Industrial X-ray Inspection Systems Market: Strategic Outlook for 2026

As capital planning cycles reset for 2026, leaders in manufacturing, aerospace, electronics, food & beverage, and industrial services face a pivotal decision window for inspection technology investments. This briefing, drawn from PW Consulting’s forthcoming Industrial X‑ray Inspection Systems Market study (base year 2025, historical series 2020–2025, forecast 2026–2032), synthesizes the strategic implications that matter most to executive teams, corporate development, product management, and operational leaders. It is designed as a high‑signal trailer: authoritative enough to guide immediate conversations while reserving the granular segmentation tables and vendor scorecards for the full report.

Industrial X-ray Inspection Systems Market

Market at a Glance — macro trajectory

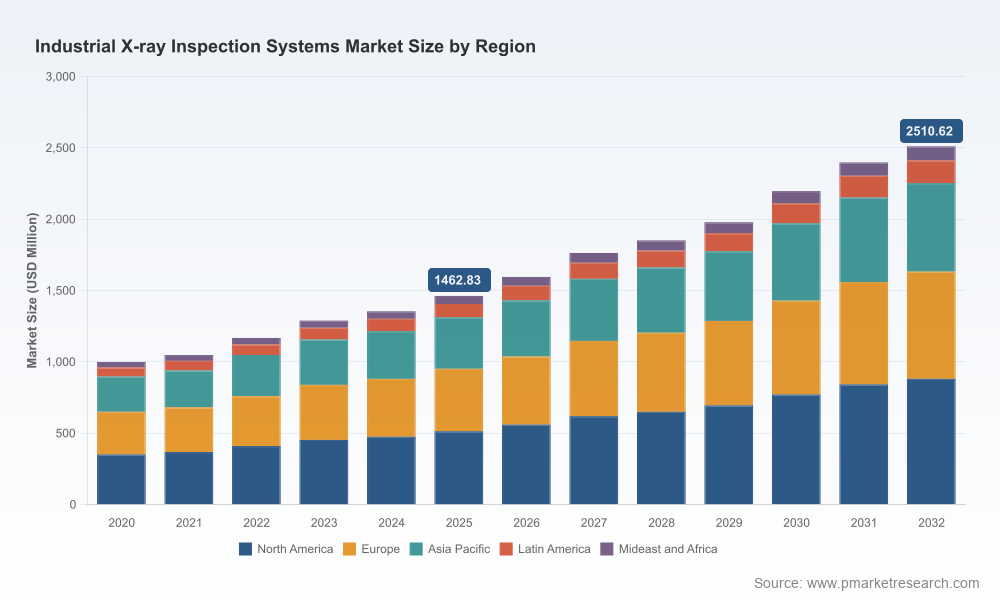

The industrial X‑ray inspection market has transitioned from a recovery phase into a sustained growth profile. Measured in USD (Million), total industry revenue rose from approximately 1,000 in 2020 to about 1,462.8 in 2025, reflecting accelerated adoption across safety‑critical and high‑precision manufacturing applications. PW Consulting’s baseline model projects an 8.0% compound annual growth rate (CAGR) through the 2026–2032 forecast window, bringing total market size to an estimated 2,510.6 by 2032 under the base scenario.

Industrial X-ray Inspection Systems Market

Why this matters now: the combination of mid‑single‑digit to high‑single‑digit CAGR and compounding technology upgrades creates a narrow horizon for first‑mover advantage in hardware refreshes, detector upgrades, and softwareingested analytics. For organizations considering multi‑year capital expenditure programs, an 8.0% growth environment implies both growing supplier margins and intensifying competition for advanced detector components and skilled inspection engineers.

Industrial X-ray Inspection Systems Market

What’s driving growth in 2026

- Regulatory tightening and sector standards: Heightened regulatory expectations — from contaminant detection mandates in food & beverage to component traceability and reliability requirements in aerospace — are converting inspection from cost center to compliance imperative. These forces amplify demand for higher‑resolution, metrology‑grade CT systems and robust digital radiography workflows.

- Technology convergence: Detector innovation (transition from conventional a‑Si panels toward direct‑conversion a‑Se and photon‑counting CT detectors), combined with more powerful reconstruction algorithms, is enabling inspection of denser materials and finer defects. This technological shift is a primary reason suppliers are updating product portfolios and creating new pricing tiers.

- Industrial electrification and additive manufacturing: The proliferation of complex, lightweight components and new materials increases the need for 3D non‑destructive evaluation. Additive manufacturing parts, in particular, are driving demand for high‑fidelity CT metrology to validate porosity, internal geometries, and assembly integrity.

- Aftermarket and services uplift: As installed bases mature, service contracts, detector retrofits, and software subscriptions are becoming meaningful revenue drivers — supporting higher lifetime value per deployment and creating strategic cross‑sell opportunities for OEMs and system integrators.

Competitive landscape — concentrated but dynamic

The market remains concentrated, with the top three suppliers controlling a substantial majority of vendor revenue and the top five representing an even larger share. This concentration fosters a market where new entrants must either pursue clear technological differentiation or align behind channel and service excellence.

