Anti-decubitus Cushions Market — Strategic Outlook for 2026 Decision‑Makers

Market snapshot: pace, scale and what it means

Our latest PW Consulting market study places the global anti-decubitus cushions market at an inflection point as stakeholders prepare strategies for 2026 and beyond. The market recorded steady expansion through the 2020–2025 historical window, rising from roughly USD 550 million to approximately USD 738 million in 2025. Under our baseline scenario, the market is projected to continue growing at a compound annual growth rate (CAGR) of about 6.05% across the 2026–2032 forecast period, reaching just over USD 1.11 billion by 2032.

Anti-decubitus Cushions Market

These topline dynamics—solid, non‑explosive growth but persistent expansion—frame a competitive environment where product differentiation, reimbursement positioning and supply‑chain resilience will decide winners and losers. Importantly, market concentration metrics point to a mid‑level fragmented structure (CR3 ≈ 35%, CR5 ≈ 45%), which signals both meaningful incumbency advantages for leading players and available pockets of opportunity for focused challengers or consolidation plays.

Anti-decubitus Cushions Market

Why this study matters for decisions made in 2026

- Timing for product and channel investments: With predictable compound growth and growing demand from clinical and homecare settings, 2026 is the year to commit to scalable manufacturing, digital augmentation and service models that capture recurring revenue (rental, refills, servicing).

- Reimbursement-driven differentiation: Durable Medical Equipment (DME) coverage pathways and device classifications are changing how payors evaluate pressure‑reducing surfaces. Alignment with DME rules and proactive coding strategies materially affect time‑to‑market and net selling price.

- Consolidation and partnerships: The market’s concentration profile creates attractive scenarios for bolt‑on M&A to achieve route‑to‑market synergies, particularly when combined with clinical validation or unique materials expertise.

- Risk management: Raw material sourcing (medical‑grade polyurethanes, foams, gels) and standards compliance (ISO and national flammability/launderability requirements) are non‑negotiable constraints that must be managed before scaling volumes.

What the PW Consulting report delivers — practical elements for commercial execution

This study is designed as a decision‑ready toolkit for senior commercial, product and strategy leaders. Rather than a high‑level narrative, the report contains operational modules you can use directly in 2026 planning cycles:

Anti-decubitus Cushions Market

- Top‑line market model (historical 2020–2025 and forecast 2026–2032) with scenario toggles for pricing, reimbursement and adoption curves.

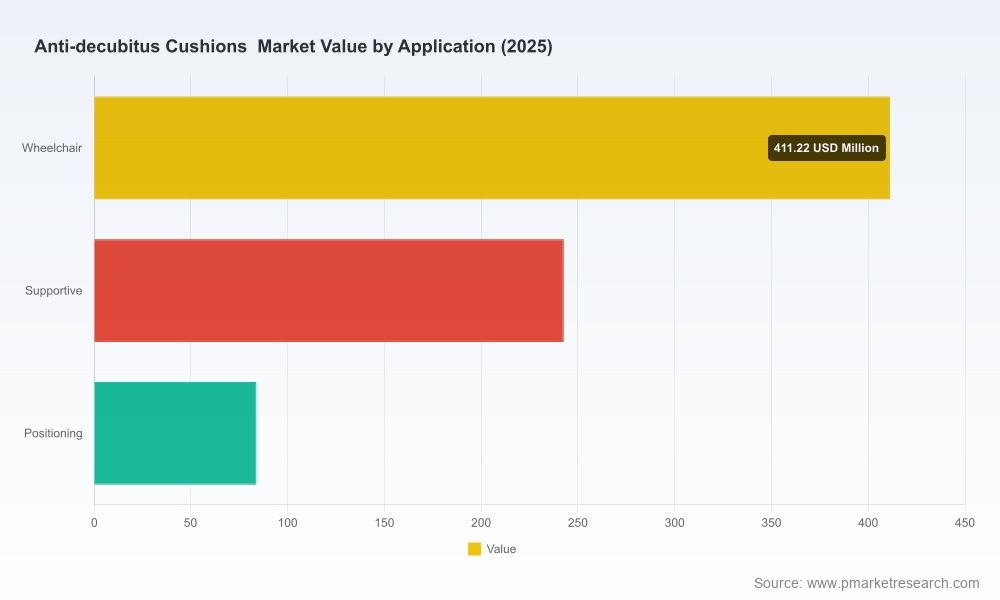

- Segmentation framework by geography, cushion type and end‑use application, plus a confidentiality‑safeguarded dataset that supports prioritization matrices for go‑to‑market investments. (Note: this preview intentionally withholds the full split tables to protect tactical insights—full segmentation is available in the source report.)

- Vendor scorecards and feature maps for the competitive set, linking product attributes (air cell vs. gel vs. foam, intelligent monitoring, custom vs. standard) to clinical outcomes and procurement preferences.

- Clinical and regulatory playbook: mapping of relevant device codes, DME coverage rules, ISO and national standards, and a checklist for rapid regulatory readiness.

- Supply‑chain risk register and cost‑curve analysis reflecting medical‑grade material sourcing, manufacturing complexity and launderability/maintenance requirements.

