Compostable Food Service Packaging Market Beyond Current Trends

Other |

2026-06-24 07:08:15

As senior advisors to executive teams planning for 2026, PW Consulting presents a tightly focused preview of our forthcoming Paint Protection Film (PPF) market study. The global PPF sector has evolved from a niche aftermarket accessory into a strategic layer of vehicle and surface protection solutions, driven by material innovation, rising vehicle parc values, and expanding application beyond traditional automotive uses. Our analysis anchors on a robust historical base and a forward-looking projection: with a 2025 base-year sizing and a compounded annual growth rate (CAGR) of 6.4% over the forecast horizon, the market trajectory suggests sustained, accessible growth through 2032.

Paint Protection Film Market

Timing: 2026 sits at a structural inflection where raw-material dynamics (notably TPU and polyurethane inputs), evolving regulatory standards, and advances in self-healing and hydrophobic chemistries converge into commercially meaningful product differentiation. This is the moment to translate technical product roadmaps into go-to-market moves.

Paint Protection Film Market

Resource allocation: With moderate but persistent CAGR-driven expansion, firms must decide whether to invest in higher-margin premium films, expand capacity to capture scale, or pursue downstream installer and service-channel control. Our research quantifies the trade-offs and expected payback profiles under multiple scenarios.

Paint Protection Film Market

Competitive positioning: The PPF arena balances incumbents with strong brand and distribution (including global chemical and films corporations) against nimble regional manufacturers and technology-focused challengers. The market concentration metrics in our study highlight a moderately consolidated structure that still leaves material opportunity for targeted disruption.

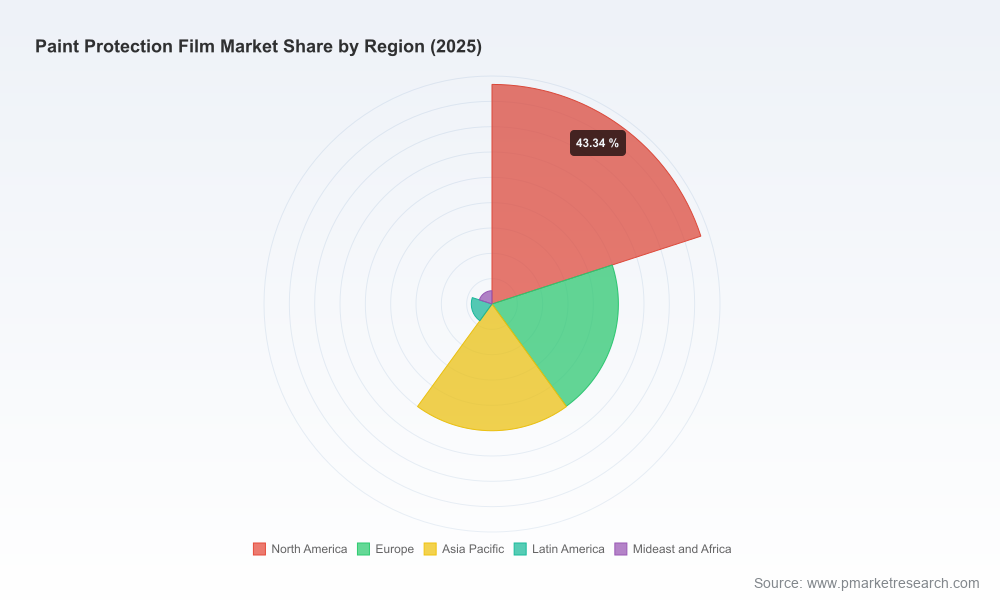

PW Consulting’s base-year analysis (2025) establishes a market size that validates PPF as a meaningful investment category within automotive and adjacent surface protection strategies. From a historical recovery and growth run (2020–2025), the sector is forecast to expand at a steady mid-single-digit CAGR—6.4%—through the 2026–2032 horizon, with the market moving into the billion-dollar territory by the end of the forecast window. This pace implies predictable demand expansion for premium, performance-enhancing films and creates a multi-year runway for product development, channel build-out, and backward integration into raw materials.

Raw-material concentration and technology: Thermoplastic polyurethane (TPU) and polyurethane-based films continue to dominate advanced PPF formulations because of their intrinsic self-healing and hydrophobic capabilities. Control over TPU supply chains and polymer formulation know-how is a competitive lever; vertical integration or long-term procurement contracts materially alter margin and service elasticity.

Standards and regulation: New standards from national and international bodies — including developments reported within Indian and UNEP frameworks — are beginning to codify material and performance baselines for PPFs and related polymers. Compliance readiness affects product certification, cross-border trade, and warranty structures, and will be a differentiator in selling into fleets and OEM programs.

Product differentiation beyond protection: Innovations in finish (gloss, matte, color-stable topcoats), dry-install technologies, and multi-functional coatings (e.g., integrated ceramic-like properties) are converting single-use installers into value-added service partners. This increases lifetime revenue per vehicle and changes competitive dynamics between pure-film manufacturers and integrated service providers.