Core industry participants profiled in our study include:

- Comet Yxlon (Germany) — High‑end X‑ray and CT systems oriented to aerospace, semiconductors, and critical NDT segments. Focused on integrated inspection solutions and automation for advanced manufacturing lines. (https://yxlon.comet.tech/)

- Nikon Corporation — Industrial Solutions BU (Japan) — Robotic X‑ray and CT solutions optimized for complex parts and metrology‑grade applications. Recent productization activity signals emphasis on compact, high‑precision CT systems for electronics and additive manufacturing. (https://industry.nikon.com/en-aom/)

- DÜRR NDT GmbH & Co. KG (Germany) — Broad portfolio spanning digital X‑ray detectors and scanners, with recent detector launches reinforcing a push into isotope and high‑energy inspection. (https://www.duerr-ndt.com/)

- VisiConsult X‑ray Systems & Solutions GmbH (Germany) — Specialist integrator with strength in customized NDT applications for automotive and aerospace assemblies. (https://visiconsult.de/)

- VJ Technologies, Inc. (United States) — Offers automated and bespoke X‑ray/CT systems across aerospace and industrial segments with emphasis on service and automation. (https://www.vjtechnologies.com/)

- Maha X‑Ray Equipments Pvt. Ltd. (India) — Cost‑competitive manufacturing and export focus; important in low‑to mid‑range deployment segments. (https://www.mahax-ray.com/)

- Bosello High Technology srl (Italy) — Niche player in high‑energy CT for large aerospace castings and custom industrial inspection. (https://www.bosello.com/)

- 3DX‑RAY Ltd. (United Kingdom) — Focused on product integrity and safety checks for manufacturing quality assurance. (https://www.3dx-ray.com/)

Notable product activity captured in our research: Nikon launched a compact metrology‑grade VOXLS CT solution (VOXLS 20 C 225) in April 2025; DÜRR announced a mid‑sized digital detector (D‑DR 2430 NDT) in December 2025 and followed with detector housing variants for large‑format models in March 2026. These moves are emblematic of supplier strategies to cover both metrology and high‑throughput inspection use cases.

Strategic implications for 2026 decision cycles

- CapEx timing and modularity: With detector technology evolving quickly, buyers should favor modular systems that allow staged detector or source upgrades rather than full replacement. Procurement cycles opened in 2026 should include upgrade options and financing that preserve flexibility for 2028–2030 refresh events.

- Product roadmap alignment: OEMs investing in a‑Se and photon‑counting CT technologies are likely to command price premiums and secure early adopters in high‑value sectors. Corporate strategy teams should map R&D pipelines and vendor roadmaps against their own product lifecycles and component obsolescence risk.

- Aftermarket and services as margin anchors: Given the recurring revenue potential from calibration, detector replacement, and software subscriptions, companies should prioritize long‑term service contracts and remote diagnostic capabilities. For suppliers, bundling analytics and training materially increases lifetime value.

- M&A and partnership plays: The high market concentration and technology specialization create opportunities for bolt‑on acquisitions — particularly for players seeking detector IP, reconstruction software, or metrology certification capabilities. Strategic partnerships with AI/ML firms for automated defect detection can accelerate go‑to‑market for both incumbent and challenger vendors.

- Regulatory and compliance preparedness: Firms operating in food & beverage and aerospace must align inspection specifications to evolving FDA, FAA, and EASA expectations. Early alignment reduces validation cycles and shortens time‑to‑production for critical parts.

- Talent and skills strategy: Advanced CT and data interpretation require a different skill mix: physics‑literate inspection engineers, data scientists for reconstruction modeling, and IIoT integrators. Upskilling programs and strategic hires are pressing priorities for 2026 workforce planning.

What PW Consulting’s full report provides (practical deliverables)

This industry brief is a strategic doorway. The full PW Consulting Industrial X‑ray Inspection Systems Market report includes a comprehensive suite of deliverables crafted for executives and practitioners:

- Transparent market sizing and forecasting model (2020–2032) with scenario toggles, growth drivers, and sensitivity analyses.

- Vendor benchmarking and scorecards that evaluate technology stack, breadth of offering, pricing tiers, installed base quality, and service network reach.

- Go‑to‑market playbooks for OEMs, integrators, and service providers — including channel design, pricing architectures, and aftermarket monetization strategies.

- Use‑case prioritization matrices and TCO calculators for buyers to compare compact CT, high‑energy X‑ray, and detector retrofit pathways.

- Regulatory impact assessment and compliance checklists for industry verticals subject to FDA, FAA/EASA, and regional safety authorities.

- M&A heatmaps identifying attractive targets by capability, geographies, and valuation expectations, plus a deal execution checklist.

- Risk register and mitigation playbooks covering supply chain concentration for detector components, rare earth exposure, and skills scarcity.

To preserve the competitive value of our market segmentation and vendor rankings, detailed tables and segment‑level financials are accessible only in the full report. That granular data is what many buyers use to finalize RFP scopes, capex approvals, and M&A valuations — and it is intentionally gated to ensure professional use.

Immediate actions for executives and investors

- Initiate a six‑month audit of installed inspection assets and contract expirations to identify retrofit opportunities and service churn risks.

- Reassess supplier roadmaps and contract clauses to secure upgrade paths for detectors and reconstruction software while managing price escalation risk tied to component scarcity.

- Prioritize pilots that combine advanced detectors with AI‑driven defect recognition to validate performance gains versus incremental cost.

- For investors and corporate development teams: use the market concentration profile and recent product launches to screen targets that can either expand addressable markets or consolidate critical technology for scale economies.

Concluding perspective

In 2026, industrial X‑ray inspection is no longer an adjunct quality check; it is an integral part of product assurance and regulatory compliance. The market’s steady compound growth — underpinned by detector innovation, regulatory tightening, and the increasing complexity of manufactured parts — creates both opportunity and urgency. Organizations that time their investments to align with modular upgrade paths, prioritize aftermarket monetization, and secure partnerships for advanced analytics will capture disproportionate value as the market advances toward 2032.

For the detailed segment breakdowns, vendor scorecards, and the interactive forecast model that financial planners, procurement officers, and M&A teams will rely on, access the full PW Consulting Industrial X‑ray Inspection Systems Market report via our market research portal. The full dataset contains the granular intelligence needed to convert strategy into executable plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Industrial X-ray Inspection Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com