Electric Toothbrush Market — Strategic Preview for 2026 Decisions

As PW Consulting’s lead industry analyst, I present a condensed strategic briefing drawn from our full Electric Toothbrush Market study (base year 2025). This preview is structured to equip senior leaders and investment committees with the high‑impact market signals they need to prioritize 2026 actions — while reserving the granular segment-level tables and proprietary forecasts for the full report. What follows synthesizes the market’s macro trajectory, competitive dynamics, regulatory inflection points, and the practical playbook elements that will determine winners over the next planning horizon.

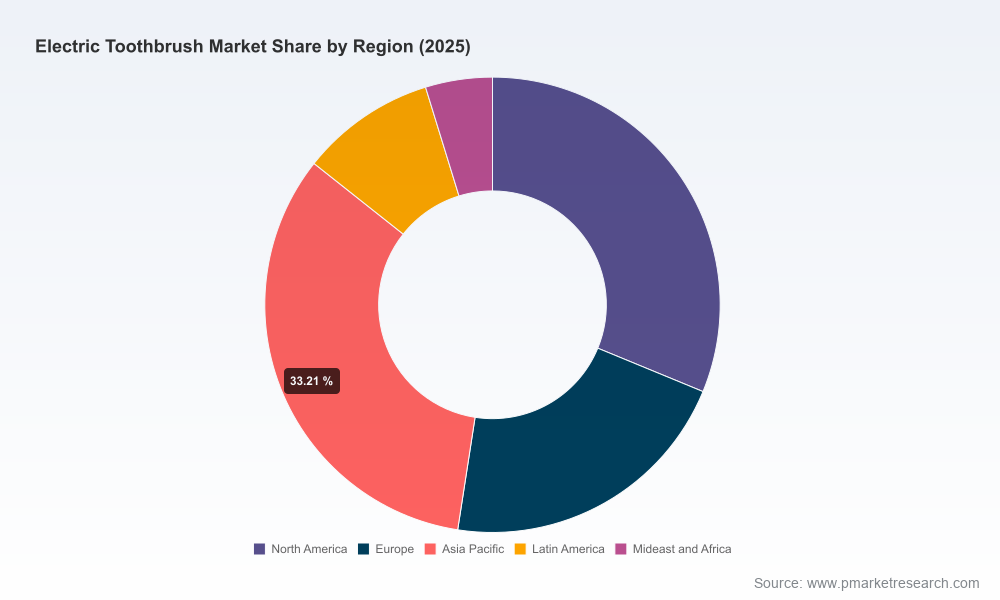

Electric Toothbrush Market

Market snapshot: growth trajectory and market structure

The electric toothbrush market has shifted from niche to mainstream over the last half decade. Our historical reconstruction shows steady expansion from 2020 through 2025, culminating in an estimated global market around USD 215 million in 2025 (revenue unit: Million USD). Looking forward, our base forecasting scenario (2026–2032) projects a compound annual growth rate of approximately 6.98%, with the market approaching the high‑hundreds of millions by the end of the forecast window. This is growth sufficient to sustain multiple strategic plays — premium product rollouts, subscription services, and continued investment in smart device ecosystems.

Electric Toothbrush Market

Concentration metrics in our analysis point to a market that remains fragmented: the leading global brands capture a material but not overwhelming share of sales. That fragmentation creates persistent whitespace for both incumbent innovation and nimble challengers willing to pair product differentiation with channel sophistication.

Electric Toothbrush Market

Why this matters for 2026 corporate strategy

- Allocate R&D selectively: A sub‑10% CAGR with pockets of higher growth argues for targeted R&D spending — prioritize platform investments (sensors, battery, connectivity, brush‑head materials) that scale across multiple SKUs rather than one‑off features.

- Monetize services: Subscription and consumable models (brush pods, replacement heads, coaching services) convert product sales into recurring revenue and defend margins against pure price competition.

- Channel plays are decisive: The interplay between DTC, retail, and dental/professional channels will determine headline growth and margin capture in 2026. Winning requires differentiated propositions by channel, not a single go‑to‑market template.

- M&A and partnerships: With modest top‑line scale at the category level and fragmentation among manufacturers and OEM/ODM providers, bolt‑on transactions and strategic JV structures can accelerate access to technology or distribution with limited capital outlay.

- Regulatory readiness: Quick clearance pathways and clinical evidence packages shorten time‑to‑market in key geographies — a nontrivial competitive advantage for product launches planned in 2026.

Key market forces shaping 2026

- Technology convergence: Sonic and oscillating mechanisms remain table stakes; differentiation now comes from embedded sensors (pressure, orientation), app connectivity, AI coaching, and UX innovations such as medical‑grade silicone brush heads. Expect product roadmaps in 2026 to emphasize software and service tie‑ins as much as mechanical performance.

- Premiumization versus accessibility: The category splits into ultra‑premium smart devices and value models. Margin expansion is possible at the premium end, but volume growth in broader geographies will be driven by affordable, reliable devices and trade programs.

- Supply chain and unit economics: Manufacturing cost variability remains wide — from low‑single‑digit to mid‑double‑digit dollars per unit depending on feature set. Cost engineering and supplier diversification will be critical to sustain margins as competitive intensity increases.

- Regulatory and standards environment: In major markets, electric toothbrushes are regulated as medical devices or under performance test standards. Compliance with regulatory frameworks and ISO test standards is now a board‑level issue for any company scaling global distribution.

