Dishwashing Detergent Market Growth in Commercial Cleaning Sector

Other |

2026-04-07 06:37:59

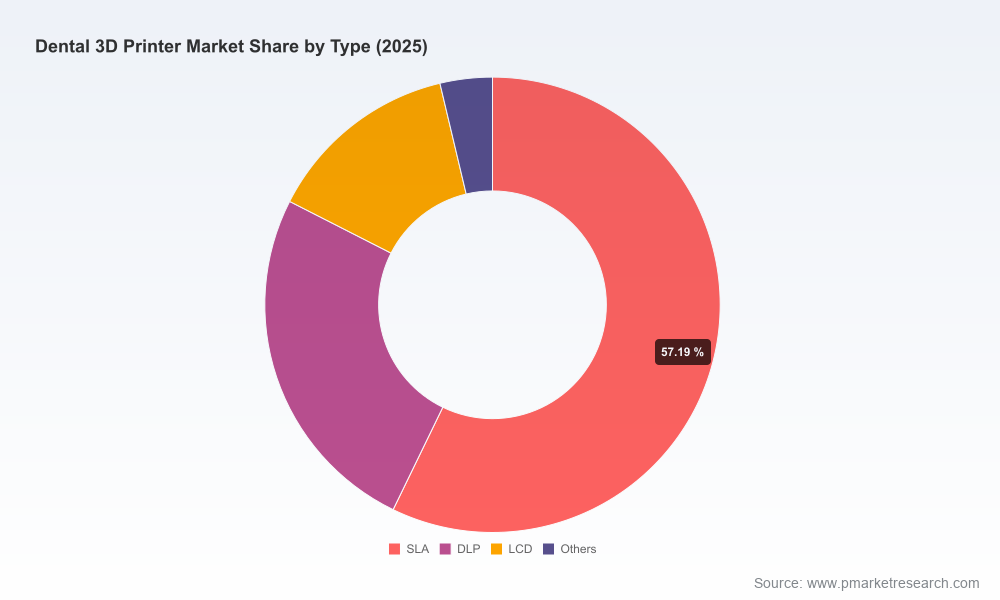

By 2025 the global dental 3D printer market had evolved from an early commercial phase into a more diversified and clinically integrated industry. PW Consulting’s latest market study (base year 2025, forecast 2026–2032) quantifies that evolution: the market advanced from roughly USD 98.45 Million in 2020 to USD 143.76 Million in 2025 and is projected to continue growing to an estimated USD 224.42 Million by 2032, at a compound annual growth rate (CAGR) of approximately 6.98%. This study is built to inform capital allocation, product strategy, M&A screening, and commercial planning as organizations prepare for the decisive strategic moves of 2026.

Dental 3D Printer Market

Timing matters. The market is transitioning from niche lab deployments to broader chairside and same‑day clinical workflows. That transition creates windows for premium pricing and bundled service models, but also raises the bar on regulatory compliance, materials development, and clinical validation. Executives planning 2026 launches or funding rounds need to align product readiness with reimbursement and regulatory momentum — our study identifies the inflection points and adoption milestones to watch.

Dental 3D Printer Market

Investment and M&A prioritization. With increasing product innovations and recent regulatory clears, discerning which technology stacks (printer hardware, material chemistry, and software workflow) are likely to command differentiated margins is critical. The report provides a repeatable evaluation framework to rank targets for inorganic growth, licensing, or distribution partnerships.

Dental 3D Printer Market

Commercial model redesign. As clinics capture higher value through in‑house printing, channel strategies must evolve from transactional equipment sales to recurring revenue via materials, service contracts, and cloud workflows. Our study maps out viable go‑to‑market permutations and their revenue implications, enabling CFOs and commercial leaders to stress‑test revenue mixes for 2026 budgeting cycles.

Growth in the dental 3D printing space is being driven by four converging forces: technological maturity of additive platforms, a widening palette of biocompatible and FDA‑cleared materials, the economics of same‑day dentistry, and increasingly favorable reimbursement frameworks in major health markets. The combined effect is predictable—steady year‑over‑year expansion at a mid‑single digit CAGR through the forecast horizon—but the distribution of that growth is uneven across technologies, clinical applications, and distribution models. Our market model captures both the aggregate trajectory and alternative scenarios tied to regulatory and reimbursement outcomes.

Transparent market sizing and forecasting (2020–2032) with scenario analysis and sensitivity testing tied to key variables — adoption rates, reimbursement changes, and regulatory approvals.

Go‑to‑market playbooks for vendor, lab, and clinical audiences: pricing strategies, channel economics, and retention levers for 2026 rollouts.

Vendor scorecards and product matrices covering hardware precision, throughput, material ecosystems, software integrations, and service economics.

