Laptop Repairing Course in Delhi

Other |

2026-06-22 14:39:31

As PW Consulting’s Senior Strategy Advisor and Head of Industry Analysis, I present a focused orientation to our new Travel Insurance Market research — a strategic briefing designed to inform high-stakes decisions in 2026. The travel insurance sector has transitioned from cyclical rebound to sustained structural expansion. Our study (base year 2025; historical window 2020–2025; forecast 2026–2032) synthesizes quantitative market sizing, competitive mapping, regulatory friction, and executable playbooks so that boards, CFOs, and product chiefs can convert macro opportunity into measurable value.

Travel Insurance Market

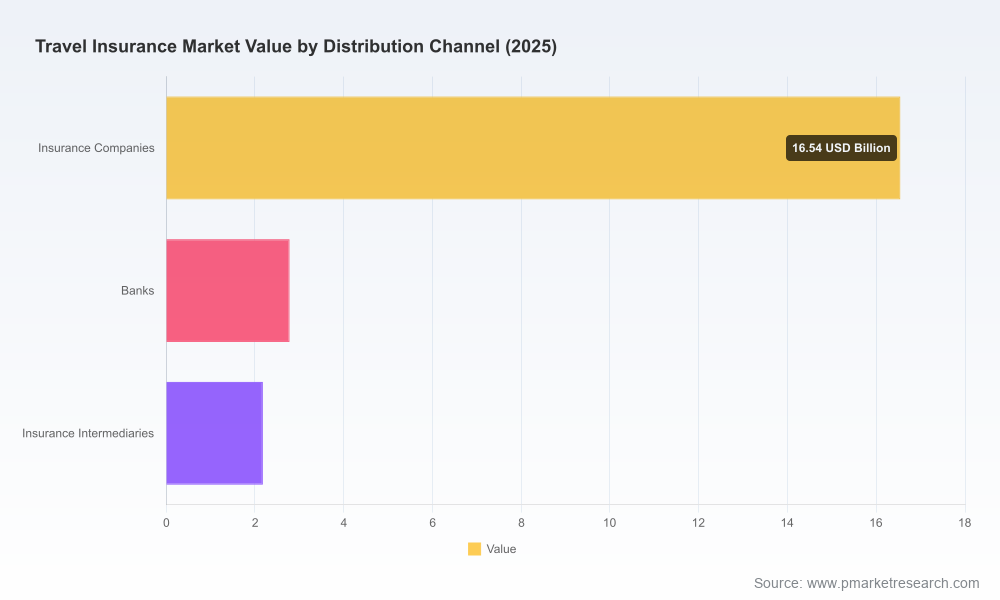

Timing: The market moved from a recovery phase into steady growth. Measured at USD 21.5 Billion in 2025, the sector is projected to continue expanding to the low‑30s Billion range by the end of our forecast horizon, driven by rising mobility, product innovation, and embedded distribution at scale.

Travel Insurance Market

Clarity for capital deployment: With an expected compound annual growth rate of 5.7% across the 2026–2032 forecast, managers must prioritize where to invest — core underwriting capability, digital claims automation, parametric product engineering, or distribution partnerships.

Travel Insurance Market

Execution focus: This research is intentionally tactical — not an academic catalog. It highlights operational levers that materially affect combined ratios and return on capital in travel insurance businesses.

Commercial defensibility: The report helps you evaluate whether to partner, acquire, or build capabilities to defend against both traditional incumbents and nimble InsurTech entrants.

From recovery to structural growth: The market scaled rapidly during the recovery years — rising from a modest baseline in 2020 to over USD 21 Billion by our base year 2025. The projection for 2026 begins the forecast phase with continued expansion and ends in 2032 at roughly USD 32.0 Billion under the baseline scenario.

Drivers of expansion: Demand elasticity from leisure travel, higher average per‑trip premiums tied to medical inflation, growing corporate travel volumes, and the spread of multi‑trip and long‑stay products are converging to sustain demand. Technology‑enabled products, particularly parametric triggers and embedded insurance within booking flows, are accelerating adoption and opening new revenue pools.

Return dynamics: While GWP growth is positive, margin improvement will depend on claims discipline, pricing sophistication, and reductions in administrative friction — areas where the smart market participants will differentiate.

Regulatory complexity: Regulation is not uniform — but in several markets it is imposing significant direct and indirect costs. For example, regulatory obligations in some jurisdictions have been quantified as imposing multi‑billion dollar burdens on customers through compliance overheads. Governance over third‑party data feeds, cloud ecosystems, and automated decisions is receiving growing regulatory scrutiny in mature markets, necessitating investment in compliance, monitoring, and explainability.

Claims & administrative spend: Operational economics are dominated by claims management. Industry studies indicate travel insurers allocate a large share of budgets to claims handling, with a sizable portion absorbed by administrative workflows — an immediate opportunity for automation and reengineering.

