—rooted in scenario modeling, supplier-risk mitigation, compliance readiness, and targeted commercial plays. PW Consulting’s full Fiber Cement Market study gives you the actionable tools to convert this year’s decisions into lasting competitive advantage: validated models, executable playbooks, and a prioritized set of tactical moves that align with your appetite for growth and risk.

Access the full study to unlock the detailed segment analytics, downloadable models and step-by-step implementation guides that translate these strategic imperatives into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Fiber Cement Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com