- Reimbursement tailwinds: Policy moves to broaden FSA/HSA eligibility for oral care products could materially alter consumer price dynamics in some markets; scenario planning should treat reimbursement expansion as a plausible upside risk to adoption in 2026–2027.

Competitive landscape — what leading players are doing

The market features a mixture of global CPG and medical‑device incumbents, digitally native DTC brands, and a robust OEM/ODM base. Strategic positioning varies by company:

- Royal Philips N.V.: The Sonicare franchise remains a flagship example of platform evolution — next‑generation sonic technology, integrated pressure detection and improved connectivity are core to maintaining premium positioning. Recent product introductions indicate continued investment in flagship ranges and brand refresh.

- Procter & Gamble (Oral‑B): Oral‑B’s oscillating‑rotation iO series exemplifies the incumbent playbook: advanced mechanical engineering married to UX‑led features that lower friction for manual‑to‑electric conversion. New models designed to simplify consumer switching are a defensive priority.

- Colgate‑Palmolive and Panasonic: Both keep the category competitive with broad portfolios focused on reliability and distribution breadth; product differentiation emphasizes practicality and proven cleaning mechanisms.

- Waterpik and specialized innovators (Foreo, quip, Oclean): These players layer unique value propositions — Waterpik with integrated water flossing bundles, Foreo with silicone hygiene advantages, quip with subscription and DTC ease, and Oclean with AI coaching. Their speed to market and consumer positioning pressure incumbents to respond on product and service fronts.

- OEM/ODM ecosystem (China and India‑based manufacturers): A dense supplier base provides scale manufacturing, rapid prototyping, and certification capabilities — attractive targets for strategic partnerships or M&A to compress time‑to‑market for new SKUs.

Notable recent product launches underscore the competitive churn: major brand refreshes and new model introductions in 2025–2026 confirm the category’s innovation cadence and the importance of coordinated product‑launch playbooks.

Regulatory and compliance considerations

- In key geographies, electric toothbrushes are subject to medical device classification and premarket controls. Preclearance strategies and clinical validation plans should be in place for any product targeting regulated markets in 2026.

- ISO and material standards govern performance and biocompatibility; these standards increasingly inform purchasing decisions by professional channels and sophisticated retail partners.

- Companies must build compliance checkpoints into product development to avoid last‑mile delays — especially for novel materials and software‑based features subject to cybersecurity and data‑privacy scrutiny.

Strategic imperatives for executives planning in 2026

- Prioritize platform flexibility: Invest in modular electronics and brush‑head architectures that allow features to be recombined across price tiers with limited retooling.

- Design for recurring revenue: Structure brush‑head replacement, subscription coaching, and bundled consumables to maximize LTV while keeping CAC manageable via channel incentives.

- Lock in go‑to‑market routes: Define differentiated propositions for DTC, retail and professional channels; deploy piloted partnerships to validate price elasticity before full roll‑out.

- Operationalize regulatory readiness: Acquire or partner for clinical chemistry, biocompatibility and 510(k) filing expertise early in development cycles.

- De‑risk the supply chain: Qualify alternate suppliers, negotiate volume‑based ergonomics, and adopt cost engineering to protect margin across foreseeable material and labor cost volatility.

- Use M&A as capability acceleration: Target premium tech boutiques, AI coaching startups, or established OEMs to leapfrog internal timelines for 2026 product roadmaps.

What the full PW Consulting report delivers (practical, actionable content)

Our comprehensive offering is built to be operational from day one for product, commercial, and corporate strategy teams. Highlights include:

- Probability‑weighted market sizing and a dynamic forecasting model (2026–2032) you can run under alternate premia and adoption scenarios.

- Channel and pricing playbooks with sensitivity analyses that translate consumer price points into unit economics and profit pools.

- Product roadmaps tied to manufacturing cost matrices and supplier archetypes. (We provide unit‑level cost ranges by feature set — useful for build vs. buy decisions.)

- Regulatory navigation maps and fastest‑path checklists for major markets, including clinical evidence templates to support 510(k) and ISO verification.

- Competitive benchmark dossiers for the leading brands and an M&A shortlist of high‑value OEM/ODM and software startups — prioritized by strategic fit and execution risk.

- Go‑to‑market launch playbooks (90‑day and 12‑month plans) that align marketing, channel, and supply chain milestones to minimize time‑to‑revenue.

How to apply these insights in 2026

Use the macro lens provided here to set your portfolio priorities and the full study to operationalize them. If your board is deciding resource allocation for 2026, the decision frameworks in our report convert the category’s projected mid‑single‑digit CAGR into specific investment thresholds across R&D, marketing, and M&A. Scenario pathways — from accelerated premium adoption to rapid commoditization — let leadership test outcomes before committing capital.

We intentionally omit segmented tables and granular regional breakdowns from this preview. The full report contains the proprietary, disaggregated datasets, channel forecasts, and product‑level economics required to execute on the plays above. If you are preparing product launches, evaluating acquisition targets, or redesigning distribution for 2026, that level of detail is essential.

Next steps

PW Consulting can provide expedited advisory engagements to translate this market outlook into a 90‑day action plan: prioritizing product requirements, identifying partner targets, and sequencing regulatory milestones to meet 2026 commercial objectives. Contact our strategy desk to access the full report and the underlying models that power it.

For detailed analysis of this topic, please visit the official page:Electric Toothbrush Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com