Sustainable Toys Market Size, Share and Strategic Developments (2025–2032)

Other |

2026-03-18 08:47:48

As PW Consulting’s lead industry strategist, this briefing distills the strategic imperatives embedded in our full Polyethylene Glycol (PEG) Market research (base year 2025). It is written for executive teams, corporate development officers, and supply‑chain leadership who must make high‑stakes decisions in 2026 — from capacity deployment and M&A to regulatory risk management and portfolio prioritization. Consider this a high‑fidelity trailer: we reveal the directional trends, competitive dynamics, and decision frameworks that matter, while reserving detailed segmental numbers and proprietary scenario outputs for the full report and accompanying Excel models.

Polyethylene Glycol (PEG) Market

PEG is multi‑sectoral. Its role as an excipient, solvent, lubricity agent and polymer intermediate ties it to healthcare, personal care, industrial formulations and emerging specialty chemistries. Strategic moves in PEG ripple through product pipelines, margin stacks and regulatory exposure.

Polyethylene Glycol (PEG) Market

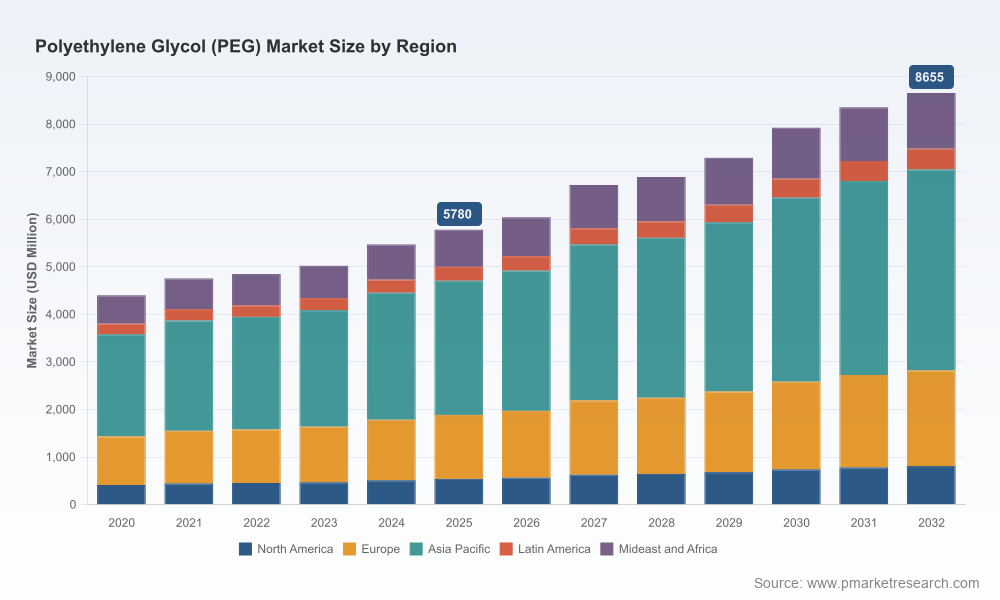

Market trajectory is predictable and material. From a 2020 market base that registered industry recovery and re‑balancing, PEG reached approximately USD 5,780 Million in 2025. Our forecast through 2032 assumes a 6.0% CAGR over the 2026–2032 period, with mid‑cycle scale reaching the higher end of the market as formulators re‑engineer portfolios for performance and compliance.

Polyethylene Glycol (PEG) Market

Concentration is meaningful but not prohibitive. The top three producers account for approximately 45% of the market; the top five collectively approach 58%. That structure creates oligopolistic pricing power in some grades, while leaving pockets of competitive pricing pressure and innovation opportunities for specialists and regional players.

Demand dynamics: Healthcare and personal care remain the primary demand engines. Pharmaceutical applications continue to grow thanks to biologics and formulation needs for oral/topical delivery systems, while personal care formulations value PEG for solvency and emolliency. Industrial demand is steadier but sensitive to cyclical end‑markets.

Feedstock and cost volatility: Ethylene oxide (and upstream ethylene glycol) pricing materially shapes margins. In the second half of 2025, ethylene glycol prices in Asia moved mostly downward due to supply pressure — a dynamic that can compress or expand spreads depending on timing of feedstock procurement and contract structures.

Regulatory pressure and ESG: Regulators are tightening scrutiny on polymers that show persistence in aquatic environments. Recent actions by European authorities signal growing constraints on certain PEG derivatives and heightened documentation and stewardship expectations. At the same time, sustainability mandates push buyers to seek lower‑impact chemistries or demonstrably managed lifecycle footprints.

Supply resilience and localization: The combination of regulatory friction, feedstock volatility, and customer demand for pharma‑grade GMP capability is driving selective reshoring or regional capacity builds. Strategic implications include the value of regional GMP capability, flexible multi‑grade production lines, and proximity to key end markets.

The PEG vendor map contains global majors with integrated portfolios, specialty chemical houses that emphasize excipient compliance, and regional producers that compete on scale and cost. Notable players we profile in the full study include:

BASF SE — leveraging specialty portfolios (e.g., reactive and excipient‑grade PEG offerings) and a strong pharma formulation channel.

