Unlocking Innovation with Software Defined Vehicles Architecture

Other |

2026-02-16 10:08:12

As global demand for electro‑optical and infrared capabilities accelerates across defense, automotive, industrial and security applications, senior leaders must decide today how to position product roadmaps, supply chains and M&A agendas to capture the next wave of value. PW Consulting’s new Infrared Lens Market study—anchored on a 2025 base year, a 2020–2025 historical series and a 2026–2032 forecast horizon—translates that trajectory into actionable choices. The market we track expanded from roughly 138 million USD in 2020 to about 192 million USD in 2025 and is forecast to surpass 315 million USD by 2032, reflecting a compound annual growth rate of 7.52% over the forecast window. This briefing explains why that trajectory matters for 2026 planning, what strategic moves produce durable advantage, and what the full report delivers to support rapid, confident decisions.

Infrared Lens (IR Lens) Market

Technology convergence: Advances in sensor performance (MWIR/LWIR/SWIR), materials engineering and miniaturized optics are compressing development cycles and enabling new product classes—from compact uncrewed systems to embedded automotive thermal sensing.

Infrared Lens (IR Lens) Market

Supply‑chain sensitivity: The IR optics value chain is increasingly exposed to raw‑material concentration and export controls; procurement decisions now carry strategic risk implications that extend beyond cost into program continuity and regulatory compliance.

Infrared Lens (IR Lens) Market

Commercial scale inflection: Forecast growth at ~7.5% CAGR implies expanding addressable volumes, but also intensifying competition—companies that secure scale advantages (through vertical integration, trusted supply agreements or OEM partnerships) will capture disproportionate margin uplift.

The market’s historical expansion and forecast growth underline two realities for 2026: first, demand is broadening beyond traditional defense and high‑end industrial buyers into automotive safety, consumer thermal imaging and mass‑market surveillance; second, the pace of innovation in materials and production is a leading indicator of which suppliers will be able to scale profitably. For executives this generates three immediate lines of action:

Secure supply continuity: prioritize contract structures and dual‑sourcing strategies for critical substrates and coatings to avoid program delays driven by raw material shortages or export constraints.

Invest selectively in alternative materials: fund or partner on near‑term substitutes (e.g., polymer‑based or chalcogenide solutions) to reduce exposure to germanium price/availability shocks.

Calibrate go‑to‑market by segment economics: target segments where unit economics improve with scale or where regulatory sourcing rules create natural protection for compliant suppliers.

Germanium remains central to high‑performance LWIR/MWIR optics, but its supply chain has shown vulnerability to disruption. Procurement teams must map material sources, lead times and held inventory—short‑term buying is no longer an adequate hedge.

Chalcogenide glasses and novel polymer formulations are maturing as pragmatic alternatives. Notably, recent academic innovation on repairable polymer‑based IR lenses signals a potential low‑cost, sustainable path for certain thermal imaging applications; commercialization timelines will determine whether this is a near‑term procurement lever or a 3–5 year strategic play.

Vertical integration of material processing and assembly materially reduces total delivered cost for many suppliers. Firms that control substrate production, coating and lens assembly can compress lead times and improve negotiating leverage—factors that matter for defense and high‑volume commercial OEMs alike.

Export controls on critical elements create program‑level risk for defense and industrial purchasers. Organizations subject to domestic sourcing mandates must build traceability and contractual guarantees into supplier relationships; failure to do so can stop programs or force costly redesigns.

Market participants are increasingly localizing capacity for strategic reasons. New domestic production lines for chalcogenide glasses and the emergence of NDAA‑compliant supply streams are reducing single‑point dependencies—but these solutions come at a premium and require early investment commitments.

Procurement strategies that treat materials as a strategic asset (including inventory policies, long‑lead contracting and qualifying alternative substrates) outperform classical lowest‑price sourcing models under the current risk environment.

The IR lens supplier landscape blends vertically integrated heavyweights, precision optics specialists, OEM module providers and regional manufacturers. Market concentration is meaningful: the top three players account for roughly two‑fifths of the market by revenue, while the top five approach roughly three‑fifths—enough concentration to influence pricing and supply, but also leaving room for specialists and emerging material innovators to win niche positions.

LightPath Technologies (United States): a vertically integrated producer offering germanium alternatives and MWIR/LWIR assemblies. Their investment in domestic processing reduces exposure to foreign export risks and improves supply continuity for sensitive programs.

TAMRON (Japan): recognized for precision optics and uncooled IR lens production targeted at automotive and security; strength lies in manufacturing scale and quality control for high‑volume applications.

Umicore (Belgium): combines materials science and assembly capabilities, supplying proprietary germanium and chalcogenide glass solutions—an example of how upstream material ownership can be a strategic differentiator.

Ophir Optronics (Israel): focuses on precision continuous‑zoom optics across MWIR, SWIR and LWIR—appealing for platforms requiring adaptable field-of-view without heavy integration cost.

Beijing Lenstech & Kunming Full‑wave (China): regional producers with strong domestic sourcing and competitive cost profiles; however, geopolitical and export‑control considerations affect their role in certain programs.

Raytheon (RTX) & Teledyne FLIR (United States): system‑level OEMs delivering integrated EO/IR assemblies and camera modules, with deep defense relationships and programmatic buying power.

