Genetic Testing FAQs: Answers to the Most Common Questions

Health |

2026-07-03 13:20:41

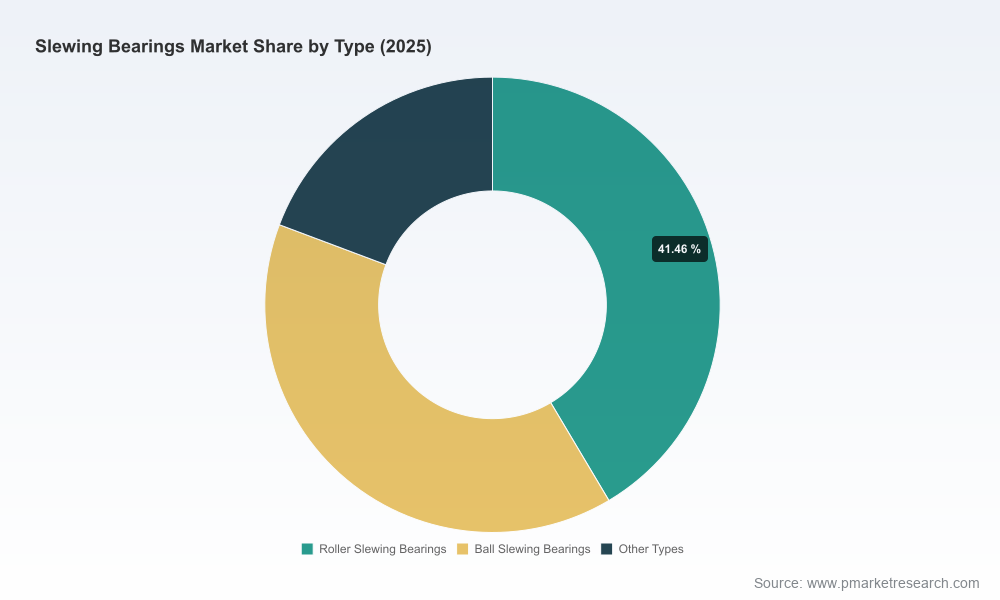

As companies prepare capital allocation, product roadmaps, and supply-chain pivots for 2026, slewing bearings are re-emerging as a high‑leverage component class across heavy equipment, renewables, industrial automation and aerospace adjacencies. PW Consulting’s latest study — built on a 2020–2025 historical baseline (base year 2025) and a 2026–2032 forecast horizon — projects the global slewing bearings market to expand at a compound annual growth rate (CAGR) of 5.95%. The market size moves from an estimated USD 438.27 Million in 2025 toward roughly USD 652.66 Million by 2032, reflecting steady demand growth coupled with pockets of accelerated adoption driven by renewables, automation and aftermarket service models.

Slewing Bearings Market

Decision velocity: Procurement, product development and M&A decisions made in 2026 will shape cost structures and market access across the 2026–2032 window. A single large capital program (e.g., wind, mining OEM, or infrastructure fleet renewal) can alter order books and supplier bargaining power for multiple years.

Slewing Bearings Market

Margin pressure & opportunity: Steel- and material‑intensive manufacturing means raw material volatility compresses margins; meanwhile, modularization, thin‑section innovation and service offerings unlock higher value capture for OEMs and specialized suppliers.

Slewing Bearings Market

Regulatory and sustainability gait: New standards and circularity expectations are shifting manufacturing practices and capital allocation. Companies that align product portfolios and factory footprints early will avoid retrofit costs and regulatory drag.

PW Consulting’s topline model synthesizes demand drivers, supply capacity changes and material cost inputs to forecast a clear upward trajectory. From USD 331.45 Million in 2020 to USD 438.27 Million in 2025 (base year), the market exhibits recovery and steady expansion. The projected CAGR of 5.95% through 2032 reflects a balance: underlying industrial growth and electrification projects increase structural demand, while raw material headwinds and competitive fragmentation constrain margin expansion.

Two structural characteristics to note from the topline modelling: (1) growth is broad‑based but not uniform — certain end markets and product formats capture elevated premiumization and aftermarket revenues; (2) market concentration remains moderate, with the leading three and five players collectively holding under one‑third of global sales, leaving meaningful runway for consolidation and regional champions.

This study is designed to be operationally actionable for strategy teams, procurement, product management and corporate development. Core deliverables include:

Forecast models (2026–2032) with scenario toggles for raw material price shocks, regulatory tightening, and accelerated wind/EV capex — exportable and interactive for internal sensitivity runs.

Supply‑chain stress maps that identify single‑source exposures, alloy steel dependencies (including grades such as 42CrMo) and rare‑earth risk nodes for driven slewing solutions.

Commercial playbooks covering pricing elasticity, aftermarket service design, inventory policies and total cost of ownership (TCO) positioning tailored to OEMs and distributors.