- Go‑to‑market blueprints for institutional, outpatient and homecare channels, including pricing ladders, rental vs. sale decision trees, and a sample provider contracting term sheet.

- Five‑year ROI calculators and break‑even models for new product introductions and retro‑fit programs, plus sensitivity testing for reimbursement changes.

Competitive landscape — what leading players reveal about strategic priorities

The competitive set is differentiated not just by product form factor but by go‑to‑market model and clinical positioning. Our analysis focuses on four emblematic players whose strategies illustrate prevailing competitive logics.

- Direct Healthcare Group (DHG) — With alternating pressure systems (e.g., Dyna‑Form Mercury Advance) and intelligent air cushions (Dyna‑Tek), DHG demonstrates a twin approach: high‑risk clinical solutions for institutional care and intelligence‑led cushions for monitoring and prevention. Their emphasis on alternating pressure and pressure‑redistribution algorithms makes them a natural partner for acute care contracts and high‑acuity long‑term care providers.

- etac — etac’s vertical air‑cell seat cushions focus on high‑risk prevention, positioning and pressure redistribution, with clear attention to standards (including launderability and flammability norms). Their product philosophy targets clinical robustness and maintainability—attributes valued by procurement teams that prioritize lifecycle cost and infection‑control workflows.

- Invacare — Offers mainstream pressure care wheelchair cushions that combine gel and foam inserts (e.g., Matrx Flo‑tech). Invacare’s strength is breadth and channel reach: modular designs and price points that appeal across outpatient, homecare and Medicaid/Medicare DME channels.

- Permobil (ROHO) — The ROHO line exemplifies premium, customizable air‑cell solutions with strong integration into complex wheelchair platforms. Their strategic play emphasizes personalization and clinical outcomes, which supports premium pricing and bundled sales with mobility systems.

Collectively these companies underscore three strategic imperatives for 2026: invest in clinical differentiation and measurement, design for serviceability and laundering, and align commercial models with payor reimbursement practices.

Dynamics: regulation, reimbursement and materials that will shape commercial outcomes

The policy and standards environment is a structural force in this market. Key considerations include:

- Regulatory posture: Wheelchair cushions are governed by device classifications and applicable device codes that can simplify market entry for many models but still require establishment registration, labeling compliance and adherence to applicable standards. This reduces some barriers but increases the importance of documentation and quality systems in supplier selection.

- Reimbursement landscape: Pressure‑reducing support surfaces fall within DME benefit frameworks. The nuances of coverage, documentation and supplier accreditation can materially affect uptake—especially for higher‑priced, intelligence‑enabled products that require separate justification.

- Standards and operational requirements: Compliance with ISO seating standards and national flammability/launderability rules is non‑negotiable for institutional procurement. Products that demonstrate easy inspection and cleaning win tenders and reduce lifecycle costs for providers.

- Materials and supply constraints: Alternating pressure and air‑cell cushions rely on medical‑grade polyurethane, gels and foams. Material performance affects durability and skin safety; supply disruptions or raw material cost inflation have direct margin and availability implications.

Five prioritized moves for executives preparing 2026 plans

- Clarify product‑to‑channel fit: Use the report’s segmentation and buyer persona tools to map each product SKU to the highest‑value channel (institutional, homecare, rental, bundled wheelchair sales).

- Lock reimbursement pathways early: Secure coding and documentation strategies for DME coverage; build clinical evidence packages that accelerate approvals and reduce payer friction.

- Invest selectively in digital capabilities: Integrate simple sensing and alerts that demonstrably reduce pressure ulcer incidence—our ROI models show faster payback when digital features are tied to service revenue or better reimbursed outcomes.

- Harden supply chains: Establish dual sourcing for critical polymers and gels, and evaluate nearshoring for key assembly steps to reduce lead times and ensure launderable, inspectable designs.

- Evaluate bolt‑on consolidation: Given the market’s concentration profile, acquisitions that add complementary channel access, material expertise or clinical validation can be accretive to growth and margins.

How to use the full PW Consulting study

This industry brief is a strategic preview. The complete report contains the unredacted segmentation tables, granular market-size breakouts by year and scenario, competitive feature scoring, and downloadable financial models you can port into board decks and investment memos. We intentionally withheld some segment‑level figures in this preview to protect the tactical value of the datasets for licensed report holders—accessing the full report provides the precise figures and decision analytics that turn strategy into execution.

For strategy teams preparing 2026 budgets, the full deliverable enables three immediate actions: (1) quantify the revenue upside of product upgrades and bundling, (2) model reimbursement sensitivity to inform pricing and contracting, and (3) build an M&A screening list based on financial and clinical fit. PW Consulting can also provide rapid advisory support to operationalize these actions over a 60–90 day engagement.

Closing perspective

The anti‑decubitus cushions market offers predictable growth with strategic complexity: clinical efficacy, service design and reimbursement mechanics are decisive. Companies that align product design, regulatory readiness and channel economics before 2026 will capture outsized share in the next market cycle. Our full study equips executives with the datasets, frameworks and executable playbooks required to convert the sector’s steady growth into durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Anti-decubitus Cushions Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com