Edmund Optics & Resolve Optics (United States/UK): versatile suppliers of stocked and custom IR substrates and assemblies, useful for rapid prototyping and lower‑volume production runs.

Recent industry movements illustrate these dynamics. Academic groups and smaller innovators are advancing polymer‑based repairable lenses, suppliers are refreshing product catalogs with new zoom and high‑volume LWIR modules, and established OEMs are emphasizing supply continuity for defense programs. These trends collectively tighten the window for strategic decisions in 2026; late movers will face elevated sourcing costs and longer qualification cycles.

Our full study translates market intelligence into tools executives can deploy immediately. Key deliverables include:

Comprehensive market model (2020–2032): downloadable spreadsheets and scenario engines that allow you to test pricing, material shocks and demand shifts against revenue and margin outcomes.

Supplier scorecards and validated capability matrices: side‑by‑side assessments of material ownership, production footprint, quality certifications and program‑level compliance (NDAA and equivalent frameworks).

Supply‑chain stress‑test playbook: step‑by‑step procurement templates for dual‑sourcing, inventory buffering, long‑lead contracting and supplier development for alternative substrates.

Technology adoption roadmap: timeline and commercial readiness levels for critical alternatives (chalcogenide glass scale‑up, polymer innovations, coating advances) and recommendation on where to co‑invest.

Regulatory & geopolitical impact matrix: practical guidance on supplier selection, contractual clauses and qualification regimes tailored to defense, automotive and commercial buyers.

M&A and partnership targets: prioritised lists and valuation heuristics for acquisitions, minority investments or strategic JV partners that accelerate vertical integration or regional diversification.

12‑month tactical plan: prioritized actions for R&D, procurement and commercial teams with estimated cost, lead time and expected ROI for each initiative.

For procurement leaders: convert the supply‑chain stress‑test into immediate contracting decisions—identify and qualify at least one alternate substrate supplier and secure multi‑quarter safety stocks for critical components.

For product and R&D heads: allocate a proportion of next year’s budget to explore polymer/chalcogenide options in parallel with continued germanium roadmaps; early pilots accelerate time‑to‑market if supply shocks occur.

For corporate development teams: prioritize targets that either add upstream material capability or open an NDAA‑compliant supply channel; the market’s concentration favors deals that offer a path to scale.

For executive leadership: treat IR optics not as a commodity buy but as a strategic asset. The combination of forecast growth and supply‑side sensitivity makes it a lever for competitive differentiation.

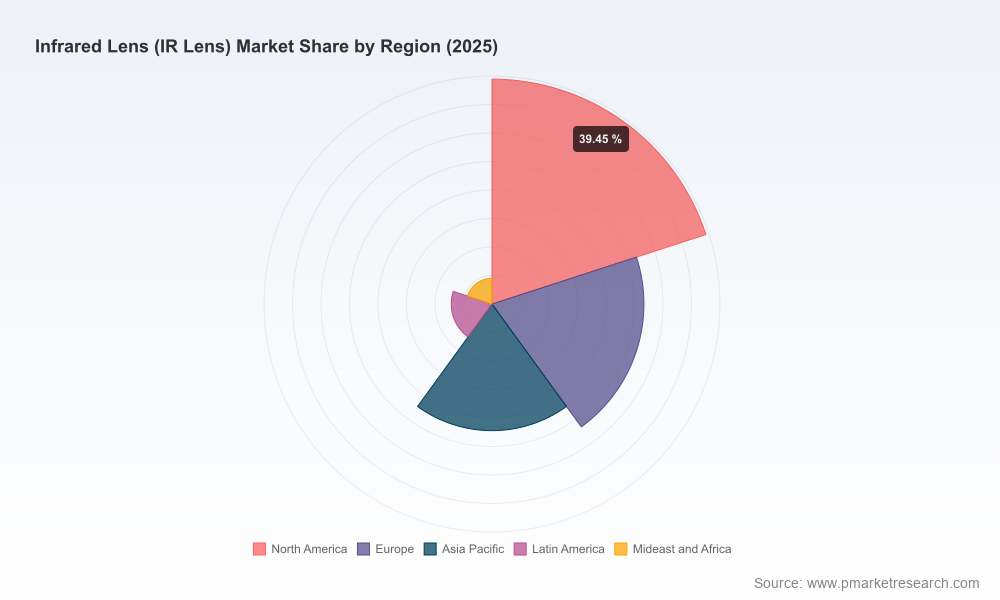

This briefing demonstrates the market’s direction, competitive forces and the actionable frameworks we use to advise clients. To preserve the report’s role as a decision‑support asset, we intentionally do not disclose full regional or application‑level revenue splits, nor the detailed segment tables and unit‑price curves that underpin our scenario models. Those detailed datasets, along with supplier scorecards and model files, are included in the full PW Consulting Infrared Lens Market report and are required to execute the tactical playbook we outline here.

For organizations preparing 2026 budgets or strategic roadmaps, this is a pivotal moment: secure supply continuity, commit to select material alternatives, and align M&A/procurement on a 12‑month execution plan. PW Consulting’s full report provides the quantitative models, supplier intelligence and executable templates needed to convert that strategy into results. Contact our research desk to obtain the complete market dataset, supplier scorecards and the scenario engine that will make your 2026 decisions defensible and outcome‑oriented.

For detailed analysis of this topic, please visit the official page:Infrared Lens (IR Lens) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com