Dow Inc. — a scale incumbent with industrial and pharma grades under legacy brands, positioned on formulation performance and global distribution.

Clariant — a fast follower but increasingly strategic in pharma excipients, with investments to establish regional GMP capacity.

INEOS, Lotte Chemical, Sanyo Chemical, India Glycols, Croda, and several Chinese producers — each offers differentiated value propositions spanning price, regional access, and specialty grades.

Recent corporate moves illustrate the competitive responses we expect in 2026: Clariant announced a capacity expansion to establish a U.S. GMP‑compliant pharmaceutical PEG facility in early 2026, signaling that access to certified excipient manufacturing is now a strategic battleground. BASF’s 2025 introduction of a reactive PEG variant highlights continuing product innovation aimed at industrial formulators.

Granular market model (2020–2032): historical series, base‑year calibration (2025), and high‑granularity forecasts by region, by molecular weight band, and by application — all delivered in an editable Excel model that lets you run your own scenarios.

Scenario planning and sensitivity analysis: stochastic and scenario outputs that stress feedstock pricing, regulatory shock events, and capacity shifts — useful inputs for capital allocation and working‑capital planning.

Competitive benchmarking: detailed profiles of the top global players, capacity maps, product portfolios, and go‑to‑market strengths and weaknesses that support M&A screening and partnership targeting.

Regulatory and stewardship playbook: jurisdictional risk maps, compliance checklists for pharma‑grade and consumer‑facing products, and mitigation levers (substitution, reformulation, extended producer responsibility) with estimated implementation timelines.

Procurement and feedstock strategy templates: contracting alternatives (spot vs. long‑term vs. tolling), hedging templates tied to ethylene glycol cycles, and inventory optimization heuristics for multigrade plants.

Commercial playbooks: pricing corridors by channel, margin waterfall tools by molecular weight grade, and customer segmentation to inform sales prioritization and premiumization strategies.

Prioritize GMP capability where pharma exposure is material. The market reward for certified excipients is not merely price premium — it is access to long‑term relationships, co‑development pipelines, and lower churn. Where feasible, accelerate investments that shorten time‑to‑qualified supplier status (e.g., certification, clinical‑use documentation, and audit readiness).

Hedge feedstock risk structurally. Given the demonstrated volatility in ethylene glycol markets, 2026 is the year to secure multi‑year supply agreements with indexation mechanisms and to evaluate partial vertical integration or tolling relationships to lock in spreads.

Invest in sustainability R&D and LCA transparency. Regulatory pressure on persistence and lifecycle impacts is rising. Early movers who can demonstrate lower‑impact PEG or credible stewardship programs (take‑back, biodegradation proof points, polymer stewardship) will find preference in procurement tenders and regulatory negotiations.

Adopt a portfolio approach to capacity and pricing. Maintain a mix of commoditized grades for volume and specialty grades for margin. Agile manufacturing lines that can swing between molecular weight bands deliver strategic optionality in 2026’s uncertain demand and pricing landscape.

Use M&A and partnerships to fill capability gaps, not just capacity. Examples of high‑value targets are regional producers with GMP certification, formulators that hold customer relationships in high‑value niches, or feedstock players that can secure upstream continuity.

Embed regulatory scenarios in capital allocation. Model the impact of adverse policy changes (e.g., tighter restrictions on certain derivatives) on usable grades and conversion costs. Building contingency into project evaluation is now table stakes.

Capital projects: deploy the report’s scenario outputs to stress test IRRs at different feedstock cost levels, regulatory timelines, and uptake curves for specialty grades. Use the model to define trigger points for greenfield versus brownfield options.

M&A: screen targets using our competitive scorecards — prioritize entities that accelerate GMP qualification, expand specialty portfolios, or provide feedstock security in target geographies.

Commercial strategy: reprice contracts for customers willing to pay for documented sustainability and guaranteed supply; reposition commodity offerings to defend volume where margins are thin.

Risk management: operationalize our procurement templates and stock buffer recommendations to blunt short‑term feedstock shocks while you pursue structural mitigations.

Our PEG Market research arms you with a validated macro baseline (2020–2025 historical calibration and a 2026–2032 forecast built on a 6.0% CAGR), an operational playbook for procurement and manufacturing, and a regulatory foresight framework that converts ambiguity into executable options. We map where value will accrue — geographically, by molecular weight band, and by application — and we provide the decision templates you need to prioritize capital, M&A, and product strategy in 2026.

For executives preparing capital allocation memos, M&A screens, or commercial turnaround plans, the full PW Consulting report contains the actionable segmental datasets, the downloadable financial model, and the step‑by‑step playbooks referenced here. Access to those proprietary elements will enable you to move from directional confidence to transaction execution.

Contact PW Consulting or visit our report page to unlock the full dataset, the Excel model, and the supplier scorecards that support rapid, evidence‑based decisions in 2026.

For detailed analysis of this topic, please visit the official page:Polyethylene Glycol (PEG) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com