Regulatory impact assessment including ISO implications and EU sustainability guidance, with compliance roadmaps and capex timing considerations.

Competitive benchmarking and capability scorecards for leading manufacturers, plus a prioritized M&A heatmap identifying practical targets across geographies and technology stacks.

Practical supplier selection templates, contract clauses for price escalation and quality acceptance criteria tuned to slewing-bearing specific failure modes.

These components are assembled to move teams from insight to execution within 90 days of review.

The industry is populated by a mix of global incumbents, regional specialists and precision niche players. Key company archetypes observed in the market include integrated global producers, thin‑section specialists, heavy‑diameter OEMs and precision suppliers targeting aerospace/robotics. Notable companies analyzed in the report:

SKF (Göteborg, Sweden): Broad product portfolio spanning standardized and highly customized slewing bearings. Strengths include scale, materials R&D and global aftermarket capabilities.

Kaydon Bearings (Muskegon, USA): Thin‑section and slewing ring expertise with strong inroads into wind energy applications and thin‑section markets.

thyssenkrupp Rothe Erde (Germany): Leader in very large diameter bearings; global footprint and heavy‑duty engineering depth are strategic assets for large OEMs and infrastructure projects.

Specialists such as Scheerer, SlewPro, TGB Group and Silverthin: These players excel in precision engineering, custom drives and target sectors where performance margins justify premium pricing (robotics, aerospace, medical).

Chinese OEMs (e.g., LDB, Fenghe): Competitive on price and local content, increasingly participating in trade shows and expanding export markets.

Recent corporate developments underscore industry dynamics: catalog expansions into high‑margin verticals (e.g., Silverthin’s July 2025 catalog targeting aerospace and semiconductor), facility consolidations and relocations (a 2026 operations update from a major global producer), and intensified trade‑show activity by Chinese and regional manufacturers in 2026. These moves indicate both offensive play (market penetration) and defensive optimization (cost and logistics).

Four dynamics will shape outcomes for 2026 decision‑makers:

Raw material volatility: Steel alloys (including commonly used grades) and rare‑earth elements used in associated actuation systems drive cost and lead‑time risk. Manufacturers with flexible alloy substitution strategies and hedging arrangements will sustain margins better.

Regulatory tightening: New standards (for example, a 2025 ISO standard for certain marine applications) and evolving EU sustainability guidelines force product re‑qualification cycles and may require investment in greener process technologies.

Aftermarket monetization: As fleets age and modular designs proliferate, aftermarket service, condition monitoring and retrofit offerings become differentiated revenue streams.

Consolidation opportunity: With market concentration modest and fragmentation high across regions and product types, strategic M&A or alliance activity can rapidly scale capabilities — but target selection must account for material technology fit and regulatory footprint.

Operational hedges: Establish multi‑tier supplier contracts for key steel grades, implement indexed pricing clauses tied to transparent material indices, and qualify secondary alloy sources to limit single‑supplier exposure.

Product & service differentiation: Invest in thin‑section and integrated slewing‑drive assemblies for electrified applications, and develop predictive maintenance services to capture higher lifetime value.

Regulatory alignment: Map product portfolios against ISO and EU sustainability requirements now; initiate low‑carbon process pilots and circularity programs to avoid late‑stage rework.

Targeted inorganic moves: Use the report’s M&A heatmap to screen targets that materially improve either technical capability (precision bearings, thin section) or market access in priority regions — prioritize acquisitions that yield immediate aftermarket and digital service synergies.

Commercial agility: Reconfigure sales incentives and distributor contracts to reflect TCO rather than unit price alone; bundle bearings with lifecycle services and training to deepen customer lock‑in.

Strategy teams should treat the PW Consulting study as both an input and an executable toolkit. Use the interactive forecast model to stress‑test capital scenarios; apply the supplier stress maps to RFP and sourcing timelines; adopt the compliance roadmaps when setting 2026 CAPEX for factory upgrades. Most importantly, leverage the competitive scorecards to benchmark your technology and commercial positioning against regional champions and precision specialists.

The analysis above outlines the structural story and the clear choices facing executives in 2026: manage material and regulatory risk, sharpen product/service differentiation, and selectively consolidate when scale unlocks aftermarket and technology synergies. PW Consulting’s slewing bearings study goes further — it contains the underlying datasets, interactive models, supplier scorecards and transaction targets that enable teams to convert intent into measurable outcomes.

For the granular datasets, scenario outputs, and executable templates that underpin these insights, visit our report landing page to access the full study and downloadable tools. The summary here is intended to demonstrate our analytical approach and the strategic levers at play while preserving the comprehensive, actionable intelligence reserved for report subscribers.

For detailed analysis of this topic, please visit the official page:Slewing Bearings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com