Channel economics: Installer networks, training programs, and localized service models remain the primary route to end-users. Firms that pair product innovations with robust installer enablement capture higher retention and pricing power; distribution-only plays face margin compression unless they pursue branded service partnerships.

The PPF market combines long-established global industrial players with specialized PPF brands and regional manufacturers. Industry participants fall into three broad archetypes: (1) global chemical/film conglomerates offering integrated product portfolios and channel reach; (2) specialized PPF brands focused on film chemistry, installer support, and aftermarket positioning; and (3) regional manufacturers that leverage cost-competitive production and localized distribution.

LEGEND® PPF (North Carolina, USA): A U.S.-based manufacturer emphasizing aliphatic TPU-based PPF tailored for North American installers. Strengths include localized production, high control over formulation, and installer-focused channel programs.

XPEL Inc. (USA): A brand built on self-healing film innovations and broad aftermarket recognition. Their product positioning stresses protection against rock chips and scuffs and they maintain extensive installer networks — a model that demonstrates the value of aligning product R&D with service ecosystems.

3M Company (USA): Leveraging industrial-scale film manufacturing and cross-category coating expertise, 3M’s Scotchgard Pro Series demonstrates how traditional materials companies can translate R&D scale into premium PPF offerings and institutional sales.

STEK USA, UPPF-USA, Pure PPF, Ceramic Pro, LLumar Films, and TeckWrap (USA and multinational footprints): These firms represent variations of the specialized brand model — combining finish options, hydrophobic and self-healing properties, and installer training. Several have deep ties to ceramic and window-film segments, enabling bundled offers.

ORAFOL (Germany) and multiple China-based manufacturers (e.g., Kehui, Sino Vinyl, GSWF, REEDEE, Livinyl): These players illustrate the geographic diversity of supply and the strategic choices firms face: source differentiation on clarity, finish, and price; or invest in co-development to secure unique formulations.

Market concentration data indicate a competitive set where the top firms command a meaningful share of market activity, but not to the point of excluding regional entrants — a structure that favors strategic partnerships, niche premium plays, and selective M&A.

Trade shows and product unveilings in late 2025 and 2026 have rapidly advanced product narratives: Ceramic Pro’s demonstrations at SEMA, LLumar’s exhibitor showcases, TeckWrap’s dry-install demonstrations, and ORAFOL’s trade presentations all signal strong innovation velocity and an increasingly experience-led buyer journey.

Firms exhibiting at global print and automotive expositions are prioritizing installer education and real-world demonstrations — an endorsement of service-capability investments as much as product innovation.

Scenario-based market sizing and demand drivers: actionable scenarios that map how price, raw-material availability, and channel strategy affect near-term revenue and margin outcomes.

Profitability maps by go-to-market strategy: comparative analyses of OEM-specified supply, aftermarket premium positioning, and distributor-only models, including investment timelines and sensitivity to TPU cost swings.

Regulatory and compliance playbook: concise checklists and product certification pathways to align product development with emerging standards, reducing time-to-market friction.

Competitive benchmarking and partnership matrix: qualitative profiles and capability maps for leading PPF firms, with suggested partnership and acquisition targets based on strategic fit and capability gaps.

Installer and channel enablement toolkit: sample commercial terms, training program outlines, and co-marketing frameworks to accelerate adoption across service networks.

If you are a material supplier: prioritize long-term TPU supply agreements and consider selective downstream partnerships to capture formulation IP value.

If you are a PPF brand: invest in installer economics and performance guarantees that differentiate on service outcomes more than price alone.

If you are a distributor or installer group: evaluate bundling PPF with ceramic and window-film services to increase lifetime value per customer.

If you are an investor or M&A lead: seek targets that combine proprietary film chemistry with established installer networks; the current market structure rewards scale in brand and channel.

Raw-material price shocks and supply-chain constraints linked to TPU production — these can compress margins quickly for non-integrated players.

Fragmentation of installer quality and post-install support, which can erode consumer trust in high-end PPF and increase warranty liabilities.

Emerging regulation and standards (national and international) that may impose testing, labelling, or composition requirements — early compliance is a market-access advantage.

This preview outlines the evidence-based contours you need to calibrate 2026 capital allocation and commercial strategy. The full PW Consulting PPF report contains the granular segment-level intelligence, regional demand matrices, price and cost curves, and vendor scorecards that firms require to finalize executable plans. In the spirit of a strategic “trailer,” we have shown the major themes and directional data (including the 2025 market base and a 6.4% CAGR to 2032) while preserving the detailed segmentation and proprietary model outputs for our subscribers and clients.

For leadership teams preparing 2026 budgets, this study is designed to shorten the decision cycle: validate investment theses, prioritize capability gaps, and align product and channel roadmaps with the most likely commercial outcomes. PW Consulting can support tailored deep-dives — including bespoke scenario modeling and partner sourcing — to convert insight into measurable actions.

For detailed analysis of this topic, please visit the official page:Paint Protection Film Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com