Healthcare interface friction: Paperwork and reimbursement processes create external costs, including significant time burdens on public health practitioners in key markets. Streamlining medical claims interactions and restoring provider trust is a priority for insurers who want to reduce friction and speed up settlements.

Price sensitivity: Consumer research shows average international trip insurance premiums are meaningful at an individual level; pricing optimization and clear value articulation are therefore central to conversion rates in digital channels.

The market is bifurcated between global incumbents, specialist regional players, and digital natives. Our competitive map profiles each firm by capability, route‑to‑customer, and product innovation:

Global incumbents (e.g., Allianz, AXA Assistance) retain scale advantages in underwriting capacity, global assistance networks, and B2B2C distribution. They continue to be active acquirers and consolidators of regional portfolios, expanding distribution via both wholesale and white‑label partnerships.

Specialists and niche specialists (e.g., Seven Corners, Travelex Insurance Services, Tin Leg) differentiate through product design targeted at particular travel cohorts — high‑limit medical plans, cruise‑specific cover, and family‑focused multi‑trip offerings.

Digital natives and nomad‑focused carriers (e.g., World Nomads, SafetyWing) compete on flexibility, digital onboarding, and community credibility, capturing segments like backpackers, remote workers, and long‑stay travelers.

New product innovators (e.g., Chubb’s parametric offerings) are integrating insurance directly into booking flows and airline/agency channels, enabling instant refunds and weather guarantees — a capability that materially changes claims frequency and customer satisfaction metrics.

Recent corporate moves crystallize these trends: a major acquisition in mid‑2026 expanded a global partner’s footprint in Australia and New Zealand and included a long‑term white‑label distribution agreement; product launches in late 2025 introduced parametric, instant‑refund travel products designed for embedding at the point of sale; and alliances in 2025 embedded insurer capability directly into corporate travel booking platforms. These examples underline two imperatives — scale through partnership, and product innovation through technology.

Value creation: Faster settlements, parametric design reducing subjective claims, embedded distribution raising attach rates, and targeted underwriting for commercially attractive cohorts.

Value destruction: Overcentralized claims workflows with high administrative overhead; slow remediation of regulatory and data governance exposures; mispriced multi‑trip and long‑stay products that understate medical inflation and exposure.

Operational battlegrounds: Claims automation, provider payments, fraud detection, and real‑time policy lifecycle management.

M&A and partnerships: Prioritize targets that offer either embedded distribution or technology that materially reduces claim cycle times (e.g., parametric triggers, API‑driven provider payments).

Product and pricing: Revisit assumptions for multi‑trip and long‑stay segments to incorporate medical cost inflation and evolving traveler behavior. Test parametric pilots tied to weather, delays, and trip disruption for predictable, low‑touch payouts.

Claims & operations: Target a 20–40% reduction in administrative claims workload through robotics, structured data capture from providers, and delegated authority models with trusted partners.

Regulatory & data governance: Implement a compliance roadmap for cloud‑based decisioning and third‑party data feeds, with audit trails and model explainability built into product lifecycles.

Channel strategy: Invest in B2B2C distribution and embedded insurance partnerships while maintaining direct digital channels for brand, margin, and customer insights.

Our full report provides a practical toolkit: baseline market sizing and scenarios, competitive profiles with capability matrices, go‑to‑market playbooks, a vendor evaluation framework for claims automation, regulatory checklists for key markets, and a prioritized roadmap for product pilots and M&A. It also includes financial benchmarks and sensitivity analyses you can use in investment memos.

In keeping with our “trailer” principle, this introduction presents the macro context and strategic implications but intentionally withholds the granular segmentation tables and raw micro‑datasets that drive competitive tactics (e.g., detailed regional splits, fine‑grained product share percentages, and named channel revenue breakdowns). Those datasets are available in the full report package and come with an interactive model you can use to stress‑test multiple scenarios.

Executive briefing: For boards and C‑suite teams evaluating strategic bets, we recommend commissioning a one‑day briefing that uses your internal portfolio to run live scenario analysis against our market model.

Rapid pilot design: Identify a parametric or embedded distribution pilot to launch within 6–9 months. Use our vendor matrix to shortlist partners for a minimum viable product.

Download the full research package to access the granular datasets, interactive forecast model, and step‑by‑step implementation playbooks.

The travel insurance market in 2026 is neither a simple rebound story nor a mature, closed ecosystem. It is an industry being reshaped by technology, regulatory complexity, and changing mobility patterns. Our research cuts through the noise to show where leaders should allocate capital, where operational change can deliver immediate margin improvement, and how to structure partnerships that scale. Contact PW Consulting to convert the opportunities described here into a prioritized, risk‑adjusted growth plan.

For detailed analysis of this topic, please visit the official page:Travel Insurance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com