Regulatory and reimbursement tracker: a practical matrix that maps clearances, predicate considerations, and payer landscape implications for core product families.

Implementation blueprints and ROI models for clinics and labs, including CapEx/Opex tradeoffs for chairside adoption versus centralized production.

Supply chain and materials roadmap, highlighting critical suppliers, bottlenecks, and strategies to secure differentiated resin portfolios.

M&A and partnership pipeline — a prioritized watchlist of adjacency plays, integration risks, and value capture opportunities.

The competitive field is a mix of vertically integrated incumbents, specialized dental OEMs, and platform players with broader additive portfolios. Several notable themes emerge from our company analysis:

SprintRay (Los Angeles) continues to position itself around chairside efficiency and clinically focused resins, leveraging FDA clearances to support fixed prosthetics and hybrid workflows. Their strength is a combined hardware + materials approach aimed at the in‑office practitioner.

Formlabs (Somerville) has concentrated on accessible SLA platforms and a broad resin ecosystem for models and temporary restorations — their strategy emphasizes affordability and developer ecosystem extensions for labs and small clinics.

Asiga (Sydney) differentiates on precision and open material libraries, making it attractive to dental labs that require high throughput and material flexibility for complex restorations.

LuxCreo (U.S.) is notable for an end‑to‑end direct‑print aligner system with FDA clearances and automation — a verticalized play that targets the high‑volume orthodontic segment with a distinct value proposition.

3D Systems and Stratasys represent the higher‑end, multi‑technology incumbents. 3D Systems has recently commercialized a jetted, multi‑material denture solution and expanded its materials portfolio; Stratasys’s multi‑material PolyJet systems target lab workflows that demand color and compositional fidelity.

Carbon and other materials innovators are pushing into clinically cleared resin chemistries for removable partial dentures and flexible appliances — a sign that materials differentiation will be a prime battleground for margin capture.

Acknowledged smaller suppliers and regional OEMs fill important niches around price‑performance and service coverage, creating a moderately fragmented supplier base that still rewards scale and proprietary material ecosystems.

Regulatory clearance activity has accelerated and materially affects commercial viability. Several vendors have secured 510(k) pathways for specific dental indications, enabling broader clinical adoption and payer conversations. Concurrently, reimbursement frameworks in mature markets (notably North America) are aligning in ways that favor digital restorations — a structural tailwind for certain printer‑material combinations. For 2026 planners this means prioritizing clinical validation and payer engagement early in the product lifecycle to avoid delayed uptake.

Prioritize FDA‑ready materials and predicate strategies: Allocate development and validation budget toward material chemistries that unlock high‑value clinical indications (e.g., prosthetics and denture workflows).

Bundle hardware, materials and digital services: Design commercial offers that convert one‑time equipment sales into recurring revenue through consumables, cloud subscriptions, and service SLAs.

Target regulated clearances as a market access lever: Use cleared clinical claims to accelerate payer engagement and premium pricing for clinical customers focused on same‑day delivery.

Lock material supply and diversify manufacturing: Given rising demand for FDA‑cleared resins, secure strategic supply agreements and consider backward integration for critical chemistries.

Segment GTM by customer economics, not geography alone: Differentiate propositions for high‑volume labs, chairside clinics, and orthodontic chains; adapt financing and service models to each segment’s unit economics.

Use M&A defensively and offensively: Acquire complementary material IP or software workflow players to accelerate time‑to‑market, and secure distribution in underpenetrated clinical channels.

This PW Consulting study is designed as an operational playbook rather than a high‑level forecast. For 2026 planning cycles, teams should use our scenario outputs to stress test R&D roadmaps, link regulatory milestones to sales forecasts, and build integrated P&L models that capture recurring consumable demand. The vendor scorecards and implementation blueprints are purpose‑built to shorten trial‑to‑deployment timelines and to quantify ROI for procurement and clinical leadership.

In this overview we have intentionally highlighted high‑level trends and strategic implications while withholding granular segment allocations and proprietary benchmarking that form the core of the full PW Consulting dataset. The full report contains detailed regional and application splits, pricing matrices, CR analyses, and downloadable financial models that power transactional decisions — essential inputs for deal teams, product managers, and commercial executives preparing definitive 2026 strategies.

If you are preparing capital plans, product roadmaps, or M&A screening for the 2026 horizon, PW Consulting’s full Dental 3D Printer Market report provides the quantitative backbone and executable playbooks required to convert strategic intent into measurable outcomes. Contact our team to schedule a briefing or to license the complete dataset and model packages designed for immediate integration into corporate planning workflows.

For detailed analysis of this topic, please visit the official page:Dental 3D Printer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com